Does your business have access to a steady cash flow for day-to-day expenses? If not, have you thought of what the solution can be? While every business requires a steady flow of capital to operate efficiently, ensuring the same is hectic. So, while you plan to get your business a helping hand with daily expenses, you can get assistance from leading fintech management platforms such as EnKash.

Whether running a small startup or a large corporation, having enough cash is essential to keep your business running smoothly. Working capital is the money available to a company to meet its day-to-day expenses. It’s the difference between your current assets and liabilities. Now, you must be wondering what do working capital loans mean. They are a type of financing that provides businesses with the necessary funds to cover their day-to-day expense.

This blog will discuss the features and benefits of working capital loans.

Features of working capital loans

Working capital loans are short-term loans (in most cases, revolving credit) intended to cover a business’s expenses for a short period, usually up to 12 months. Read further to learn about the features of working capital loans.

These loans come with a fixed repayment period and a fixed interest rate. Here are some key features of working capital loans:

Quick access to funds: Unlike traditional loans that take a long time to process, working capital loans are usually approved within a few days. This makes it easy for businesses to get the funds they need quickly

Flexible repayment options: Working capital loans come with flexible repayment options. Businesses can choose to pay back the loan in monthly or quarterly installments, depending on their cash flow

Unsecured loans: Most working capital loans are unsecured, which means businesses don’t have to provide collateral to secure the loan. This is beneficial for small businesses that may not have enough assets to offer as collateral

Low credit score requirements: These loans typically have lower credit score requirements than traditional loans. This makes it easier for businesses with lower credit scores to get approved for a loan

Types of working capital loans

There are two main types of working capital loans: secured and unsecured. Let’s take a closer look at each of these types.

Secured working capital loans: Secured working capital loans require collateral to secure the loan. Collateral can be in the form of assets such as property, equipment, or inventory. Secured loans usually come with lower interest rates than unsecured loans since the lender has some security in case the borrower defaults on the loan

Unsecured working capital loans: Unsecured working capital loans do not require collateral to secure the loan. These loans are riskier for lenders since they have no security if the borrower defaults. Therefore, unsecured loans usually come with higher interest rates than secured loans

What are the benefits of working capital loans?

Working loans offer several benefits to businesses. Here are some of the top benefits of working capital loans:

Maintains cash flow: Working capital loans help businesses maintain a steady cash flow, which is essential to meet their day-to-day expenses. This ensures that businesses have enough funds to cover their bills, payroll, and other expenses

Helps businesses seize opportunities: Businesses need to act quickly when opportunities arise. Working capital loans can provide businesses with the necessary funds to take advantage of these opportunities, such as investing in new equipment or expanding their operations

Businesses manage seasonal fluctuations: Many businesses experience seasonal fluctuations in sales. Working capital loans can help businesses manage these fluctuations by providing them with the necessary funds to cover their expenses during slow periods

Helps businesses improve credit scores: By taking out and repaying working capital loans on time, businesses can improve their credit scores. This can make it easier for them to secure future financing at better rates

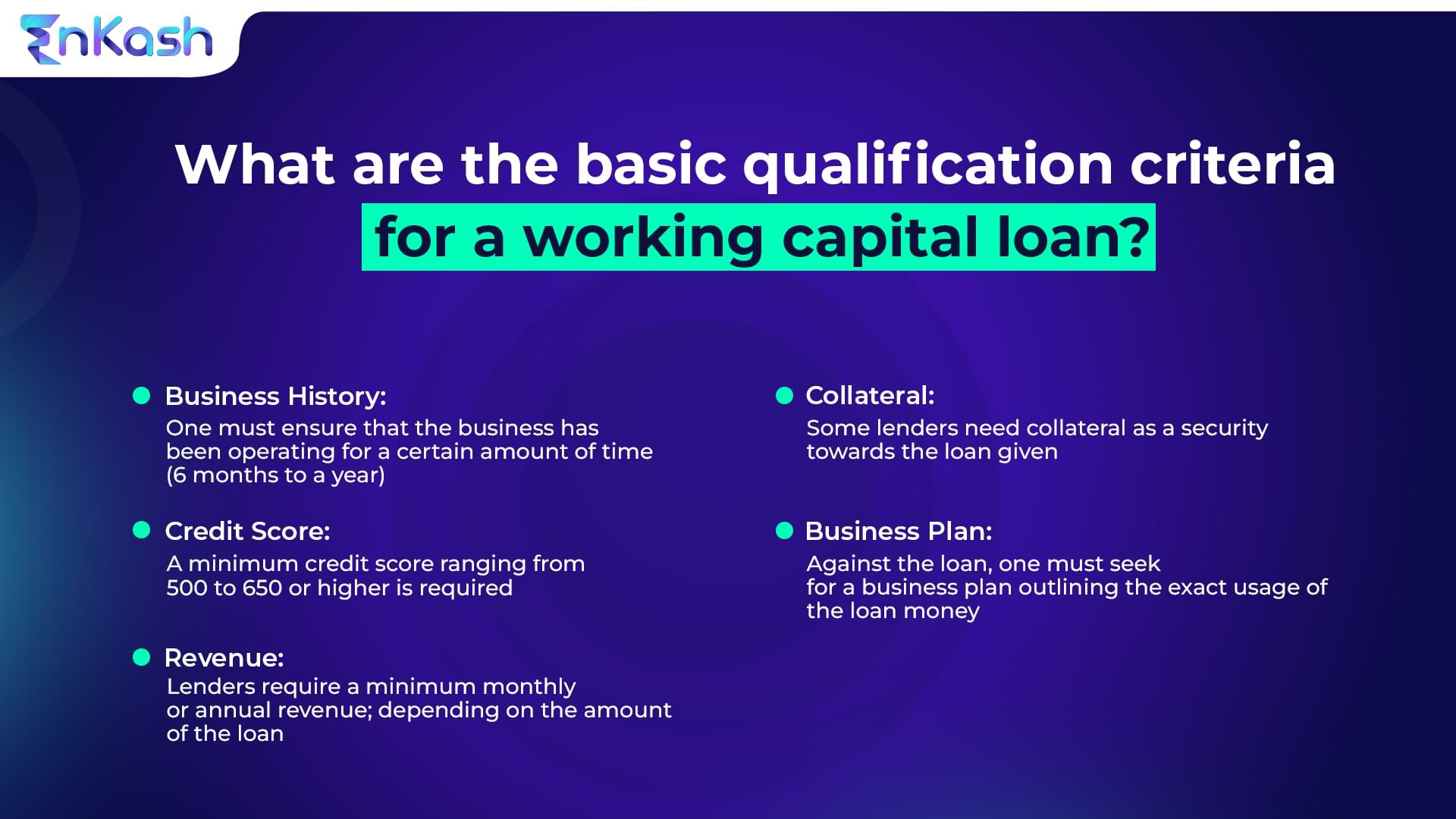

Basic criteria to get working capital loan

Conclusion

So, working capital loans are an essential financing tool for businesses of all sizes. If you wish to ensure that you get the working loan in time, make sure to keep your CIBIL score impressive. Use a corporate credit card to ensure a good CIBIL score.

When considering financing options for your business, working capital loans should be at the top of your list. Whether you need funds to cover unexpected expenses, invest in new equipment, or expand your operations, working capital loans can provide you with the necessary capital to achieve your goals. By taking advantage of working capital loans, businesses can maintain cash flow, seize opportunities, manage seasonal fluctuations, and improve their credit scores.

If you’re looking to finance your business, consider a working loan. You agree that working capital loans are valuable for businesses needing quick access to funds. They offer flexible repayment options, lower credit score requirements, and the ability to maintain a steady cash flow.

For more such fintech-related queries and advice, visit our website today! Get the best assistance with EnKash now!

Does your company have its very own credit card? If not, how do you make and track all the expenses for your business? Well, are you aware of the fact that credit card for company have become an essential tool for businesses of all sizes?

The best corporate credit cards provide a convenient way to make purchases, manage expenses, and track spending. With the right credit card, companies can earn rewards and cash back on their purchases, which can help to reduce costs and improve the bottom line. However, managing credit card spending can be a challenge, and it requires careful planning and attention to detail.

In this blog, we will discuss the importance of managing credit card for company and its spending. We will also talk about the tips and strategies to help businesses make the most of their credit cards. We will also discuss the best practices for managing company credit card spending and how to manage credit card rewards and incentives.

Importance of managing credit card spending

Credit card for company and its spending is a critical area for businesses to manage. If not managed correctly, it can lead to overspending, cash flow problems, and even fraud. By managing credit card spending, companies can avoid these issues and ensure that their expenses are under control.

One of the most significant advantages of using a credit card for company expenses is the ability to track and categorize expenses. Many credit cards provide detailed statements that break down expenses by category, making it easy to see where the company is spending its money. This can be helpful for budgeting and planning, as well as for identifying areas where the company may be overspending.

Another advantage of managing credit card for company and its spending is the ability to take advantage of rewards and incentives. Many credit cards offer cash back, points, or miles for purchases, which can help to reduce expenses and improve the bottom line. However, to make the most of these rewards, it is essential to manage credit card spending effectively.

Apply for a business credit card with EnKash.

Best practices for managing company credit card spending

Managing credit card spending for a company can be a challenging task, but there are some best practices that businesses can follow to make the process easier and more effective.

Set spending limits: One of the best ways to manage credit card spending is to set spending limits for each cardholder. This can help to ensure that employees are not overspending or making unnecessary purchases. Businesses can set spending limits for each cardholder based on their role and responsibilities, and they can adjust these limits as needed

Monitor transactions: Monitoring credit card transactions is critical for managing expenses and identifying potential issues. Businesses should review credit card statements regularly to ensure that expenses are legitimate and to identify any unusual or unauthorized transactions. Many credit card companies offer fraud protection services that can alert businesses to suspicious activity

Use expense management software: Expense management software can help to streamline the process of managing credit card spending. This software can automate expense reporting and categorization, making it easier to track expenses and identify trends. Many expense management tools also integrate with credit card companies, making it easy to import transactions and monitor spending

Encourage responsible use: Encouraging responsible credit card use among employees is critical for managing expenses and maintaining good credit. Businesses should provide training and guidelines for credit card use, including how to make purchases, when to use the card, and how to track expenses. Employees should also be encouraged to report any issues or concerns regarding credit card spending

Managing credit card rewards and incentives

Managing credit card for company’s rewards and incentives is an essential part of managing credit card spending for a company. To make the most of these rewards, businesses should consider the following strategies:

Choose the right credit card: Choosing the right credit card is critical for earning rewards and incentives. Businesses should consider the types of purchases they make most frequently and select a credit card that offers rewards for these purchases. For example, if the company frequently travels, a credit card that offers rewards for airline miles may be a good choice

Maximize rewards: To maximize rewards, businesses should use their credit cards for as many purchases as possible, including recurring expenses like utility bills and office supplies. It is also important to pay the credit card bill on time and in full each month to avoid interest charges and late fees

Redeem rewards wisely: Businesses should carefully consider how to redeem their credit card rewards to get the most value. Some credit cards offer cash back, while others offer points or miles. Businesses should choose the reward that provides the most value and consider the redemption options available

Keep track of rewards: Keeping track of credit card rewards is critical for managing expenses and maximizing rewards. Businesses should track their rewards and ensure that they are being credited properly. Many credit card companies provide online tools to help businesses manage their rewards

Conclusion

Credit card for company is an essential tool for managing expenses and improving the bottom line for businesses. However, managing credit card spending can be a challenge. By following the best practices for managing company credit card spending and taking advantage of credit card rewards and incentives, businesses can ensure that they are making the most of their credit cards.

Apply for a business credit card today with EnKash, the spend management platform that deserves for your business. You can also enjoy the perks that you and your business deserve!

Choosing one of the best corporate credit cards and applying for a business credit card with suitable rewards and incentives can significantly impact the financial health of a company. You can do that with EnKash, your very own fintech solution provider. By paying attention to credit card spending and rewards, EnKash can help your business to save money and improve their overall financial health.

Processing payments is one of the most crucial part of any business; and ensuring that you process payments through a trusted provider is very important. So, who is your business payment provider?

As a business owner, choosing the right payment processing provider for your business is essential. With so many options available, allow EnKash to help you make the right decision. We are a spend management platform offering your customized fintech solutions for your business.

But before you get on board with our experts, learn more about payment processing providers and their services!

Introduction to payment processing providers

Payment processing providers transfer of funds between a customer’s bank account and a business’s bank account. They act as intermediaries between the parties, ensuring the transaction is safe and secure. As one of the best payment processing providers, we offer various services, from processing credit card payments to handling bank transfers.

What does a payment processor do?

Payment processors play a crucial role in facilitating transactions between customers and businesses. They ensure that transactions are processed quickly, securely, and efficiently. Payment processors handle all the technical aspects of the marketing, such as authorizing the payment, verifying the customer’s information, and ensuring that the funds are transferred to the correct account.

To begin the payment process, the payment processor receives the customer’s payment information, such as their credit card details, bank account information, or mobile wallet credentials. The processor then sends this information to the issuing bank or payment network, which verifies the customer’s payment credentials and authorizes the transaction.

Once the payment is authorized, the payment processor transfers the funds to the merchant’s account, deducting any applicable fees. Payment processors also ensure that the transaction complies with security standards, such as PCI DSS (Payment Card Industry Data Security Standard), and provide robust fraud protection measures to protect both the customer and the merchant.

Payment processors also offer additional features to make the payment process more efficient and convenient for customers and businesses. For instance, some payment processors offer recurring billing, allowing enterprises to charge customers automatically for ongoing services. Others offer mobile payments or e-commerce integrations, allowing businesses to accept customer payments anywhere and anytime.

Payment processors are essential for businesses that want to accept payments securely and efficiently. They handle all the technical aspects of the payment process, ensuring that transactions are completed smoothly while providing additional features that make it more convenient for customers and businesses.

Tips for choosing the right payment processing provider

Choosing the right payment processing provider can be daunting, but it’s essential to consider some factors before deciding. Here are a few tips to assist you in selecting the right payment processing provider for your business:

Security: Security should be a top priority when choosing a payment processing provider. You want to select a PCI-compliant provider that offers robust fraud protection measures to ensure your customers’ data is safe

Ease of Use: A user-friendly platform will save you time and effort managing your transactions. Look for a provider that offers an easy-to-use platform that makes it simple to manage your payments

Fees: Different providers charge different prices, so it’s essential to understand what you’re paying for. Some providers charge a flat rate per transaction, while others charge a percentage of the transaction value

Customer Support: Look for a provider that offers excellent customer support. You want to be able to get in touch with someone quickly if you have any issues or questions about your account

Features: Consider the features that the payment processing provider offers. Do they offer a platform as a service (PaaS) or an API marketplace? Depending on your business’s needs, either option could be the right choice

Role of API marketplace in payment processing

API (Application Programming Interface) marketplaces are playing an increasingly important role in the world of payment processing. Unlike traditional PaaS (Platform as a Service) solutions, API marketplaces offer more flexibility and control over the payment processing experience.

API marketplaces offer more flexibility than PaaS solutions and allow you to integrate your payment processing into your existing website or app. They provide you with a set of APIs that you can use to build custom payment processing solutions that meet your business’s unique needs. With an API marketplace, you have more control over the payment processing experience and can customize it to meet your specific requirements.

It provides businesses with a set of interfaces that can be used to build custom payment processing solutions that are tailored to their specific needs. This allows companies to integrate their payment processing into their existing website or app, providing a seamless payment experience for their customers.

With traditional payment processors, companies are limited to features and functionality provided by the provider. With an API marketplace, businesses can customize the payment processing experience to meet their requirements.

API marketplaces also offer businesses more scalability than traditional payment processors. As companies grow and their payment processing needs evolve, they can quickly scale their solution by adding or removing APIs as needed. This allows businesses to remain agile and responsive to changing market conditions without completely overhauling their payment processing infrastructure.

Conclusion

Choosing the right payment processing provider is essential for any business. So, make sure that you make the right decision. EnKash provides payment processing tools that ensure critical factors, such as security, ease of use, fees, customer support, and features, to help you make the right decision. Therefore, whether you choose a PaaS solution or an API marketplace, ensure it meets your business’s unique needs and offers the required features and flexibility. By choosing the right payment processing provider, you’ll be able to offer your customers a safe, secure, and convenient way to make payments, and you’ll be able to manage your transactions more efficiently. Let EnKash be your go-to-website for payment-related issues at every stage! Connect with us today and get professional services for your business.

While the world is busy transforming everything online, you should choose a solution for payments that is trustworthy. Now, you must be wondering how one can do that- with EnKash.

So, you must be wondering what a free virtual card is. Read further with EnKash to gain an understanding of free virtual cards!

What is a free virtual card?

Free virtual cards are digital versions of physical credit or debit cards that can be used for online transactions. Virtual cards in India are gaining popularity among small businesses in India thanks to their numerous benefits. One of the key advantages of virtual cards is that they offer increased security compared to physical credit or debit cards.

Virtual cards are not linked to your bank account or physical card, which means that even if your virtual card details are compromised, your bank account and physical card remain safe. When you create a virtual card, you are assigned a unique card number, expiration date, and security code.

This article will explore the benefits of free virtual cards for your business, how they work, and best practices to maximize their security.

How to get started with a virtual card in India for your business?

Many banks and financial institutions offer free virtual cards to their customers. EnKash in collaboration with a few banks is one such free virtual card provider. To get started, log in to your bank account or mobile wallet app and look for the option to create a virtual card.

When selecting a business credit card in India, it’s essential to research and compare different providers’ features and benefits. It’s also necessary to ensure that your virtual card provider is reputable and has a track record of providing secure and reliable services. Some providers of providers of business credit cards in India, offer additional features, such as cashback rewards or discounts on select merchants, which can help you save money on your online transactions.

Creating a free virtual card with EnKash

Once you have chosen a virtual card provider, creating a virtual card becomes straightforward. Log in to your bank account or mobile wallet app, select the option to create a virtual card, and follow the instructions. You will be prompted to enter the details, such as the card number, expiration date, and security code. Once coated, you can use it for online transactions.

One of the main advantages of using virtual cards for your business is that you can create multiple virtual cards with specific limits and expiration dates for each transaction or vendor. This can help you keep track of your expenses and prevent unauthorized transactions. It also lets you control your spending by limiting the amount charged to each virtual card.

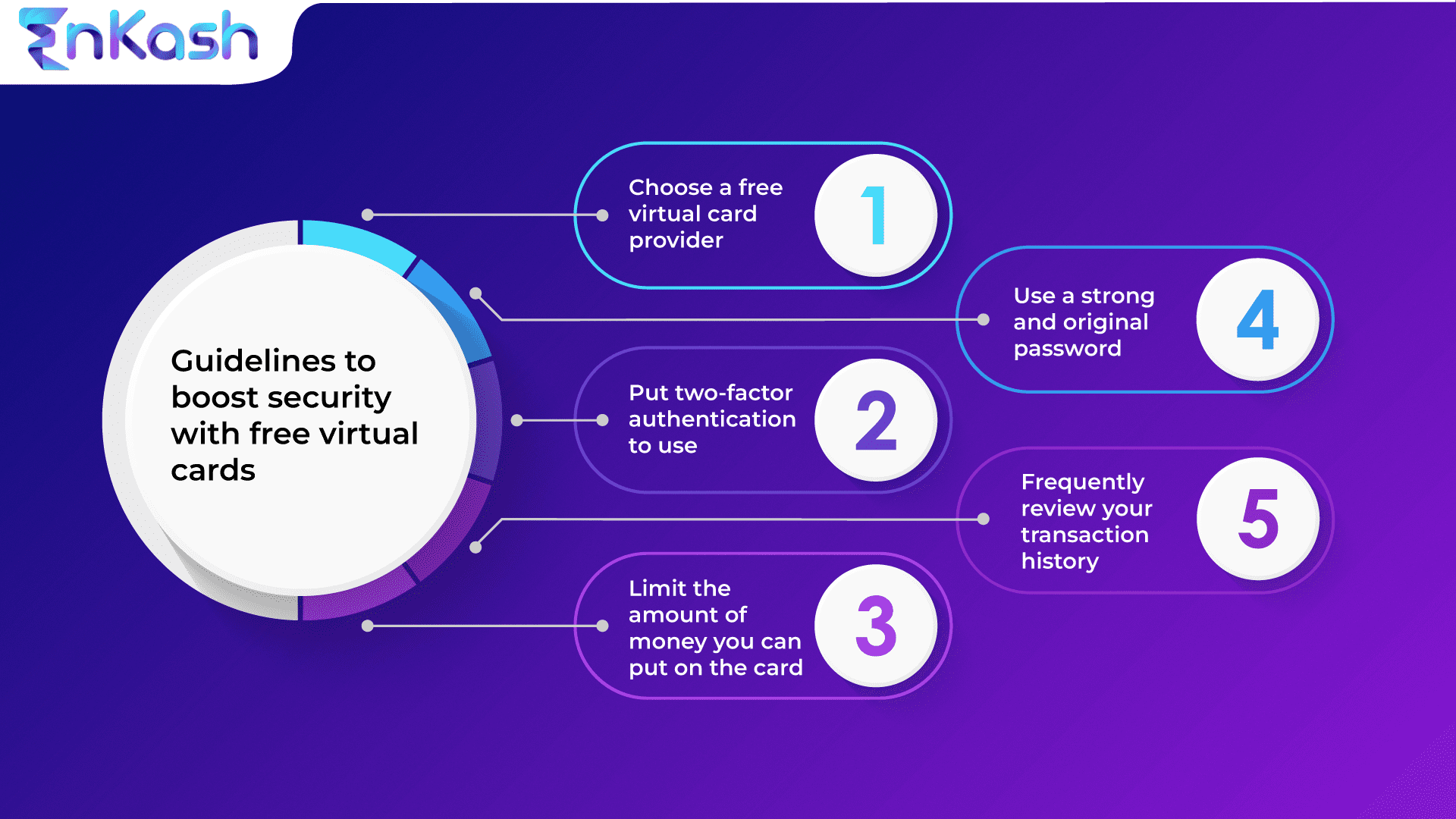

Best practices to maximize security with free virtual cards

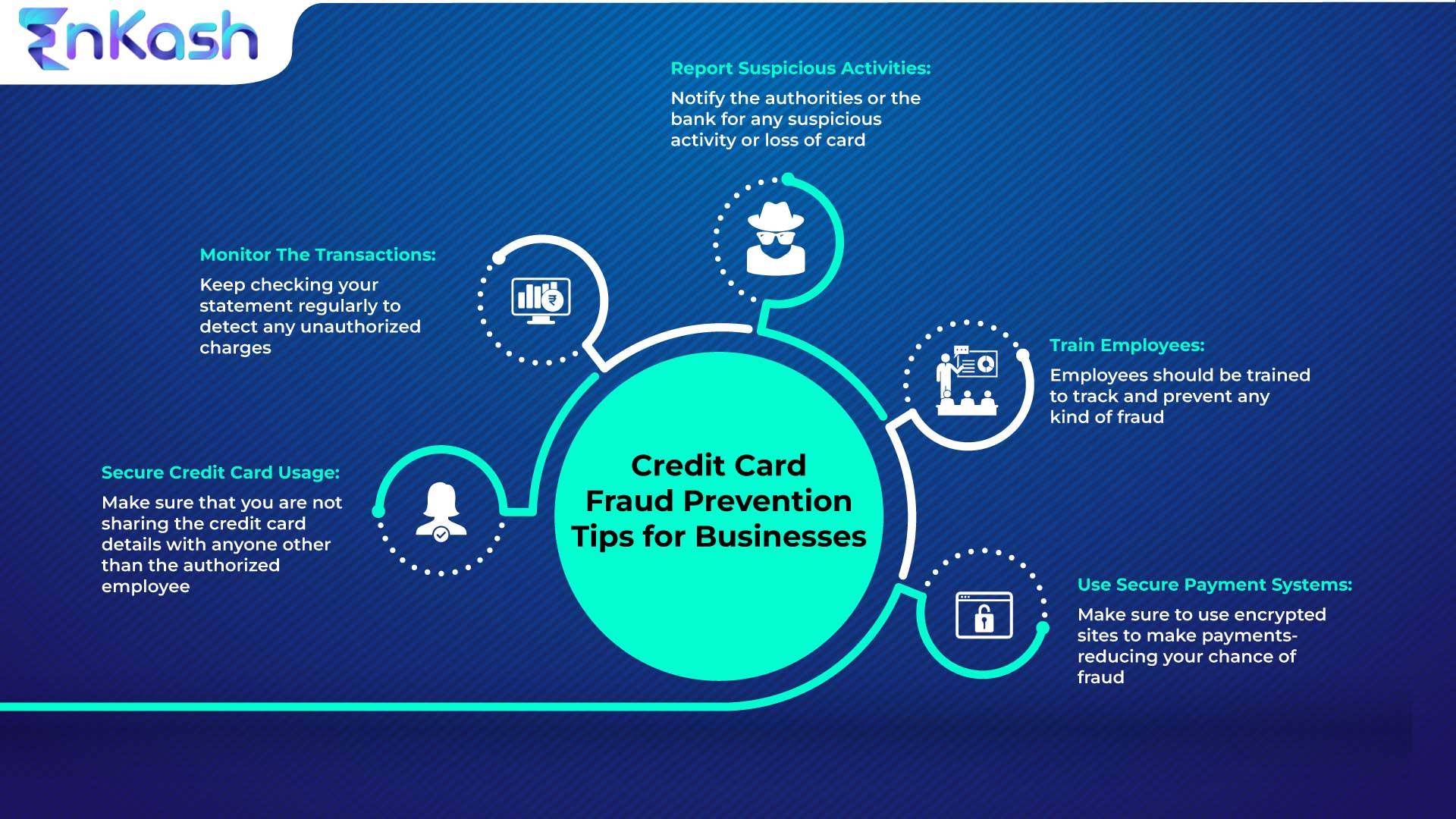

While virtual cards offer increased protection for online transactions, taking precautions to protect your financial information is still essential. Read below some of the best practices to keep in mind:

Use a strong password and enable two-factor authentication for your bank account or mobile wallet app

Only use virtual cards for reputable and trusted websites and merchants

Regularly monitor your virtual card transactions for any suspicious activity

Always use a secure internet connection when making online transactions

In addition to the above-mentioned best practices, keeping your virtual card details confidential is essential; do not share them even with your family or friends. Be cautious of unsolicited emails or calls requesting your virtual card information, as they may be fraudulent attempts to steal your financial information.

Another effective way to maximize security with virtual cards is to use them for one-time transactions or with a limited spending limit. This way, even if your virtual card details are compromised, the damage is limited to the spending limit set on the card. Some virtual card providers also allow you to set spending limits or restrict usage to specific merchants, adding an extra layer of security.

When making online transactions, it’s crucial always to verify the website’s security features, such as SSL encryption and the padlock symbol in the browser address bar. This ensures that your financial information is transmitted securely over the Internet.

By following these best practices, you can maximize the security of your virtual cards and prevent fraudulent transactions. It’s essential to constantly scan your virtual card transactions to detect any suspicious activity and report it to your virtual card provider immediately.

Future of virtual cards

Virtual cards are becoming more popular in India as they are a safe and convenient payment option. As more people shift towards online payments, the demand for virtual cards will increase. With technological advancements, we can expect virtual cards to become even more secure and user-friendly soon.

Conclusion

Virtual cards will likely become essential to our financial transactions as the world becomes increasingly digital. Free virtual cards from banks collaborating with EnKash offer a secure and convenient way to make online payments without needing a physical credit or debit card. They are especially beneficial for small businesses that may need more money for a business credit card in India. Following best practices to maximize security, virtual cards can provide peace of mind when making online transactions. Get high-end free virtual cards with us and enjoy a safe and secure transaction in this digital age!

A fascinating step towards sound business spending is virtual credit cards. They provide businesses with a safer, more personalized, and transparent way to pay for rent, vendors, GST, bills, and many other things. A company can make purchases using a virtual card directly from their desktop, which makes managing finances easy for the finance team.

Reduced processing costs, simplified vendor payments, and improved internal accountability are just a few advantages that the virtual card business offers to businesses. Compared to physical cards, these well-known virtual card businesses aid in more cost savings while enhancing simplicity and security for employee purchasing.

This article will cover all that you need to know about using a virtual card business, including how to get an instant virtual credit card free right away and the advantages of doing so. Continue Reading!

What is a virtual card for business?

A virtual credit card is just like a standard credit card, except that you do not possess a physical copy. The cardholder’s name, credit card number, billing address, CVV, and expiration date are all included in a virtual card business, along with all other relevant facts and identifying details.

It acts like a Visa, MasterCard, or any other physical card when making an online transaction. Its ease of use has helped the virtual card business grow swiftly into one of the most affordable, practical, and secure e-payment methods, especially for online transactions.

A digitally constructed virtual card business can be issued for recurring payments, to settle a single transaction issue for a predetermined amount, or to establish a card that can be created on demand and used individually. The cardholder might make further purchases up to the monthly business spending limit in the second circumstance.

Benefits of virtual card business as a payment solution

The primary objective of virtual credit cards is enhanced safety in an increasingly digital world, as is the case with the new financial technology. However, security is just one aspect of the innovative technology connected to virtual card business payments. There are other additional advantages listed below:

Security: Making business payments with virtual cards is extremely secure. Your physical and virtual cards are connected to your primary account. Still, the virtual card business protects your data by restricting the information revealed when you make a transaction. These systems tokenize data, encrypting your account details and generating a random sequence or token that you can only use to make one-time payments.

Easy to use: The ease of use of virtual cards over real ones is one of their key advantages. With the help of these solutions, users may make timely payments without having to deal with the trouble of passing around a business card.

Control on expenses: You may choose your spending limits and the number of merchants you wish to pay using virtual cards. These measures ensure that your employees use business money appropriately and defend your account from hackers.

Get it free of cost: Most card issuers offer this free virtual card, and that too without charging extra. As a result, you can get an instant virtual credit card free right away, and you don’t need to pay anything more to get one.

Enhances accountability: You should no longer stress about making payments or track down the accounts department to acquire receipts for processed payments because of the categorization, labeling, and orderly organization of every payment made so far or still to be paid.

The remaining balance can be transferred: If your virtual card business expires and you still have available credit on your card, it will be transferred to your main credit card to ensure full utilization of your credit card limit.

Steps to apply for a virtual card

Follow these 6 steps to apply for a virtual card:

Visit EnKash’s Website and click on sign up tab

Tap on the credit card tab under the freedom section

Enter GSTIN/PAN details for verification

Save the details and enter the OTP received on your phone number

Upload your company documents, director’s PAN card, e-mail, and mobile number for verification

Submit your application and get your free virtual card

How is a virtual card helpful for businesses?

Manages your budget across teams: When a team member needs a virtual card number, the virtual card business can help you generate, manage, and distribute them. Then, it will be simple for you to keep an eye on that team member’s spending and make sure they stick to the allocated budget.

Act as a business travel card for employees: You can use your virtual card business to arrange travel for personnel representing you at events or on business travels, including lodging and travel.

Serves as an expense management tool: By offering spend analysis and other financial reporting data, some virtual card businesses act as an expense management tool. This helps you know how much money an employee spends and where you don’t want someone to end up overspending or making unwanted expenses.

Monitoring subscriptions and campaigns: Your company may have subscriptions that require monthly or yearly payments. The virtual card business eliminates the hassle of coordinating various payments for multiple subscriptions by filling the card with funds that will cover each subscription service.

Virtual credit cards are superior in many ways compared to traditional credit cards. These cards lower the danger of credit card fraud because they don’t reveal your credit card information to anyone other than you. One of the top digital spend management platforms, EnKash enables companies of all sizes to automate payments and take advantage of paperless transactions.

EnKash lets you manage your financial transactions across your company’s divisions from a single platform. So, manage vendor payments easily, pay recurring bills on time, and allow your finance department to conduct an audit without difficulty with EnKash.

Advance payments are transactions or parts of transactions done in advance. These payments are recorded as assets on the business sheet and made before exchanging goods and services. They are also known as prepaid expenses.

Advance payments are widespread and valuable for businesses to keep track of their assets. Through online GST payment, companies can now file GST on advance payments using their own device from their homes and offices. Let’s understand how you can pay GST on advance payments online safely and securely.

What is GST?

GST, also known as Goods and Services Tax, replaced VAT in 2017 as the indirect tax in India. It is levied on goods and services sold for domestic consumption and has many different tax slabs depending on the product. GST is paid to the supplier at the time of delivery of goods and services. Businesses file GST every month, and businesses can file for GST returns at the end of the financial period, for that you should know about the types of GST returns.

The main feature of GST is that it is entirely digitalized. This means that electronic payments can be made for GST payment at one’s leisure. Moreover, online GST challan payments support various modes of payment, including corporate cards which makes them highly convenient.

What is GST on advance payments?

Because GST payments are made online, businesses can easily track the GST on advance payments. GST on advance payments is exactly like GST on regular transactions. It is calculated as a percentage of the advance payment instead of the total amount. The best part is that GST on advance payments allows businesses to file their taxes in a timely manner.

Here are some crucial points to bear in mind while paying GST on advance payments:

Receipt of advance payment The receipt of advance payment is an essential document when you are generating the online GST challan. It contains the time of supply, which is when the final payment and delivery of goods are decided to take place. This helps both the involved parties, and the authorities compute the date of GST payment. As we will see below, businesses generally prefer to pay the GST on advance payments during the receipt of advance payments.

Exemption of GST on advance payment Another critical point to note is that while GST is paid during the delivery of goods and services, GST on advance payments is compulsorily applicable to services. In simple words, GST on advance payments in the case of services must be paid while making the advance payments. Even in the case of goods, businesses that have opted for the composition scheme must complete the payment of GST on advance payments. This is why tracking and paying GST is important for all businesses when it comes to GST on advance payments.

GST advance receipt voucher For regular transactions, businesses issue a GST tax invoice once they complete the payment. However, in the case of advance payments, they issue a different document called a GST advance receipt voucher. It acts as proof of received payment and includes the company’s particulars, date of issuance, advance payment amount, the GST on advance payment, and the applicable tax rate. Additionally, it must contain the GST identification number of the supplier and the place of supply, including the state and the pin code.

Tax payment under GST is convenient because it can be done on your device. Online GST challan payments can be made on the EnKash portal via these simple steps:

Log in to the government GST portal

Create the GST challan

Select NEFT/RTGS as the payment mode

Enter remitting bank name

Upload the generated challan on EnKash portal

The challan is auto-verified with the maker/checker approvals

Pay the GST on advance payments using credit cards or any other convenient mode

Using the EnKash portal, you can quickly pay tax under GST. It provides a user-friendly interface to track GST challans and manage the company cash flow. Furthermore, it provides a centralized location to monitor GST payments, make timely payments, and avoid penalties.

Besides, online GST challan payments allow you to pay using various payment methods. EnKash auto-reads GST challans and converts them into payment records swiftly. It also shares insights from past records and enables businesses to proliferate. Finally, EnKash can help you streamline tax payments by ensuring safe and smooth transactions.

Conclusion: You can now make GST payments using the EnKash portal. EnKash is a spend management platform built specifically for business needs. It uses efficient software programs to deliver a hassle-free experience while paying GST on advance payments. Complete online GST challan payments quickly and never worry about last-minute struggles.

Credit card processing services are vital to online and offline business transactions. The ability to accept credit card payments could make or break your company. If you are running a small start-up or looking to start one, you must decide which system you should choose.

Accepting payments online is simple, with the best credit card processing for small businesses. This can be done directly through a website or by sending payment requests via email. There are two primary options for credit card processing services:

A straightforward best credit card processing for small businesses with all fees paid per transaction

A merchant-account solution with a monthly subscription but much cheaper best credit card processing for small businesses per time

A point of sale (POS) system’s ability to best credit card processing for small businesses process is just one of its many functions. Continue reading to learn more about start-up credit cards, the best credit card processing for small businesses, the benefits of business credit cards, and how to apply for a business credit card.

What is a start-up credit card?

Start-up credit cards are the best credit cards for small businesses designed for new businesses. This card operates similarly to other corporate credit cards. They are linked to credit lines, so any transactions made using the cards and repaid on time can increase the credit line with consistent, timely repayments.

Having a start-up credit card can assist in resolving several problems that are exclusive to fledgling enterprises. Using start-up credit cards can assist budding business owners in maintaining a gap between their personal and corporate expenses. Credit cards may help a new firm experiencing a temporary financial shortage because they give access to money when needed. For this reason, a new business must obtain a start-up credit card.

Best business card for small businesses and its benefits

There are several differences between a business credit card and a personal credit card. But the major difference is their intended purpose. A personal credit card is meant for personal expenses. It is tied to an individual’s personal credit history, while a business credit card is designed for business expenses and is linked to the business’s credit history.

Apart from that, the other differences cover the spend limit, credit history and liability, and rewards and benefits, to name a few. Moreover, tools for managing a company’s expenditures are included with business credit cards, including expense tracking. EnKash is a spend management platform that assists all businesses with virtual credit cards through their trusted banking partners. We offer fintech solutions that are simple to use and can be adapted to your business.

Here are a few benefits of using a business credit card:

Minimize cash-flow issues: A corporate card optimizes business cash flow by enabling you to make necessary purchases even when you are suddenly short on cash. Your cash flow may become more balanced, making your company less susceptible to fluctuations over the short term.

Building credit score: Establishing and enhancing your company’s credit score can be accomplished by accumulating a robust payment history. The same is true for your business credit card as it is for your personal credit card: you can borrow more money and pay less interest, and it may even cut your insurance rates and make it easier for you to rent a property.

Additional benefits: A corporate credit card may come with extra perks than your card, like more cash-back points or frequent flyer miles, waived airline baggage fees, access to airline lounges, and other savings.

Separation from personal spending: Keep your personal and business expenses separate to maintain accurate reporting. By not mixing your assets with the company’s, using a different credit card specifically for business helps keep accounting organized.

Things to remember while choosing a business credit card

Business requirement: Business owners or those searching for a business credit card should be fully aware of their requirements for a credit card. These cards will also make it easier for businesses to create reports and conduct in-depth analyses of every spending. A company may decide to issue corporate credit cards to its employees, each with a predetermined spending limit.

Card offers: Business credit cards come with offers or discounts that entice consumers to use them frequently. Some cards grant access to airport lounges, while others give points on fuel purchases. Some corporate credit cards provide air miles that can be exchanged for each flight booked.

Fees and interest rates: The interest rates on many online credit cards are hefty. Therefore, it is crucial to consider interest rates before choosing a business credit card. Credit card issuers sometimes list monthly interest rates, provide an interest-free credit period of up to 48 days, or charge an annual subscription fee.

Credit limit: The credit limit is based on the applicant’s credit risk profile, credit history, and other variables. Before finalizing the company credit card application, the applicant should always confirm the credit limit. By doing this, it will be possible to prevent a firm from receiving a card with an extremely low or high credit limit.

Convenience: Business owners typically do not have much free time. As a result, they would want to save time working out the application and paperwork procedure. A business should always choose an online credit card that guarantees a simple overall application process and has low documentation requirements.

Steps to get a business credit card for small businesses

Visit EnKash’s Website and click on the signup tab

Enter your phone number and official email ID to create an account

Enter the OTP and login to access the platform

Click on the credit card option

Enter your GSTIN number and the password

After saving the details, connect your bank account with EnKash

Upload bank account statement and initiate verification

After that, select the company type and sub-category

Upload the director’s PAN, email address, and mobile number

Submit the application

A business credit card gives businesses a readily available credit limit and a slightly delayed repayment period to pay for significant business needs. A company can take advantage of an interest-free approach to acquire the things that help their firm grow, whether buying new machinery, minor equipment or investing in new software. EnKash enables businesses to get the best credit card processing for small businesses with all the advantages of a start-up company.

These cards also offer a flexible billing cycle to help manage cash shortages, a straightforward KYC procedure, complete control over transactions, and the ability to attach several cards for various uses. Visit the official website immediately and apply for one of the best business cards for your new company to enjoy its benefits.

In this digital era, everyone has become more aware of the product prices in the market. They are well aware of new vouchers that can help them save money while making bill payments. The power of ‘offers’ is quite evident in the present market, and businesses are gaining massive benefits from it. Here is a detailed guide to bill payment offers and how they benefit companies of all sizes.

What is a bill payment offer?

A timely bill payment is an integral part of everyone’s life, as it helps to keep you away from financial trouble. Bill pay service is the facility businesses offer their customers or vendors to help them easily make utility payments online without missing any payment. In addition, you will not have to worry about heavy penalties, poor credit scores, and other unnecessary issues by making timely payments.

Bill payment offers refer to different discounts that your vendor offers to the business to pay bills online, along with saving some extra money. Bill payment offers are undoubtedly the best way companies can invite new customers or vendors to their page, along with retaining the existing ones.

How bill payment offers are helpful for the business?

Today, numerous online bill pay service platforms have been introduced that offer ease of bill payment to help businesses make their regular payments on time. These platforms provide various bill payment offers so that the users can enjoy the payment process while saving an extra amount on each bill they pay.

By using a particular platform each time to make a payment, your business can enjoy numerous advantages and gain trust and loyalty. EnKash is a spend management platform that offers online bill payment services to ensure timely and automatic payment. In addition, they offer a single platform to easily make all the payments and provide the best bill payment offers.

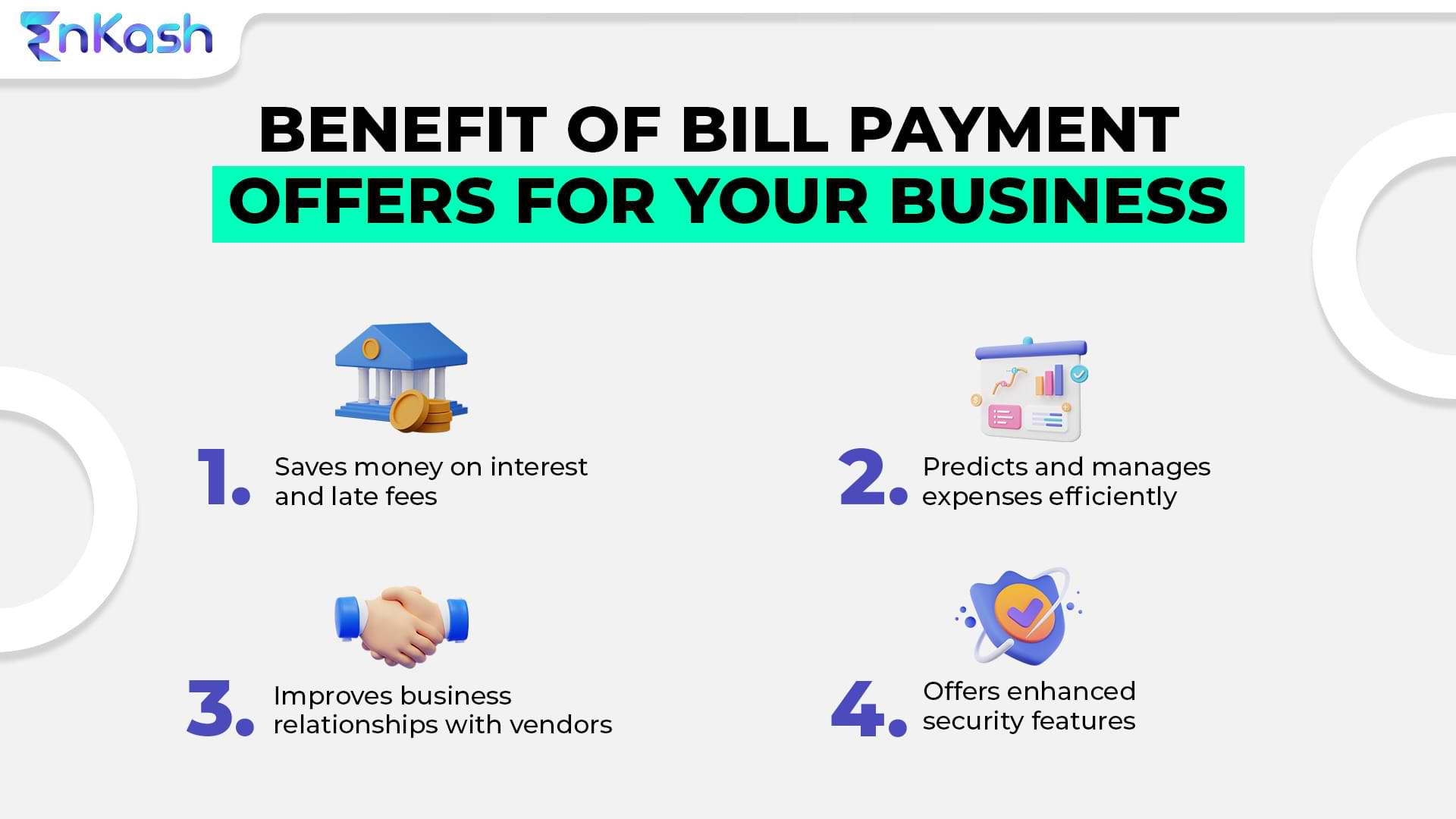

Benefits of online bill payment

Opting for a pay bill online is a way of getting financially organized. It helps to eliminate the chances of errors and makes financial management much easier for businesses. Below listed are some of the benefits your business can gain from making an online bill payment:

Convenient While you set up an automatic pay bill online method for your business, you let recurring payments for your bills be made easily and on time. Enrolling the details is a one-time process, after which your bank takes over the recurring payment process. All the account details are organized and stored at one centralized location, and there are no chances of any late or missed payments. One of the most significant advantages of using online payment options is that it offers various advanced features to businesses.

Secure By using an online payment method, you don’t need to be concerned about sharing your private information. Paying online also protects your identity and privacy by removing the possibility of lost or stolen documentation.You will no longer be required to pay for checks, stamps, or envelopes, and you can also cut your petrol expenses. By eliminating paper bills, your business can even reduce the environmental impact.

Instant payment Instant payments are made possible for businesses through online payments. Making a payment is simple and convenient while seated at home or work. It eliminates geographical limitations and enables buyers to make purchases even when they are not there physically. In addition, the online payment gateway offers businesses a quick transaction confirmation, allowing them to feel secure about their purchases.

Control payments With the online bill pay service and its advanced features, you can control when and how your business can pay the bills. You can even change or cancel the payment request until the payment is completed.

Get rewarded Pay bill online method has gained popularity, wondering why? The online bill payment platform offers numerous rewards and advantages to businesses for making regular and timely payments. You can get bill payment offers or reward points if you use your credit card to make regular payments. Due to all these expenses, numerous points are added to your credit card account each month.

Build credit score When your business pays bills on time by automatically setting payments, it helps boost your credit score. A good credit score positively affects your business processes as you can easily avail of a loan. The higher the credit score, the better it will be for your business processes in the future.

Best cards for bill payment offers

The virtual card is a unique and digitally generated 16 digits credit card that helps users to pay online. It is the same as the physical card that contains all the details like credit number, CVV and validity date, but the details are available online. These cards offer instant online application advantages to the users. EnKash provides the best virtual cards for business needs and offers customized services. With our virtual card, businesses can make timely bill payments, decentralize spending with DIY factors and take advantage to block, unblock, track, and manage expenses without any additional support. So, with virtual cards powered by our trusted banking partners, you can easily reduce costs and make timely payments.

Conclusion

Paying bills on time is crucial for every business’s growth and stable operations. Various online platforms, like EnKash, provide bill payment offers to help save money on every payment.

Do you want to streamline payment processing for your business? Connect with us and enjoy the best bill payment offers. With our platform, we help companies to pay their bills automatically. You can now set auto reminder notifications for the bills from our platform and never miss a chance of timely payments. Explore our solutions to improve spending quality and plan your cash flow in the best way possible.

The PCI DSS (Payment Card Industry Data Security Standard) was formed in the year 2004 by American Express, Discover Financial Services, MasterCard, Visa, and JCB International. The objective of these guidelines is to ensure certain compliance norms. The key is to ensure that credit and debit card transactions are secured against theft and fraud.

Even though PCI DSS does not have the legal authority to compel the compliance aspect, it has become a necessity for any business that processes card transactions. The obvious inference from the above is that fintech, which is a culmination of finance and technology, will have a lot to do with being PCI DSS compliant.

In this article, we will look at the measures required for a business to remain PCI DSS-compliant along with the relevance of PCI DSS compliance to the fintech sector.

Fintech and PCI DSS; The Connection

Today’s financial services require not only numerous options, convenience, simplicity, and accessibility but also security. Fintech enables finance and finance operations to move from the physical realm to the virtual world. Here are some leading examples of where technology has transformed finance.

Payments: In today’s world, fintech has met the need for immediacy when it comes to payments and businesses tend to make electronic payments online with a few clicks either on their laptops or on their phones.

Virtual accounts: Another aspect that technology has touched positively is that of bank accounts that are virtually accessible in the form of virtual accounts. No longer do you see the finance team making multiple visits to their bank.

Card transactions: The use of cards for personal as well as business transactions is on the rise and this is not only because of the acceptance and convenience but also because technology offers layers of security that add to our confidence.

Collections: Fintech has a role to play in accounts receivable not only with timely reminders and invoices on the go but also with a plethora of options that make it easy to receive payments.

Audits: When we talk about finance, audits cannot be far behind. Fintech has helped in this aspect as well with the creation of virtual approval flows and real-time documentation in a matter of seconds.

Reconciliation: When a business makes numerous payments and collects from many accounts, then it is likely that bank reconciliation becomes a huge task. However, technology helps in this aspect as well with automatic matching and reconciliation.

As you can see from the above instances, fintech is instrumental in easing many processes and operations in finance. And when you move finance from the physical world to the virtual world, then security is a real concern, which is where PCI DSS comes into place.

How to become PCI DSS compliant?

PCI DSS sets forth some operational and technical guidelines with a focus on ensuring that the cardholder’s data is kept safe.

How to become PCI DSS Compliant

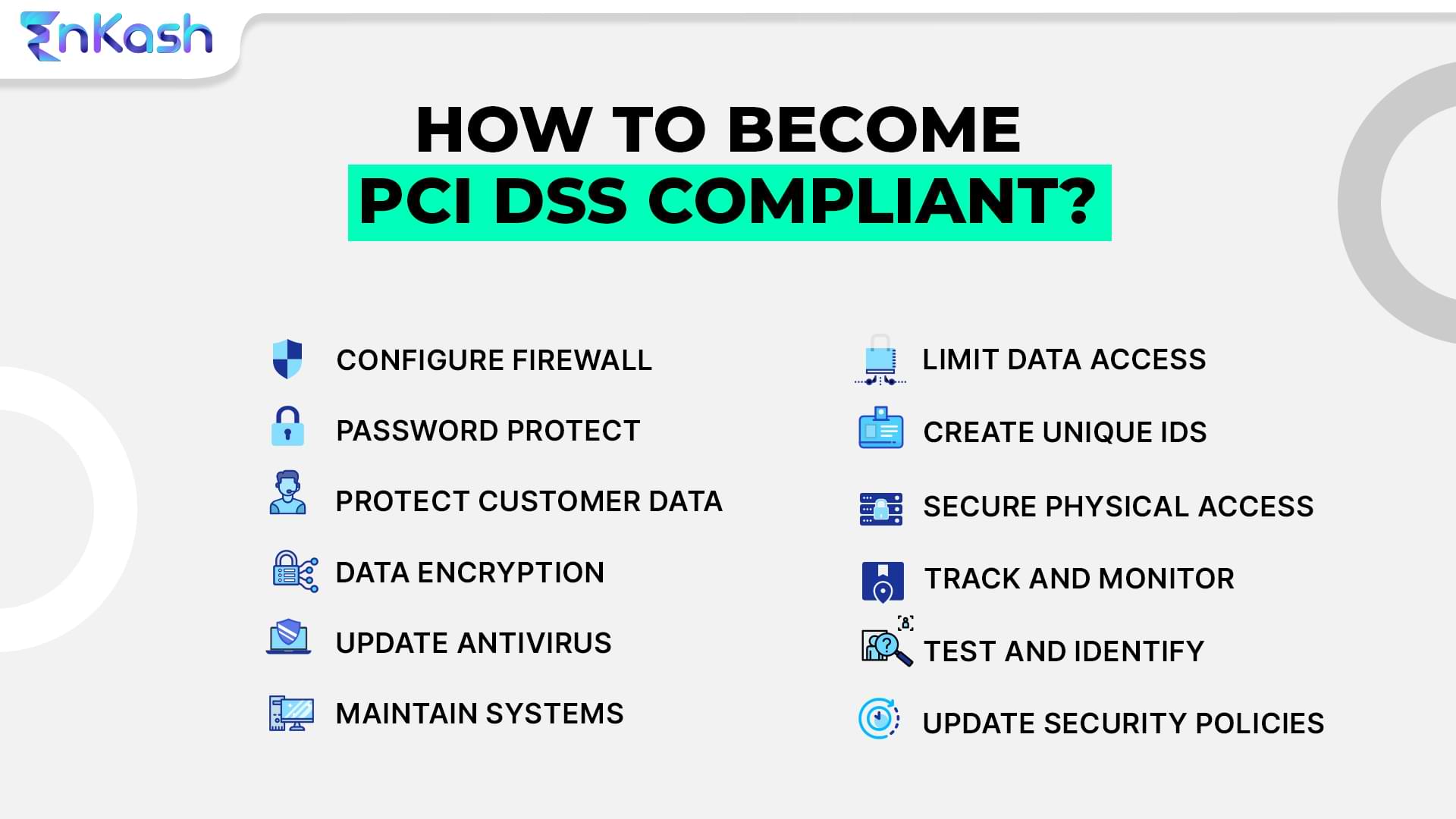

Here are the 12 steps to comply with PCI DSS:

Protect cardholder data with the installation and constant maintenance of a firewall configuration

Change the defaults supplied by vendors for the security parameters and passwords

Always ensure that cardholder data is protected

Ensure that the cardholder’s data is encrypted across networks

Keep updating antivirus software and programs

Make sure that you develop and maintain secure systems and applications

Limit cardholder data access strictly based on a business requirement to know

Make certain that each person with computer access has a unique ID

Ensure that cardholder data’s physical access is restricted

Keep track of and monitor access to cardholder information and network resources

Constantly test your security systems and processes to identify and address any gaps Create and update a policy that will help your team to maintain information security

There can be severe consequences for not meeting PCI DSS requirements. Not only will it interrupt operations but also increase costs associated with operations, compliance, and risk management.

As an offering, a host of solutions related to spend management, EnKash is not only PCI DSS compliant but also SOC2 compliant.

The way we do business has changed a lot since the demonetization and the lockdown due to the pandemic. While the process of digital transactions has become more accessible, easier, and secure than ever, there are some areas that many of us may not be aware of even now.

In this blog, we will look at what chargebacks mean and why it is critical for all businesses to be aware of them, especially for startups and smaller companies. It is essential to learn about chargebacks, how to claim them (for customers), how to prevent them (for merchants), and other details.

What is a chargeback?

As the term suggests, a chargeback is the return of money to a customer, usually involving an online transaction using a debit or credit card. In most cases, it is a dispute that the customer raises with the bank that has issued the card, which, in turn, requests the merchant to reverse the payment.

Here are some examples of chargeback instances:

Example 1: The goods that the customer has received are damaged and the customer takes this up as a reason for a chargeback.

Example 2: Customer made the payment but it is not reflecting and does it again to ensure the transaction is complete. However, both payments go through and the customer ends up paying twice. This is another instance of a chargeback being raised.

Chargebacks vs refunds and how they are different. Often chargebacks are confused with refunds. But the fundamental difference between chargebacks and refunds is that refunds are claimed from the merchant and chargebacks are claimed from the bank.

In some instances, if the merchant or seller rejects the refund request, the customer may appeal to the bank to facilitate a chargeback. Usually, the process of chargeback takes longer than the refund.

What are the possible causes of chargebacks?

Poor quality or damaged product: A customer may often request a chargeback when the product quality is not as described at the time of purchase. Or if the product is different in terms of specifications from when the purchase was made.

Product shipping issues: When the product is lost or damaged during the shipping process or delayed beyond a reasonable time, then the customer may request a chargeback.

Delayed refund: The customer is not happy with the purchase and has requested a refund, which the merchant has either not responded to or refused, then the customer may request a chargeback.

Unauthorized card transaction: The customer may raise a chargeback when there is unauthorized or improper use of the credit card or debit card.

Technical issues: In some instances, there could be cases of incorrect or duplicate billing, for which the customer has paid more than the billing amount. In such instances, the customer may raise a chargeback request.

How do chargebacks affect the seller or merchant?

If a merchant or seller has too many instances of chargebacks, it is going not only to affect the merchant in terms of cash flow but also affect their reputation. What is more, there are penalties that are associated with the chargeback that will be applied, causing further damage.

How does the chargeback process work

What best practices can merchants or sellers adopt to avoid high volume of chargebacks?

The key to avoiding too many chargeback requests is to establish a solid infrastructure in terms of payment and ensure that all the goods and services delivered are of good quality.

The other best practices include:

Detailed information: Merchants or sellers need to provide detailed information about the order paid for, to the customer. This way any confusion about the quality, quantity, specifications, and pricing can be avoided.

Order confirmation: The merchant can also ask customers for an explicit confirmation of the order before starting the packing and dispatching processes. This way, any changes the customer wants can be made before dispatch.

Regular updates: In an online world where convenience is the key motivation, often mistrust also lurks behind the minds of customers. One of the easiest ways to mitigate this is by updating customers on a regular basis. Explicit information given upfront can help avoid chargebacks.

Take measures: Merchants also need to ensure that they keep a lookout for red flags like a repetitive pattern from customers or many cards being used for orders to be delivered to the same address, and so on.

Chargebacks are a part of online transactions and have been enabled to protect the interest of customers, but there’s a chance it can be misused. Information updates, ethical business practices, and robust technology can help optimize the occurrence of too many chargebacks and minimize the associated costs.

Merchant category codes (MCC) are 4-digit numbers that are used by credit card issuing authorities to assign categories to the transactions that customers have done using the card. The MCC is listed in ISO 18245. MCC can be assigned by the type of merchant or by the name of the merchant.

To find the complete MCC list, check this blog: MCC list

How is MCC connected to corporate cards?

Corporate credit cards are issued to businesses rather than individuals and can be used specifically for incurring business-related expenses. Often businesses use their overall credit limit to issue credit cards of smaller amounts to their employees to decentralize payments and ensure a certain level of freedom. Enabling employees to pay for certain business expenses ensures that payments are made on time, and reduces the burden on the finance department.

Specific usage

However, there need to be some restrictions on the way corporate cards are used to ensure that there is accountability and transparency. Corporates often ask the card-issuing authority to restrict the usage to certain merchant categories and this is where merchant codes come into play.

Merchant codes are used to limit the type of transactions that customers can do using a particular card. For example, fuel cards are issued specifically to be used to buy fuel for vehicles. The company may issue fuel cards to its employees out on the field for business purposes and in such cases, the card can be used only to purchase fuel.

Chargebacks

A chargeback occurs when the electronic payment is reversed to the payer for some reason or due to a dispute raised by one of the parties. However, certain MCC codes do not offer chargeback protection to customers.

Convenience fees

Not all businesses can impose a convenience fee on credit card transactions. The MCC code of your company helps determine whether you will be allowed to impose a convenience fee for card transactions or not.

Rewards

Based on the type of credit card that the customer is using, the rewards could differ based on the MCC codes. This differential can motivate customers to frequent certain businesses or outlets.

Believe it or not, some merchant category codes are considered risky and will not be accepted by certain credit card companies. However, some companies specialize in processing high-risk codes and these companies undertake the assessment of risk and go ahead with the processing with certain conditions.

MCCs are also used to report tax issues, track promotions, and gather data on the buying patterns of customers. MCC is also used to determine the transaction percentage a business will have to pay the processor of the credit card transaction.

As Asia’s 1st and largest spend management platform, EnKash helps its customers manage corporate cards along with other financial transactions like collections, expense management, and more. We believe in equipping our customers with the ability to spend smart and save more using corporate cards. Whether it is restricting the kind of spend or the best rewards possible, you will be able to manage all these on our platform.

Virtual banking has penetrated the large-scale sector, and every small-scale and medium-scale business is also moving towards virtual banking. Virtual bank accounts are trending because of features such as an extra layer of security, real-time transaction monitoring, and virtual cards to streamline transactions. For the B2B sector, virtual bank accounts are a boon. But many businesses are still apprehensive about using these services, and we are here to help them realize the benefits of doing so.

So, if you are also wondering what is a virtual account number or what is a virtual bank account, how it is different from a traditional account, its benefits, and how you can open one, keep on reading!

Understanding the intricacies of what is a virtual accounts

As the name suggests, virtual bank accounts operate entirely online and can be accessed through mobile or desktop. The virtual account is linked to a primary bank account, and a system-generated account number is provided, masking the key account number. These virtual accounts cannot be traced to the primary bank account by people other than the account holders, which offers the company an extra security layer from online fraud or theft.

Meaning of what is a virtual account is really easy. Virtual bank accounts are easy to set up and can be used for various purposes, such as paying vendors, receiving funds, making online purchases, and paying bills. Some virtual bank accounts may also offer features such as virtual debit cards, which can be used to make purchases at merchants that accept card payments, pay employees, and more.

Now that you know what a virtual account is, learn how it differs from traditional bank accounts. One of the key reasons businesses use virtual accounts is that they charge zero processing fees, helping companies save costs on bulk financial transactions. In case your business is also looking forward to expanding and exploring overseas markets, virtual accounts can be beneficial as they can be used as an alternative payment method.

Benefits of virtual account

Types of Virtual Bank Accounts

Virtual bank accounts have become increasingly popular due to their convenience, security, and cost-effectiveness. They are designed to cater to a variety of business needs, and each type serves a specific purpose. Here are the main types of virtual bank accounts:

Single-Use Virtual Accounts

These are set up to handle a one-time transaction, and therefore they are perfect for companies that have a sporadic need to pay for the occasional vendor or contractor’s work done for a client. For example, if a company pays a particular vendor or contractor for a specific project, it can easily create a one-time virtual account for the single payment. Once the transaction is done, the account can be deactivated. Single-use accounts are great for companies that want to treat specific payments as separate from other transactions, which offer a very secure and easy way to do it without having to maintain multiple accounts.

Multiple-Use Virtual Accounts

Multiple-use are these unlike single-use virtual accounts, which are designed to be recurring. This kind of account would suit businesses that would like to track regular transactions in terms of payments to suppliers, contractors, or service providers in order to conduct a repetitive financial flow. The great flexibility of having to make such regular payments by making use of the account without having to create a new one, makes it quite convenient to operate with. Using multiple-use virtual accounts makes everyday balancing of accounts simple, while at the same time it’s quite safe and legal when many payments are taken care of individually.

Escrow Virtual Accounts

An escrow virtual account is an intermediary where two parties deposit funds before completion of a transaction under agreement until fulfillment of certain terms. It is ideal for lofty business transactions, particularly when the transfer of payment is made contingent upon some service or contract completion. In a real estate transaction or a business acquisition, an escrow account ensures that one party does not run the risk of being defrauded or that the service is not completed satisfactorily. It further assures buyer and seller protection, since disbursement is only possible once specific per-determined criteria have been fulfilled.

Cross-Border Virtual Accounts

Cross-border virtual accounts, by offering a simple way to make payments and receive money from a different country for businesses operating internationally, do away with the difficulties and much higher costs associated with conventional banking channels. This is especially beneficial for organizations that require doing payments or may be receiving them in several currencies, making cross-border transactions simple and inexpensive. Virtual cross-border accounts provide a better platform for businesses in efforts to stretch worldwide.

Virtual Savings Accounts

There are virtual accounts that allow a business to earn a return on idle funds without doing straightforward transactions. Virtual savings accounts offer all the advantages of online banking coupled with the upside of passive income. Businesses can save their surplus cash in such accounts so that they are not pressed to come up with money whenever they need it, but they have the power to keep withdrawing and accessing the money whenever they want. Such virtual accounts ensure that businesses can maximize their finances by providing interest free from traditional savings accounts.

Features of Virtual Bank Accounts

Virtual bank accounts come with a wide range of features that make them highly attractive for businesses:

No Transaction Fees:

Unlike the traditional accounts, where there is a fee transaction for every payment or transfer, virtual bank accounts do free transactions and all the business activities will be economical with this facility.

Paperless Setup:

Virtual accounts can be opened online and paperless, and customers do not have to visit any branch at all to have an account set up within minutes.

Security Features:

Advanced security features such as two-factor authentication (2FA), encryption, and secure password policies are often included in virtual accounts to provide security against cyber threats.

Virtual Debit and Credit Cards:

Most virtual bank accounts give businesses virtual debit or credit cards for online purchases or payments without needing a physical card.

Transactions Monitoring in Real Time:

Companies will be able to monitor online in a secure place their transactions in real time, thus assisting them in managing cash flow and avoiding discrepancies.

Customizable Alerts:

Virtual accounts can have custom alerts set for certain actions when it comes to alerting, such as low balance or huge transactions. Therefore, businesses will always know their financial position.

No Minimum Balance Requirement:

Today, very few virtual bank accounts have a minimum balance requirement like traditional bank accounts; thus, these accounts can be used flexibly to manage business funds.

Difference between a virtual account and traditional bank account

Listed below are the key differences between virtual and traditional bank accounts:

No physical branches

Unlike traditional bank accounts, virtual accounts exist only online and do not have any physical branches to carry out operations.

Easy account setup

While setting up a traditional bank account, you may have to visit a bank branch, fill out a form, and submit it to the bank official, whereas when we think of what is a virtual account can be created online with paperless KYC.

Accessibility

Traditional bank accounts can be accessed through multiple channels, such as bank branches, ATMs, bank applications, and net banking, whereas virtual accounts can be accessed through mobile or desktop.

Transaction fees

Traditional bank accounts charge transaction fees for making payments through UPI or NEFT, whereas virtual bank accounts do not charge fees.

Security

Both traditional and virtual bank accounts are subject to federal regulations and are required to have specific security measures in place to protect customer information and funds. Whereas, virtual bank accounts may have additional security measures, such as two-factor authentication, to protect against online threats.

Benefits of Virtual Bank Account Number

Virtual bank account numbers bring multiple advantages to businesses in terms of security, cost-cutting, and efficient financial management. The following are the main advantages:

Increased Security

One of the biggest advantages of having virtual bank accounts is increased security. A virtual account number is not directly related to the primary bank account; hence, it provides an added layer of security. This reduces fraud and online robbery since cyber thieves cannot access the main account through the virtual account.

Economically Beneficial

Virtual accounts tend to be free of processing fees; this is beneficial compared to traditional bank accounts that charge transaction fees during payments. For business entities that regularly engage in high volume transactions, this would translate into massive savings, reducing the overall cost of operations.

Effortless Cash Management

With the virtual bank accounts, it is possible for businesses to open as many bank accounts as they want for payments to vendors, employees, or even subscriptions. This will greatly help in organizing the revenue and making tracking the movement of cash easier, and help avoid confusion concerning where the fund allocations are directed.

Easy-to-use

Virtual account access can be gained via desktop or mobile devices so that business can have the flexibility to manage their finances anytime and anywhere. This is particularly useful for multinational companies or businesses requiring constant access to financial information.

International Expansion

Yet another benefit is for those considering international expansion for their business. The virtual accounts will allow easy transacting across borders without the need to maintain several local bank accounts. This becomes a lot easier and more efficient in operations and costs.

Real-time monitoring

Instead, it gives such companies a window of real-time transaction monitoring. Henceforth, the company can effectively keep track of incoming payments, ensuring they are processed when due. In this way, it hosts reduced errors associated with processing and clear operational flow in finances.

Advantages of virtual bank accounts for businesses

Moreover, to help you understand what is a virtual account number in detail, let’s learn about its advantages. A virtual bank account helps businesses simplify their cash management and offers several other benefits, as mentioned below:

Businesses can allot different virtual accounts for vendors, freelancers, utility bills, and subscriptions to streamline transactions

Facility to accept payment via various modes such as UPI, NEFT, RTGS, IMPS, and QR

With the proper documentation of each transaction, there are zero chances of manual error

Ability to build a separate wallet for consumers to receive, send, or even request funds

Can use the virtual account as an escrow account to protect the business from online fraud

Significant savings on maintenance charges, transaction fees, and minimum balance fees

Quick transactions and confirmation to ensure timely payments to service providers to maintain healthy business relations

How can you open a virtual bank account?

Knowing what a virtual account is is not enough. You should also know how to open a virtual bank account and enjoy its benefits thereafter. Below are six easy steps to open a virtual account:

Open the website and log in with all your information

Fill in the personal information and submit the identity proof, including PAN card, voter ID, Aadhaar card, and other details

Sign the disclosure agreement after reading the terms and conditions

Upon completing the procedure, you will get a virtual account number

Transfer the amount to the account from your existing account and link the cards

Now start the transaction as required

Here, you can monitor all the data from the dashboard from their online platform. You can limit and monitor transactions, get certain rewards, and even block the account as per your will. Furthermore, you can also access archived data at any time and anywhere.

In case your company is planning to launch any credit card or prepaid card programs and needs a virtual account to transfer funds to other accounts, let EnKash assist you. We offer virtual bank accounts powered by reputed banks. Having a virtual bank account will take away most of your worries related to bills and invoices, and every payment will be automated.

Now you know what is a virtual account and opening a virtual bank account is easy and hassle-free as the entire process is paperless. Once you log in to your account and complete all the procedures, including verification, you will instantly get your virtual account number and access. With EnKash, all your data is protected and secured. So, what are you waiting for?