Social media is no longer something that people use for social interaction, but an important part of your business arsenal. And the best part is that you can use it for free especially if you take a smart approach to how you share content online. As a smaller business or a startup, often the struggle is to always do more and reach more customers with the minimum effort possible.

Social media marketing when done right can make all the difference to your business, your brand, and the way customers see you. Your social media strategy should consider the channels that you use and the kind of content your customers prefer. For instance, if you are selling to other businesses, then the channel that resonates most with them could be LinkedIn.

And if your business is better off visually represented, then Pinterest is the way to go. Complex technical jargon or product information is easier to consume in video format and YouTube can be a good option to work with. Facebook and Instagram are good channels for building a human face for your brand.

The conclusion is that social media is here to stay and needs to be included in your overall marketing strategy. Here are the main benefits of social media.

Social media marketing benefits for small businesses

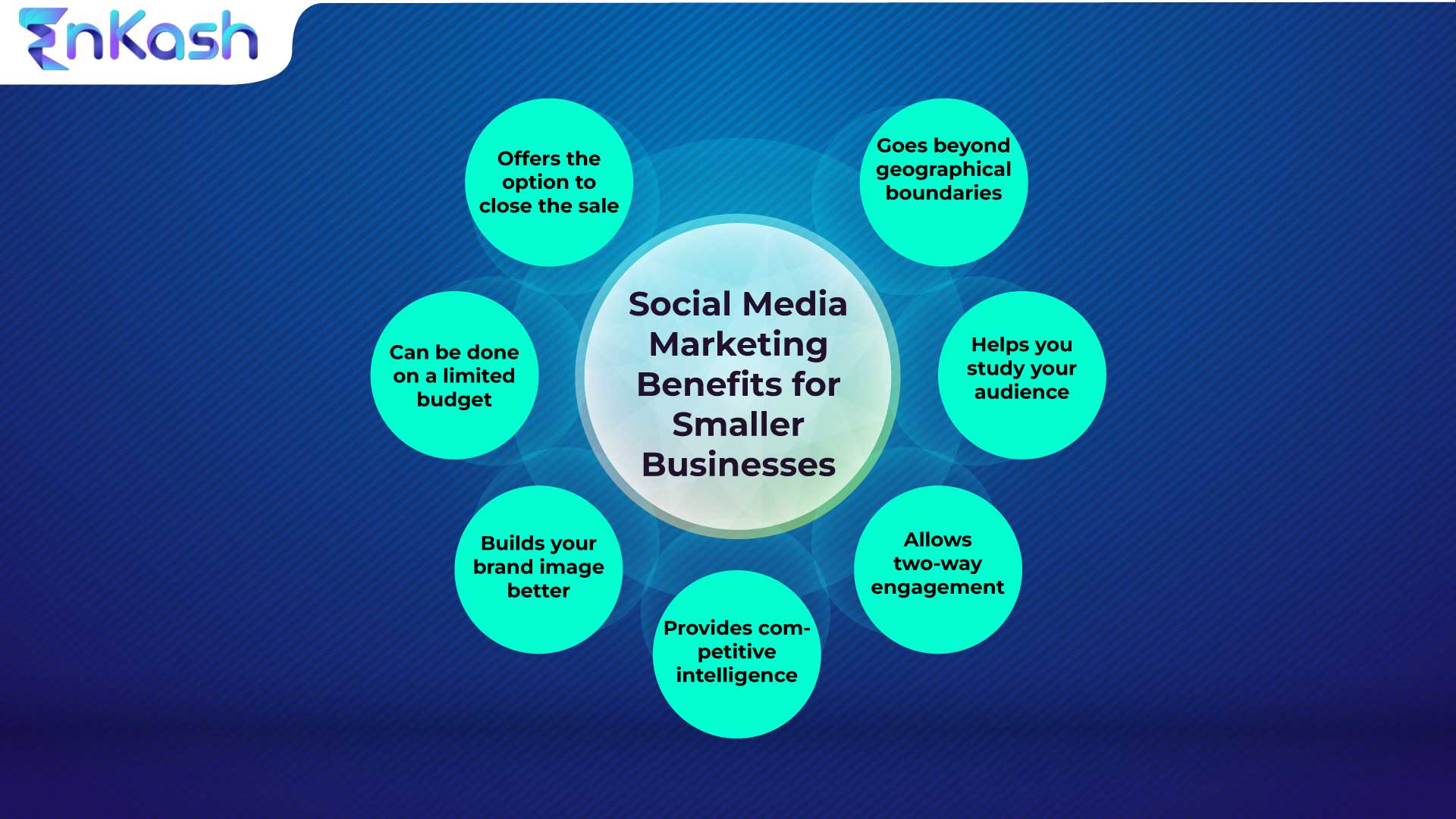

Social Media Marketing Benefits for Smaller Businesses

Getting results from your free social media efforts can take some time but it is well worth the effort that you put into it.

Goes beyond geographical boundaries

When it comes to social media for your small business, you have the freedom to choose the location where you want your content to be shown for paid advertisements. For organic efforts, too, you can choose to subtly restrict the geography or allow the content to be universally viewed. This can help with your expansion plans in the long run.

Helps you study your audience

Social media is one of the ways you can listen to the conversations your customers are having and study how they live their lives—both personally and professionally. For instance, you can study what your potential customers have to say by becoming part of forums they are most active. If you are selling finance software and join a forum for the CFO’s office, then you can get information to tweak your product and messaging as per the discussion there.

Allows two-way engagement

In today’s world, customers’ voice is loud and clear. Customers like to express their feelings—both positive and negative on social media. The good news is that you can easily address their concerns or express your gratitude on the same platform. Doing this can help you build your brand and create a positive image for your business.

Provides competitive intelligence

While you plan to be on social media, so will your competitors. Often the best insights and intelligence can be gained from social media pages of your competitors. You can not only gain insights into the way they work but also get insight into how their customers feel.

Builds your brand better

Social media also offers you to showcase the human side of your brand, like employee activities, CSR, and more. All these factors are critical to today’s customers and will help create a positive image of your brand across the web.

Can be done on a budget

You need not plan a huge budget for your social media marketing. A mix of paid and free campaigns with smart content will work easily for your social media plans. All you need is to orient your marketing team to start thinking about how they can use their content to resonate on social media.

Offers you the option to close the sale

Today social media offers you many options like allowing you to sell or teach customers how to use your product. When you use social media effectively, you will find that customer satisfaction goes up and the cost of post-sales customer service goes down.

As you can see, social media is a useful marketing tool for your business, no matter the size. However, as a smaller business, you have to make the right decision whether it is your social media marketing plans or your financial solution partner. At EnKash, as Asia’s 1st and smartest spend management platforms, we have been empowering small businesses like yours to reach their fullest potential with our fintech products.

Udyog Aadhaar, now known as Udyam Registration, is a 12-digit Unique Identification Number that facilitates registration for the small business sector and is a crucial initiative for Indian small and medium enterprises (SMEs) seeking growth and government support. It was issued by the Ministry of Micro, Small, and Medium Enterprises (MSMEs) of the Government of India in September 2015, and it facilitates a hassle-free, paperless online registration process. The reason behind Udyam registration is to boost the SMB sector in India.

What’s New with Udyam Registration

Mandatory Migration

As of 2023, Udyog Aadhaar registrations are no longer valid. All businesses need to migrate to the Udyam platform, to continue enjoying the benefits. If the entrepreneurs fail to migrate to Udyam Registration, then UAM will not be valid, and they will be required to register again for Aadhaar Udyam Registration.

Simplified Categories

The new registration system classifies businesses into three categories (Micro, Small, and Medium) based on their annual turnover and investment. This simplifies the process and ensures accurate classification

Enhanced Benefits

Udyam registration unlocks a wider range of government schemes and benefits, including easier access to credit, subsidies, and tender participation

Key Benefits of Udyam Registration

Hassle-free online registration: The process is completely online and free, requiring only your Aadhaar number and basic business details

Multiple registrations: Entrepreneurs can now register multiple businesses under one Udyam number, simplifying management

Self-declaration: No documents or proof are required beyond your Aadhaar, promoting transparency and ease

Government tender preference: Registered MSMEs get priority consideration for government tenders, increasing business opportunities

Faster payment protection: Udyam registration helps secure protection against delayed payments from buyers

Access to schemes: Unlock various government schemes and financial assistance programs

Credibility enhancement: Udyam Registration acts as official proof of your business existence

Documents Required

The following details are required for registration:

Name of the Owner

Category

Name of Business

Type of Business

Official Address

Date of Commencement

Details of Previous Organization (if any)

Bank Details

Number of employees

National Industrial Classification Code (NIC)

Amount invested in Plant & Machinery

Details of Industry Centre (DIC)

Udyam Registration Process

Before this, a lot of paperwork was needed to start a business and get MSME registration done. Two forms were required to be filled: Entrepreneur Memorandum-I and Entrepreneur Memorandum-II (EM-II). However, Udyog Aadhaar Registration simplified this process for the MSMEs to avail of government schemes in the form of subsidies, loans at a low-interest rate, and more.

Step 1: Visit the official Udyam Registration Portal

Step 2: Enter the 12-digit Aadhaar no. and name of the entrepreneur

Step 3: Click on ‘Validate’ and ‘Generate OTP’

Step 4: Enter the OTP received on the registered mobile number

Step 5: Once the verification is successfully done, fill out the form with all the relevant details

Step 6: Review the form and click on the ‘Submit’ button

Step 7: Enter the OTP again received on the mobile number

Step 8: Click on ‘Submit’ once for the final submission

Note: No registration fees is charged for this process. You can simply download the Udyam Registration Certificate upon submission of the form.

In case you do not have a valid Aadhaar Card, you must immediately apply for Aadhaar enrolment as the MSME- DI, or DSC will file your application based on your Aadhaar enrolment ID slip or any other supporting document such as PAN Card, Voter ID, Driving License, Passport, etc.

Conclusion

The Udyam Registration platform represents a significant step forward in simplifying and streamlining the process for small and medium enterprises (SMEs) in India. Whether you’re a seasoned business owner or just starting out, taking advantage of Udyam Registration is crucial to unlocking government support, boosting your credibility, and securing exciting opportunities for growth in the dynamic Indian market.

FAQs

Do I need to register again if I already have Udyog Aadhaar?

Yes, all Udyog Aadhaar registrations became invalid in 2023. Migrating to the Udyam platform is crucial to continue enjoying the associated benefits.

What documents are required for Udyam registration?

The process requires minimal documentation. You’ll need your Aadhaar number, basic business details, bank details, and National Industrial Classification Code (NIC).

How long does the Udyam registration process take?

The online process is quick and efficient. With all the information at hand, you can complete it within 15-20 minutes.

What are the key benefits of Udyam registration?

Benefits include easier online registration, access to government schemes, faster payment protection, tender preference, and enhanced credibility.

Where can I get help with Udyam registration?

The official Udyam website offers detailed information and support resources. Additionally, MSME helplines and industry associations can assist you.

Ever wondered why so many small businesses and startups collapse in the very beginning? Well, this might happen due to a plethora of reasons and one of the main reasons might be a failure to have proper HR practices and policies for systematically running a business. Many small businesses misjudge that HR management is not an essential part of achieving business goals and ignore this role to the core.

However, in this blog, we have compiled a list of the best HR practices for small businesses to help the business and the HR departments focus their efforts on these HR policies and practices to increase employee engagement, improve retention, and much more.

5 Best HR Practices for Small Businesses

HR Practices are a set of plans, principles, or ideas accepted by all the employees in a company offering them the best business execution. This is irrespective of which employee and the designation an employee holds in the organization. Moreover, these HR practices mostly revolve around the overall development of employees and aim toward the growth and expansion of the organization

In simpler words, good HR practices refer to strategic human resources processes that include streamlining the hiring process, performance evaluations, and much more.

Matching the company’s needs with employee expectations

A Human Resource team is responsible for balancing the expectations of the company and its employees to create a positive work environment. This HR practice will help the employees meet business goals smoothly, especially when it’s a small business. To cater to employee and company needs, it is essential to find the right balance of structure and flexibility as well. Employees always need clear and defined parameters for their projects, ways of working, and communication to fully sync with their managers and subordinates to meet business objectives.

Implementing Transparent and Effective Communication

This is one of the most important and good HR practices that every small business must adhere to develop a favorable reputation among its employees and beyond. Transparency and effective communication evoke a sense of trust and also help the employees cope with organizational change, especially in small businesses where the team processes, objectives, and functions change quite frequently.

Offer Employee Training at Regular Intervals

Under the HR practices and policies for small businesses, offering employee training by the HR team at regular intervals is very crucial for building their confidence and further improving their performance in the long run. Some of the types of training include sales training, management training, learning about new technologies and industry updates, and much more.

Fair Employee Performance Appraisals

It is imperative to have a fair employee performance appraisal as it is considered an essential component of a successful business. Not only this, but it also improves employees’ productivity and efficiency. All of this can only be done when the managers have clear feedback to the employees regarding their strengths and weaknesses. Moreover, a fair appraisal cycle can only take place when the employers consciously remove any kind of prejudice against the employees and evaluate them objectively.

Making Offboarding Simpler and Smooth for Employees

No employee stays in one company forever. When the employee leaves a lot of exit formalities are done such as a laptop, ID Card, key submission, and other documentation processes. A good HR practice is not limited to hiring the right people, implementing leave policies, working on a code of conduct, and more. It is also responsible for making the offboarding of employees smooth and easy similar to the onboarding process. An electronic employee HR checklist makes it easy for both the HR and the employees to save time and resources.

Final Words

Stating the obvious, every employee is the backbone of every small business. When HR follows the policy of ‘putting its employees’ interest first’ they meet the business goals smoothly without much hindrance. When HR proactively works towards catering to the needs of its employees, they also in return work with great dedication and determination. Such HR practices and policies, when created, undoubtedly improve employees’ competencies for improving the business workflow.

A Permanent Account Number or widely known as a PAN number, a 10-digit alpha-numeric unique number is one of the essential documents for tax submission by individuals, and organizations be it big or small if operating in India. Not only this, a business PAN Card is an essential document even for Indian-based businesses generating income in foreign premises for various purposes.

In this blog, we will talk about the simple process of how to apply for a company PAN Card, the documents required, and more.

Key Highlights of Business PAN Card

Form 49A must be filled by companies incorporated in India to avail a new PAN Card.

PAN Card can be applied through the official portal of NSDL.

The Certificate of Registration issued by the registrar of companies can be used as Proof of Identity and Proof of Address.

E-KYC option is not available for companies; hence the documents must be submitted physically.

The payment mode will depend on whether the firm is Indian or overseas.

Companies registered abroad or in India are obligated to pay tax on transactions conducted in India.

How to Apply for a Business PAN Card Online?

Follow these simple steps for the Business PAN Card application online:

Step 1: Visit the official website of NSDL and select Form 49A/Form 49AA from the ‘Application Type’ dropdown menu.

Step 2: From the next dropdown menu, select ‘Company’ as the category for PAN

Step 3: Enter all the relevant details, such as the name of the company, date of incorporation of the company, official email address, contact number, etc.

Step 4: Enter the Captcha Code, and a token number will be sent to the registered email address.

Step 5: Enter your company’s registration number to proceed further

Step 6: Now, enter the source of income of your company. Select ‘Income from Business / Profession’ from the drop-down menu and select business type

Step 7: Enter the official address in the PAN database for communication purposes. All other contact details will be prefilled. Click on the ‘next’ button

Step 8: Enter the Assessing Officer (AO) Code designated based on the area jurisdiction of your location. Click on the ‘Indian Citizen’ option and then select ‘State’ and ‘City.’ You can now proceed to the documentation page

Step 9: The declaration must be signed. Enter your relationship with the company(Director /Authorized Signatory) and apply for a company’s PAN. Submit the application form. Once done. Upload all scanned copies of documents.

Step 10: Review your form, and if all the information filled is correct, submit the form.

Step 11: Make the payment by choosing the payment mode, such as Demand Draft/Credit Card/Debit Card/Net Banking.

Once the payment is successfully made, you will receive an acknowledgment receipt for tracking the company’s PAN application status. This receipt must be signed and sent to the NSDL office with a copy of the registration certificate and demand draft (if any).

Step 2: Fill out the form with all the required details and attach the supporting documents and the application form.

Step 3: Send the application form and the annexed documents to the nearest NSDL processing location.

Step 4: An acknowledgment slip will be given for further reference of the form submitted once you make the payment for the same.

Step 5: Company PAN Card application form will be sent to the official address once the documents are thoroughly reviewed.

Documents Required for a Business PAN Card

Below are the Company PAN Card documents required for availing a Business PAN Card number:

Companies

Certificate of Registration Granted By Registrar of Companies

Limited Liability Partnership Firms

Certificate of Registration issued by the Registrar of LLPs

Partnership Firms

Certificate of Registration issued by the Registrar of Firms

Trusts

Certificate of Registration/ Trust Deed granted by the Charity Commissioner

Association of persons (other than Trusts) or Body of Individuals or Local authority or Artificial Juridical Person

Registration Certificate/Agreement issued by Cooperative society registrar/ Charity commissioner/Any other authority or Certified document issued from either central or state government office

What is the Need for a Business PAN Card?

The Government of India made it mandatory for all entities (individual businesses, a company, partnership firms, a HUF, or trusts) for generating income in India to apply for a PAN Card for the following purposes:

Company PAN Card is essential for tax identity of the company as it acts as the reference number for the Income Tax Department.

The Income Tax Department can track all the financial transactions with the company PAN Card.

If the companies fail to avail a PAN Card and are generating income, it is considered that the companies are trying to hide information from the government. Hence, a Business PAN Card is important.

It helps fill the Income Tax returns and avail various types of invoices, remittances, bills, etc.

If the company does not have a PAN Card, the government can levy a withholding tax which might be more than the entire payment of the invoice.

As a small business or startup, you are often faced with managing many aspects of your operations with limited resources. As a result, you may miss some vital aspects not directly connected to the development of your core business, such as human resource management (HR management).

For instance, some compliance-related tasks cannot be ignored. If you do so and this is discovered, it could result in penalties, loss of business reputation, and other dire consequences. When dealing with certain entities, either within India or abroad, they require the company to comply with local HR laws before they sign a contract with you.

In this article, we will examine the HR compliance checklist that you as a startup or small business owner should follow.

What is HR Compliance?

HR compliance is the concept of following the relevant laws and regulations surrounding the conduct, management, and administration of employees in an organization. Such provisions are aimed at safeguarding the rights of employees, ensuring equal opportunities at the workplace, and keeping the organization’s activities within the law. Compliance covers a broad scope of aspects such as payroll and employee benefits, compliance with safety practices, working hours, recruitment, and taxation.

In the case of new enterprises or small companies, HR compliance is very important for preventing potential legal suits, penalties, or loss of reputation. It is important to ensure that the organization adheres to the various local and national employment practices while at the same time promoting a conducive work environment. It entails ensuring that the policies and actions of a firm with respect to its employees are consistent with the relevant employment laws such as those related to taxation, discrimination, benefits, and health safety.

HR compliance is a continuous exercise, therefore businesses are expected to cope with the changing labor laws in the economy. When start-ups take care of the HR compliance requirements, they create a positive environment for growth and expansion, promote employee morale, and minimize any legal risks that may threaten the organization.

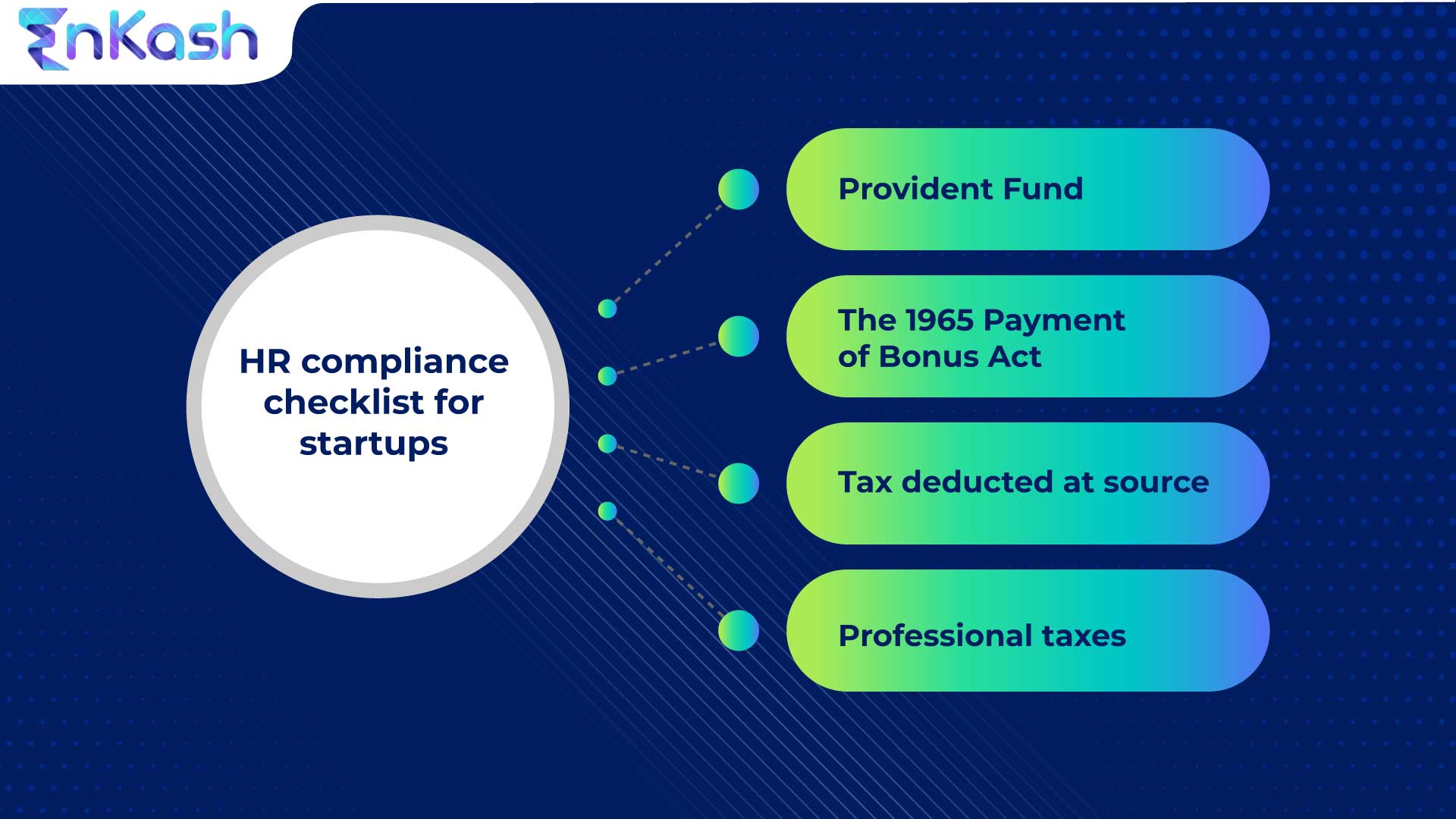

Here’s the checklist that you need to adhere to:

Why is HR Compliance So Essential?

HR compliance is crucial in ensuring that employees are protected as well as in ensuring the success of the business entity. It makes certain the company practices its operations legally, the work environment is safe and just, as well as the relationship between the employees and the employer is cordial. This is why HR compliance is so essential.

1. Avoiding Penalties and Fines

In a business structure where the human resources unit is not compliant with the legal requirements, there are serious implications that are attached for instance loss of business money through payment of penalties or even lawsuits. For instance, payment of wages below what is required by law, tax evasion, and violation of health and safety codes could lead to huge fines, depending on the extent of the violation. For start-up level and small businesses, such penalties could be very adverse economically, taking the focus off the business development and expansion

2. Safeguarding the Company’s Reputation

When a business operates within the requirements of the law and meets labor regulations, such a business is perceived as responsible and dependable. This kind of image can encourage more business, attracting clients, investors, and even job seekers. On the contrary, a negative image because of non-compliance, for example, can ruin the company so much that there will be a loss of business.

3. Improving Employee Satisfaction and Trust

Working in a workplace that is compliant with the laws and standards makes the employees feel appreciated and encourages them. When companies follow labor codes and pay the necessary portion for benefits, it shows that the enterprises care for the employees. This kills work-related stress but nurtures loyalty hence decreasing the turnover rate. An environment that encourages compliance also promotes trust, a sense of safety, and openness, which are all factors that contribute to productivity and growth.

4. Ensuring a Healthy Workplace

Ensuring HR compliance, it also means that all safety standards in the workplace are met thus the chances of people getting injuries or health conditions are minimal. When a safe working condition is maintained and the relevant safety regulations are followed, the business protects its workers from harm and lessens the chances of incurring expensive compensation claims or litigation from employees.

5. Ensuring Business Continuity

The business activities of such a business will be at risk of being interrupted by legal or financial issues. Firms that comply with the demands of HR are less exposed to risks such as audits and lawsuits that threaten their operations and lead to interruptions. Such stability is of utmost importance for new entrepreneurs and small enterprises trying to establish themselves in saturated markets.

Statutory Compliance in HR

Statutory compliance in HR refers to the mandatory legal obligations that businesses must meet to ensure that they are operating within the framework of the law. These legal requirements aim to safeguard the rights of employees and promote fair treatment within the workplace. Statutory compliance regulations differ from country to country and may vary based on state, industry, or region.

It can also be noted that in the case of India, statutory compliance involves the following:

Provident Fund Compliance (PF): Making sure that the way ordinary citizens save for their retirement, the government provides an Employer’s contribution and/or Employee’s contribution in terms of an employee’s provident fund, which is a compulsory retirement benefit scheme.

Employees’ state insurance or ESI: To ensure that employees have health and health insurance in case they are sick, injured, or involved in accidents; offered irrespective of whether it’s work-related or not.

Payment of Bonus Act: Any wage-earning employee whose wages are above the limit specified in the Payment of Bonus Act is entitled to a bonus that is calculated based on the profits of the establishment where he is working and the salaries of the employees in that establishment.

Gratuity Payments: Gratuity, often referred to as the ‘end of service’ payment, is given to employees upon resignation after serving the organization for a specified period.

Leave management: This includes abiding by the stipulated paid leaves which incorporate many public holidays, maternity leaves, and sick leaves as applicable under the law.

Occupational Health and Safety: The rules should be strictly adhered to in order to maintain proper organization and conditions at the workplace.

Inability to adhere to statutory clauses: It may yield penalties, fines, or audits. Thus, companies need to keep pace with the progression of these requirements to counter any risks and avoid legal actions.

HR Compliance Roles and Responsibilities

Labor laws and all the laws and regulations governing the treatment of employees are binding on every organization and Human Resource Management is at the heart of the organizational processes that facilitate compliance. The scope of the department includes numerous other aspects like policy formulation, record management, taxation and benefits administration, training, internal controls, and supervision of activities among others.

The HR department plays a key role in maintaining compliance through the following responsibilities.

Policy Development and Implementation: Every HR practitioner has the role of developing HR policies, revising them, and implementing them to the letter as well as respecting the labor laws. This pertains to safety at the workplace, leave, wages, and level of harassment and discrimination among other policies. In those cases when a law changes, the policies must change as well.

Employee Records Maintenance: HR must provide complete and current information and documents on every employee, such as signed contracts, payment details, attendance and leave records, tax information, and performance appraisals. Such documentation is imperative for compliance audits and tax submissions.

Tax and Benefits Administration: HR makes sure that the computation of tax withholding measures such as TDS which is tax deducted at source among other local taxes, and professional tax is done accurately and remitted on time to the respective bodies. Further, HR takes care of promoting officials’ statutory expectations, which include, but are not limited to, provident fund provision, insurance, and timely remittance of systems.

Training and Awareness: Strategies on how to inform employees of their rights and duties in response to employment laws fall within the HR scope. Training may also comprise anti-harassment or workplace safety and tax compliance external workshops. HR also makes sure that the senior managers and leaders are aware of the implications of the employment laws and how they have effectively enforced by the organization’s policies.

Compliance Audits and Reporting: Helps in carrying out assessments on labor laws and employment regulations’ observance within the firm on a regular basis. This also includes reporting to the appropriate parties including the government agencies and tax authorities wherever necessary. Regular audits help bridge the differences in compliance and enable the correction of current and future situations.

Risk Mitigation: Any threats in regard to compliance such as changes in tax policies, new laws, or hazards in the work environment are identified and dealt with by the HR. This enhances avoiding any potential lawsuits, fines, and even negative publicity to the organization.

By effectively managing these responsibilities, HR helps ensure that the business operates smoothly within the confines of the law while fostering a fair and compliant workplace.

What does the HR compliance checklist for startups look like?

The human resource department, while not directly connected to the business aspects of your company, plays a vital role in ensuring that your most important resources—are taken care of.

Apart from ensuring the well-being of employees with safe premises, offering market-relevant remuneration, and having practices like POSH, Leave Policy, Maternity Leave Policy, Travel Reimbursement Policy, and other such processes, there are some compliance-related aspects that you need to take care of. Here’s the checklist that you need to adhere to:

HR Compliance checklist for startups

Provident Fund

Provident fund or PF as it is called is a vital component of HR compliance. A part of the employee’s salary is (the employee can choose to have a percentage higher than mandated by the government) added to the provident fund and a contribution of the minimum percentage mandated by the government, comes from the company.

PF can be either state-run or companies can create a trust to manage provident funds. The PF amount can be withdrawn by the employee when he or she retires or is given to the family in case of the employee’s death. Non-compliance with PF has dire consequences for the business and should be taken seriously by companies.

The 1965 Payment of Bonus Act

The employer must provide a bonus to employees under this act if the business has 20 or more employees. The bonus is determined by the profits your company makes and the salary of the employee. If an employee works 30 days and has a salary less than INR 21000, then they need to be paid a bonus for the current financial year. The range for bonus payment ranges from a minimum of 8.33% to a maximum of 20%. Employees who are caught in a fraudulent act will not qualify for the bonus payment.

Tax deducted at the source

Tax deducted at source or TDS, as it is called is another aspect of HR compliance. The Central Board of Direct Taxes (CBDT) monitors this deduction. The income tax department considers the tax deducted at source when you file your taxes to ensure the right deductions have been made. You can consider perquisites like education allowance, medical allowances, investments, leave travel concession, etc while calculating TDS as these have an impact on the TDS amount.

Professional taxes

Each state government requires professional tax to be applied to individuals who earn in the state in any profession. The HR department must determine the applicable tax slab in the state where the business operates to ensure the correct amount is deducted. There are certain union territories and states in India where the professional tax may not apply and the HR team has to take this into account while deducting professional tax.

HR compliance is mandatory as per the law and can attract serious penalties if not followed. However, the responsibility of the department does not end there. There are many aspects, such as payroll, safety, welfare, etc., that an HR department must be mindful of.

At EnKash, Asia’s first and most innovative spend management platform, we are committed to extending support through our smart fintech solutions. We offer facilities like purpose-made cards to be used for HR-related functions like fuel, rewards and recognition, reimbursements, travel and entertainment expense management, and more. Visit our website to learn more.

Gratuity Act

The Gratuity Act applies to those employees who have completed at least five years of continuous service in an establishment. The main purpose of this Act is to ensure the financial stability and safety of employees even after they are no longer working with the organization whether on retirement, resignation, or any other reason. The calculations on the gratuity depend on the last salary drawn by the employee and the term (in years) served on the employee, therefore, gives nutrition after serving them for a long time.

Maternity Benefits

The Maternity Benefits Act obliges the employer to provide a female employee on maternity leave with twenty-six weeks’ paid maternity leave. This is effective for industries with 10 or more employees. This is beneficial to the female employees who may go on maternity leave without the fear of not having a salary throughout the period, thus concentrating on their health. Whereas it is imperative to respect the existing law, it is equally important for the promotion of women’s rights and employee welfare.

Labor Welfare

Labor welfare promotes the right to proper working conditions, limited weekly working hours, and access to welfare amenities, including health and recreation, to which individuals are entitled. It is a fundamental concern in ensuring employees’ healthy and productive workings. Ignoring the labor welfare policies may lead to penalties and destroy the image of the corporation which will affect the staff retention and loyalty in the long run.

Employee Contracts and Documentation

Having written employee contracts eliminates ambiguity in issues such as job descriptions, payments, benefits, and policies of the employers and employees. These contracts assist in minimizing conflicts by stating the intricate details of employment. Based on the documentation, the parties understand the relationship and its expectations which help avert or deal with disputes or legal issues

Employment Law

Employment Laws and Policies stipulate that the management should take proper care and protect the personal and sensitive information of its employees. This has become very pertinent especially as the value placed on an individual’s record has greatly risen. Using the Personal Data Protection Bill, no employee’s private details will be exposed to unwanted elements, which would in turn protect the firm’s reputation from possibly facing legal implications.

Health and Safety

Occupational health and safety rules should be strictly adhered to promote proper organization and condition at the place of work. This entails ensuring proper health and safety practices are observed, carrying out risk control surveys frequently, and providing appropriate protective equipment and facilities to the employees. In addition, regular medical examinations and compliance with health regulations help to reduce accidents and ill health in the workplace thereby promoting the safety of the employees and the organization.

Points to Remember for the HR Compliance Checklist

When it comes to the HR compliance checklist implementation, both startups and small businesses should take into consideration the following points:

Regular Updates: With the laundry list of compliance requirements, there is no doubt that some will be added while some will be removed. This therefore means that the checklist will have to be updated whenever any country’s statutes change or new laws come into play.

Employee Awareness: Every employee must know his or her rights and duties. In addition, everybody must know what is allowed and what is not in the organization so that there is no misunderstanding or non-compliance.

Proper Record Keeping: There should be perfect execution of all human resource services to make the records clear for purposes of audit and to prevent conflicts.

Regular Audit by External Parties: Conduct regular audits by third-party professionals to verify that all laws are observed.

Develop a Compliance Calendar: Implement a time frame within which strict deadlines will be imposed for every statutory obligation such as tax payment, filing returns, and necessary annual audits.

Why Do Startups and Small Businesses Need an HR Checklist?

Startups and small businesses typically operate with limited resources and may face a steep learning curve as they grow. One aspect that is particularly missed out in the early stages of growth is HR compliance. An HR checklist provides the ability to maintain employee-related issues and in themselves, the legal requirements of the business.

For instance, for a small business organization in this case, HR work-related cases assigned to HR personnel like tax filing, payroll, employee benefits health and safety, etc., can be said to be responsible. Learning from a checklist, a startup can be able to prevent normal HR functions from going wrong, mitigate some legalities in the process, and finally address all issues that need addressing about the business whether inclusive of all the requirements or not.

Some of the advantages of an HR checklist are:

Keeping everything in order: Assists in recording important HR-related activities and their respective deadlines.

Avoiding noncompliance: Ensures that all the legal requirements are fulfilled which helps to avoid incurring penalties.

Improvement of employee morale: Women and men in an organization are assured of equity and even entitlement to the Board a chance of benefits.

Facilitating activities: This diminishes the task of a small business person by providing a stepwise approach to HR activities.

In the end, a cost-effective hr checklist can help manage growth from the very beginning and prevent any legal issues associated with the business.

Components of an HR Checklist for Startups

An HR checklist for startups should consist of various components so that all the legal and regulatory obligations are adhered to. The following is an outline of what should be set forth:

Employee Documentation: Make sure that all the relevant documents such as employee contracts, offer letters, and background checks are available.

Payroll Processing: Making sure that wages, taxes, and benefits are calculated and paid correctly and on time.

Providing Fund (PF) Contributions: Making sure there is an employer and employee contribution to the provident fund.

Professional Tax Rates and Deductions: Following the state’s relevant tax and regulation based on the state of business.

Employee Benefits: Administering provided for health care, maternity, and sick leave insurance among other legally provided benefits.

Workplace Safety: Assurance of adherence to occupational health and safety procedures and measures.

Tax Filings: Adhering to tax regulations by calculating and deducting the correct TDS from employees’ salaries.

These components should be done periodically to reflect the changes in the laws and also to ensure the compliance levels are maximum.

What is the Purpose of an HR Compliance Checklist?

An HR compliance checklist’s primary aim is to offer a concise and systematic method of achieving compliance with the various legal and regulatory requirements that businesses face. For young and budding businesses, the HR compliance checklist is of the following importance:

1. Systematic Approach to HR Tasks

An HR compliance checklist aids in the accurate performance of important HR functions such as payroll administration, tax remittances, management of employees’ benefits, and even workplace safety, which is often a process of complex timelines or steps. It provides clarity for the HR department, ensuring they do not overlook any important tasks.

2. Minimizing Possible Fines

Adhering to the checklist allows businesses to be more forward-thinking and accomplish any assignments due before the timeframe expected, thus lowering the chances of failing to complete the task and incurring fines for noncompliance as a result. This assists in containing the legal and financial obligations that might jeopardize the existence of the business.

3. Streamlining HR Processes

The list enables the HR departments to be well-coordinated and effective. It assists in the control of routine HR functions, lessens the variation in difficult compliance issues, and cuts down on the workload. This frees the HR unit to handle other critical areas, such as employee engagement and development.

4. Protecting the Business

The list serves a further function as a safeguard to the business in that it helps to deal with concerns relating to legalities and finances. It also protects the business from threats due to non-compliance with labor, health, safety, and employee protection. The soundness of this protection is essential for the business’s viability over time.

5. Ensuring a Compliant Working Culture

In the end, every HR compliance checklist plays the role of fostering a working environment that is compliant, open, and free from any negativity.

What exactly is compliance in human resource management?

HR compliance is the process of keeping all your HR policy procedures in line with the laws, ethics, regulations, and any other factors that apply to your organization and modifying them in case there are new developments. It is one of the major functions within HR.

What is the checklist for compliance in human resources?

This is a checklist that helps employers ensure that they are complying with all the employment laws and regulations relevant to them. Its contents often include employment contracts, minimum wage, hours of work, equal pay and discrimination, data protection, health and safety matters, and policies relating to termination of employment.

How does HR compliance affect employee trust and satisfaction?

Adhering to HR compliance demonstrates care for employee rights, ensuring fair treatment, timely benefits, and a safe work environment. This fosters trust, loyalty, and higher job satisfaction among employees.

How can early-stage companies ensure HR regulatory compliance?

Early-stage companies can achieve compliance by:

Being aware of current employment laws and regulations

Keeping and updating all employee files

Performing compliance checks regularly

Establishing specific HR directives

Using HR management tools for payroll and tax compliance

Define Statutory compliance HR

It means complying with fulfilling the extensive legal requirements established by governing policies. This includes adhering to acts like Provident Fund (PF), ESI, Payment of Bonus, Gratuity, Maternity Benefits, and more. Learn more about statutory compliance in HR.

How is HR ensuring compliance?

The HR department outlines and puts into effect rules and procedures, keeps records of employees, manages health insurance, taxes, and other benefits, performs compliance checks, and creates educational programs for staff and management.

Provident Fund

Provident fund or PF as it is called is a vital component of HR compliance. A part of the employee’s salary is (the employee can choose to have a percentage higher than mandated by the government) added to the provident fund and a contribution of the minimum percentage mandated by the government, comes from the company.

PF can be either state-run, or companies can create a trust to manage provident funds. The PF amount can be withdrawn by the employee when he or she retires or is given to the family in case of the employee’s death. Non-compliance with PF has dire consequences for the business and should be taken seriously by companies.

The 1965 Payment of Bonus Act

The employer needs to provide bonus to employees under this act if they are a business with 20 or more employees. The bonus is determined by the profits your company makes and the salary of the employee. If an employee works 30 days and has a salary less than INR 21000, then they need to be paid a bonus for the current financial year. The range for bonus payment ranges from a minimum of 8.33% to a maximum of 20%. Employees who are caught in a fraudulent act will not qualify for the bonus payment.

Tax deducted at source

Tax deducted at source or TDS as it is called is another aspect of HR compliance. The central board of direct taxes (CBDT) monitors this deduct. The income tax department considers the tax deducted at source when you file your taxes to ensure the right deductions have been made. You can consider perquisites like education allowance, medical allowances, investments, leave travel concession, etc while calculating TDS as these have an impact on the TDS amount.

Professional taxes

Each state government requires professional tax to be applied to individuals who earns in the state in any profession. The HR department needs to find the slab in the state in which the business is to deduct the right amount. There are certain union territories and states in India where the professional tax may not apply and the HR team has to take this into account while deducting professional tax.

The HR compliance is mandatory as per the law and can attract serious penalties if not follow. However, the responsibility of the department does not end there. There are many aspects like payroll, safety, welfare, etc., that a HR department has to be mindful of.

At EnKash, we believe in extending our support through our smart fintech solutions. We offer facilities like purpose-made cards to be used for HR-related functions like fuel, rewards and recognition, reimbursements, travel and entertainment expense management, and more. Visit our website to learn more.

As a thriving business in today’s economy in India, you would have come across the term gig economy. According to Velocity Global, the global gig economy statistics show that the numbers are poised to rise from 43 million in 2018 to 78 million by 2023.

Often people may not be aware of the meaning of the gig economy in India and think that it is a concept that is not prevalent in our country. But that is far from the truth and there is a rise of the gig economy concept in India as well. And if you are the founder of a small or medium-sized business or a startup, then you must learn about the gig economy’s pros and cons. Let us dive deeper into the concept of a gig economy to understand what its impact is on smaller businesses.

What is gig economy?

A gig, by definition, is a small-term or short-term job that you pick up and work on. For instance, a specialty engineer who specializes in bridge structures may pick up gigs in the short term as and when a project requires his or her specialized expertise. An economy where more people are inclined to gigs or short-term freelancing jobs or contracts may be defined as a gig economy. In such economies, there are less long-term jobs and more gigs as the choice for employment.

What are the pros and cons of gig economy?

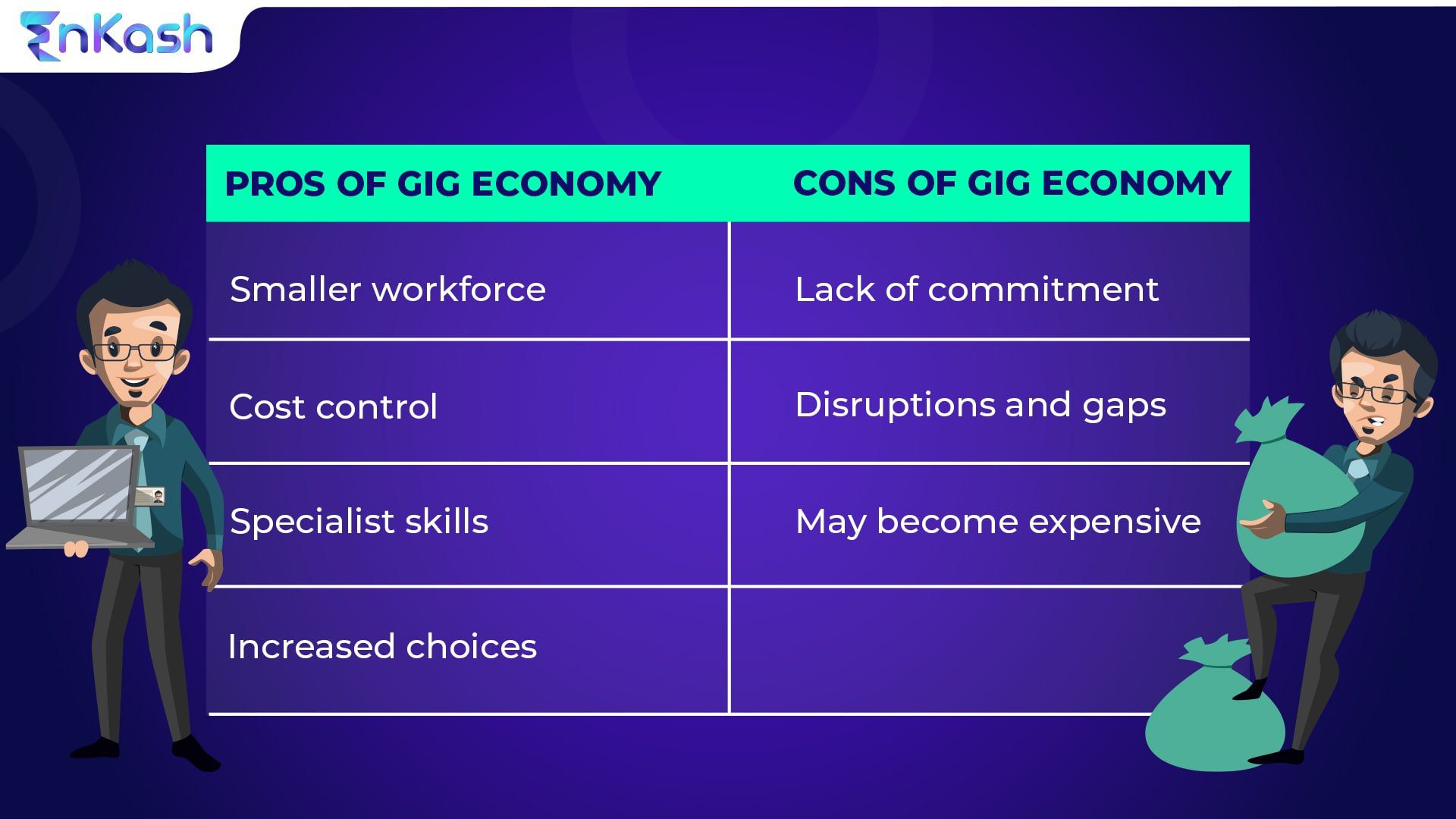

Gig economies are slowly starting to take over conventional employment, given that the younger generation is more inclined to this concept. Shorter attention spans, increased choices, and wanting to specialize are some of the reasons that encourage the growth of the gig economy. As with any other concept, gig economies have their own pros and cons. Let us take a look at some of them here.

Pros and Cons of Gig economy

Pros of gig economy

Smaller workforce

For companies that do not want to onboard too many full-time employees, gig workers are a good choice. They not only work with complete commitment during the contract period but need not be part of the long-term payroll.

Cost control

Gig workers, by definition will work for a shorter period and then move on, which means that the business has to commit to paying them for a lesser time period. Once the work is complete, there is no need to keep paying the employee in question.

Specialist skills

Many companies need a specialist with specific skills for a short time period and gig economies support that. Since gig workers are not committed to one employer, they can support your requirements without any waiting period.

Increased choices

Instead of only full-time employees or contractual employees, the gig economy allows companies to choose from increased options. Companies can appoint full-time employees for sensitive matters and take on gig workers in the short-term for project needs.

Cons of gig economy

Lack of commitment

The lack of commitment from the gig workers can often result in poor quality of work, especially towards the end of the contract. In some instances, the lack of commitment from the company can also result in issues for gig workers.

Disruptions and gaps

With an increasing number of short-term workforce working in a company, there can be disruptions in production and gaps in quality. This is especially in the case of manufacturing companies, where quality needs to meet certain standards.

May become expensive

Since gig economies operate on the concept of demand and supply, in some instances, gig workers may charge more. Given that gig workers are only short-term, they may feel the need to charge more, making it expensive for the company in question.

How is gig economy relevant to small businesses in India?

Small and medium enterprises or startups by definition have limited resources and often have to balance their limited resources against increasing demands. In such situations, the pressure to do more with less is always upon these small businesses. This, in turn, means there is a lot of pressure on employees to perform more roles.

The result is often poor quality goods, subpar customer experience, or even sometimes dangerous situations. But this does not mean that the smaller business should recruit more people to make up the difference. Doing so will tax their limited resources and reduce profit margins,

In such a situation, the concept of a gig economy with short-term specialist workers to support them is the right way to go. The smaller business gets the skillsets they require, but without adding the burden of increased payroll in the long run. Also, in some instances, when the employee they recruit may not be the right fit, and in such cases, there is a long process for separation. This concern is mitigated in a gig economy due to the nature of contracts.

Smaller companies also get to experiment with the right mix of skills in the gig economy before committing in the long term. As you can see, the benefits of the gig economy are numerous and will help small businesses grow with access to the right resources without a long-term commitment.

At EnKash, we have a number of fintech spend management solutions to meet the evolving needs of a business like yours. Click here to check out what EnKash, Asia’s 1st & smartest spend management platform has to offer you.

Technology has become an integral part of how everything works around us. As a result, all companies, be it startups, small businesses, or multinational companies, need a resource to execute, plan, and direct all the technical aspects of a business. This resource is widely known as a CTO. In this blog, we’ll dive into all the relevant details of the CTO’s roles, responsibilities, and skills for the substantial growth of the company.

Chief Technology Officer or CTO: The Definition

First, let us understand what is the CTO full form and CTO’s responsibilities. The CTO full form in the company is Chief Technology Officer. This person holds a senior designation in any organization and is mainly responsible for technology management within a company.

In other words, he or she is in charge of creating new technologies, new services, and products in the company considering all the industry factors and the technology changes by keeping in mind the short-term and long-term demands of the company. Moreover, a CTO is also responsible for the growth and expansion of the company.

How to become a CTO?

To become a Chief Executive Officer, one has to start the career by opting for a bachelor’s degree most probably in the IT sector, computer science, or information science. One can pursue a master’s degree in engineering or computer science, applied mathematics, and cybersecurity.

In a startup, if you want to work as a CTO, you will be given priority, if you are also well-versed in fields such as customer relations, marketing, and business management. This role requires a CTO to wear multiple hats to achieve company goals.

Furthermore, to become a CTO, the most essential thing is hands-on industry experience. Thus, before one takes on the responsibilities of being a CTO, lots of Chief Technology Officers start their careers working as lower-level managers and later grow to higher positions and then get promoted to the CTO role.

CTO Roles and Responsibilities

Below is the list of key responsibilities of a CTO in any organization. They are mainly responsible for:

Offering technical assistance to the company

Creating all the predictable outcomes by turning project execution into a controlled procedure

Strategizing cutting-edge ideas for driving the company’s growth

Identifying all the new technological assets that are appropriate for the company’s use

Creating cybersecurity measures to protect data and client information

Monitoring the key performance indicators and allocation of IT spending to assess technology metrics

Looking for partners/sponsors for investing purposes and communicating the technological strategies to them

Ensuring that all the corporate resources are efficiently used and distributed

Ensuring that the technology plan created aligns with the company’s objectives

Looking for partners/sponsors for investing purposes and communicating the technological strategies to them

Making all the leadership decisions primarily based on the company’s technological needs

Final Words

As you see, A CTO act as a bridge between businesses and consumers. This role is important in today’s time for providing customer-centric services and offering various customized software solutions. On the other hand, the key role and responsibilities of a CTO also depend on the size of your company, its budget, and its long-term goals as well as the nature of the transformation this person will be responsible for.

Did you know that the structure and category of your business can make a big difference when it comes to many aspects? Yes, it does. Whether it is the kind of capital you have to raise or the kind of orders you want to get, in terms of venture capital, or your liability in case required.

Each country has some distinctive types of businesses or categories and in this article, we will look at the different types of businesses in India. We will go deeper and discuss the pros and cons of each type of business and the one most suitable for you if you are starting a new business.

What are the different types of businesses in India?

Let us look at the different business categories that you can consider if you are starting a new business or considering restructuring your business.

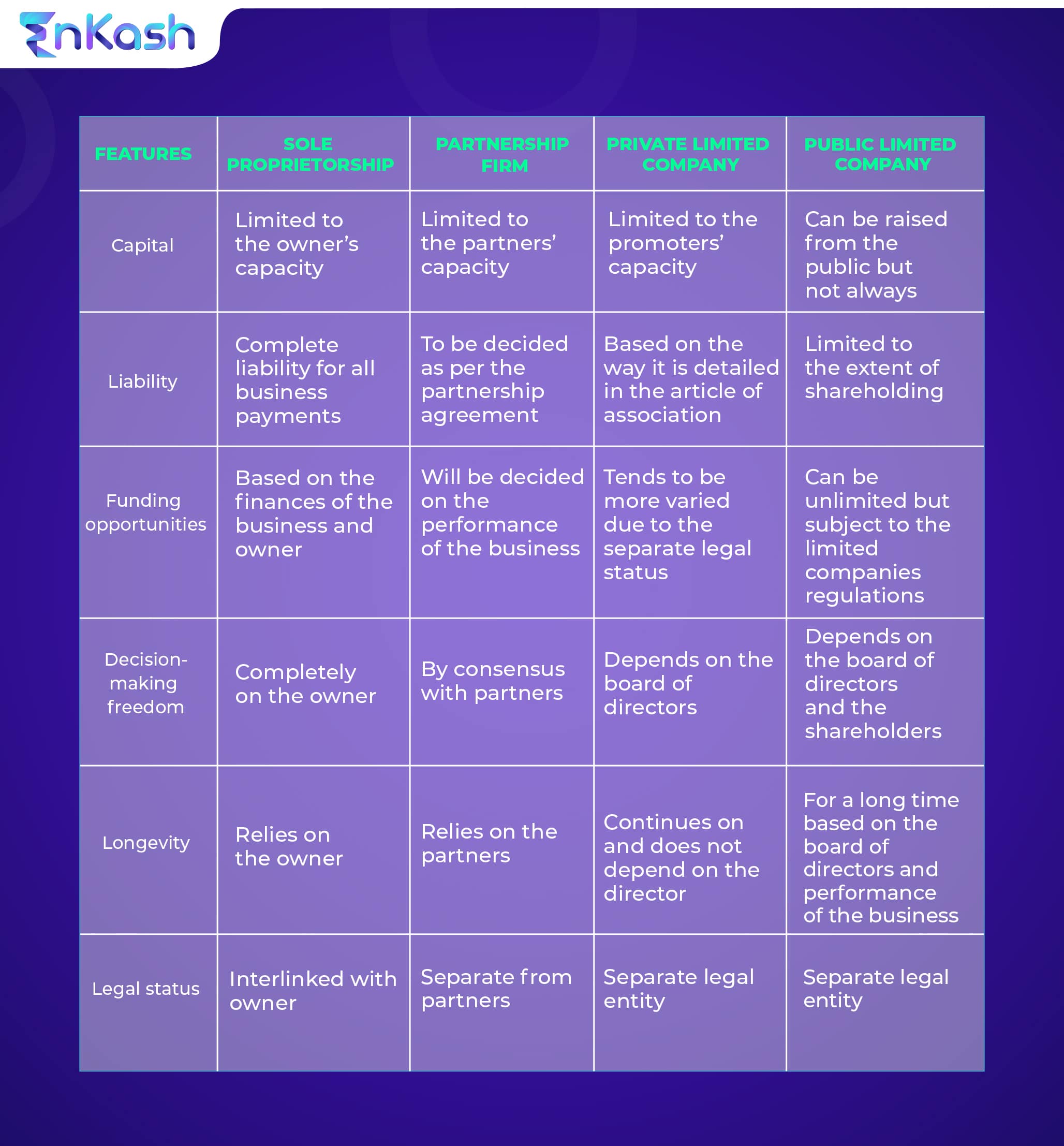

Private limited company

A private limited company has a lesser number of shareholders and the equity is defined as per the articles of association. In most instances, the transfer of shares is restricted and private limited companies generally cannot offer shares to the public.

Here are the main features of a private limited company:

Distinct legal existence

As opposed to a sole proprietorship, a private limited company is a distinct legal entity and is considered separate from the promoters. This, in turn, means that any legal action taken on the company need not apply to the promoters, though they do have some responsibilities. In the same way, a private limited company can sue others as a distinct legal entity.

Capacity to borrow

As a distinct business entity, the private limited company has the option to borrow on the strength of its financials. Banks are more likely to consider private limited companies as an acceptable entity for borrowings than other partnerships and sole proprietorship businesses

Option to exit

As specified in the articles of association, you may exit the business by selling your shares with other directors or promoters. Unlike a sole proprietorship, where this is not possible private limited companies offer you this option.

Partnership firms

In a partnership firm two or more people get together to form a partnership firm. The investments, the responsibilities, and the profit sharing is decided mutually by the partners and are entered into the agreement to use as a reference in the future. Though it is not mandatory to register a partnership agreement, it is advisable to do so. The liabilities are shared among the partners with no limits.

Here are some of the features of partnership firms:

Shared responsibility

Due to the shared responsibility for all aspects of a partnership, there is a cohesive approach to business, and this benefits and partners as well as the business.

Trust and synergy

Partnerships arise out of trust between the partners and the belief that each of them brings in their own skills and contributions. This, in turn, ensures that the partners have a lot of trust in each other and there’s a synergy in all their actions.

Ease of financing

Banks and financial institutions tend to be favorably inclined to finance partnership firms due to their performance and continuity in comparison with sole proprietorships.

Sole Proprietorship

As the name implies, sole proprietorships are owned by a single individual. As a result, there is no distinction between the legal status of the business and the owner in this case. This, in turn, means that a single person has ownership of all assets, liabilities, and profits of the business.

While sole proprietorship seems a good option for those who want complete control and ownership, it also has some disadvantages. Here are some of the main features of sole proprietorships:

Control

The complete direction of the business, the spending, and the way ahead are all decided by the owner. In case you want to retain complete control of your business, this is the way to go.

Flexibility

Sole proprietors have complete flexibility in the direction of their business or any other aspect since they are the sole authority. But this also means that any mistakes or errors are going to be the responsibility of the owner.

Finance

Since the owner of the business and the business are the same, there can be some hesitation when it comes to finding ways to finance the business. Banks and financial institutions often worry about the continued performance of the business and its ability to repay loans unless the financials and past performance of the business are strong.

Other types of businesses include Hindu Undivided Family, Limited Liability Partnerships, One Person Companies, Non-profit Companies, Joint Venture Companies, and Non-Governmental Organizations. All these are variants of the four basic categories of companies in India.

Public limited company

A public limited company has been defined as a company that is not a private company. The public limited company has to have at least 7 people with a minimum paid-up capital each. Many public companies are listed on the stock exchange and the shares of the company are traded on the stock exchange. Public limited companies that offer shares to the public are subject to a lot of regulations.

Here is a list of features of a public company:

Liability is limited

Since there are at least 7 members as shareholders on the minimum side and there is no limit to the maximum number of shareholders, the liability is limited to the extent of your share in the company.

More members

It is likely that if your business is a public limited company, then there are many members as far as shareholders are concerned. However, as a member of the board of directors, your responsibilities could be different from general shareholders.

Longer existence

A public limited company is a separate entity and is not affected by the loss or demise of a shareholder. And if well run, can enjoy a longer existence than other forms of businesses.

Bigger capital

As a public company, your company has more options and venues to raise capital or even float debentures to raise money for your business.

How to choose the right business type for your startup or small business?

Given below is a summary of the pros and cons of each type of business. You can make your decision based on your requirements and preferences for the well-being of your business.

Pros and cons of each type of businesses

At EnKash, as Asia’s 1st and smartest spend management platform, we specialize in supporting businesses like yours grow more, spend optimally, and save more.

When small and medium sized businesses or startups hear the term ‘CRM’ their usual reaction is to shrug and say that CRM is necessary for larger companies and not them. In this article, we will explore why investing in CRM is important and the importance of CRM software for small businesses. Let’s start by understanding what CRM stands for and what it does. The full-form of CRM is customer relationship management. As the name suggests the CRM software is used to manage customer relationships with ease.

The first thing to consider while deciding whether to invest in CRM or not, is by looking at the core of your business. And the core of any business is universal – the customer or customers. The better your relationship with your customers, the more likely it is for your business to survive and thrive. Given that logic, don’t you think investing in CRM is important? Yes, it is a substantial capital investment and will require a long-term finance arrangement. But it will also ensure that your business is more profitable.

What does CRM do?

A CRM helps you capture all the information about customers onto a common platform. Every interaction that any team in the company has is logged into the customer account. For instance, the marketing team has had the customer click on a link to download an asset. This will be taken as a marketing-qualified lead and nurture the customer with more information via emails.

Once the customer has opened the emails, consumed the information, and shown interest in a demo or discovery call, he or she is passed on the sales team. All the interactions and actions taken by the customer at each stage is recorded on the CRM. This enables the sales team to tailor their pitch accordingly. In the same way, once the sale is complete, all the customer-related information is stored in the CRM to ensure positive interactions, more sales, and so on.

Now that we understand that CRM can help you maximize the customer lifetime value, build a reputation as a customer-centric company, and improve overall profitability.

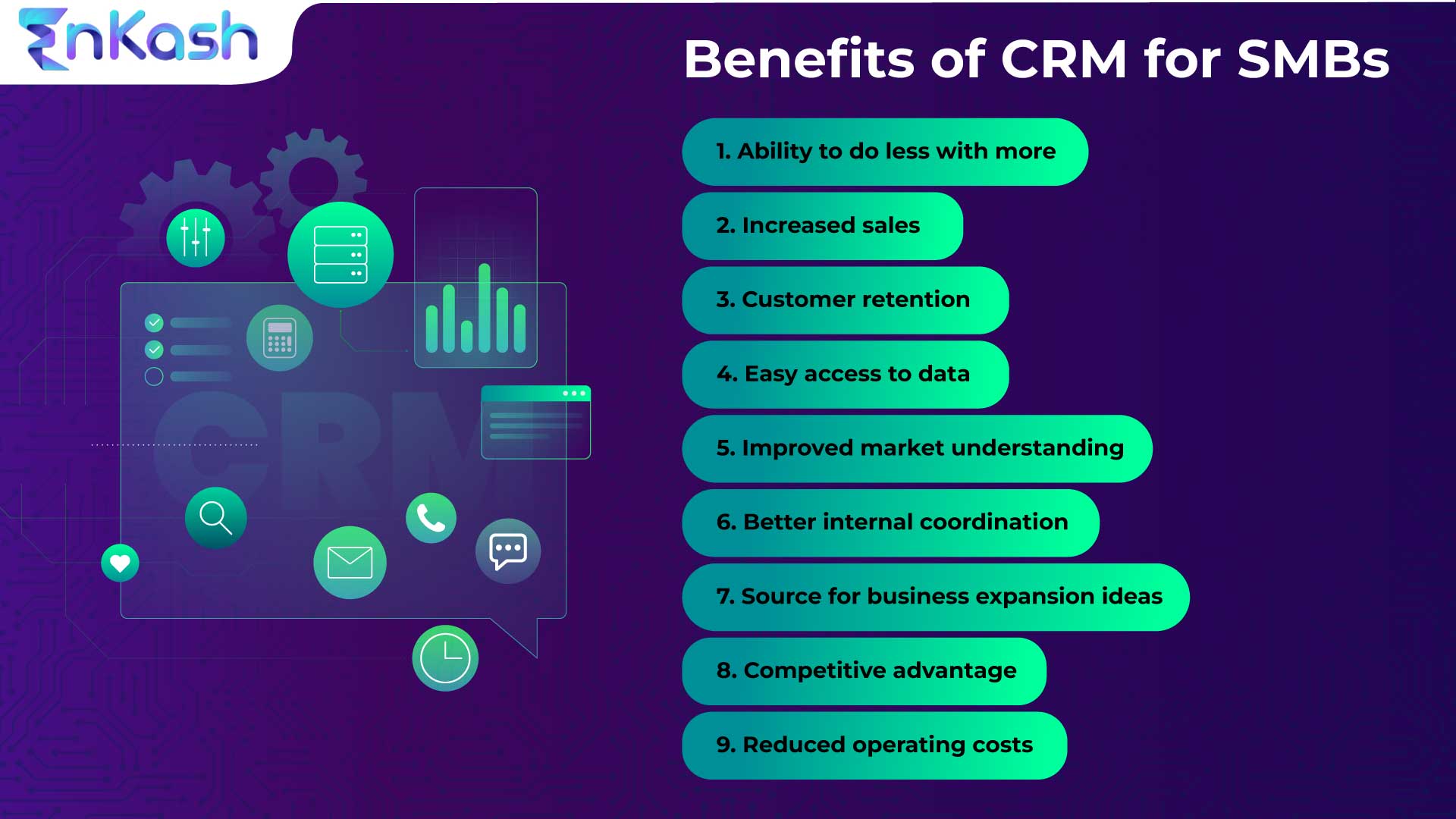

9 reasons that showcase the importance of CRM for SMBs and startups

Ability to do less with more

As a small business, doing more with least amount of resources is always the aim and your investment in the CRM can help you do that. For instance, the work of data mining to see what customers are saying about your business and service levels can be collected from the CRM. You can also use the CRM to ensure that there is common information available to all the departments without the need to generate reports, share, and disseminate the information.

Increased sales

The need to improve revenue generation is the aim of most businesses and more so for smaller businesses because their access to funds is lesser. With a CRM in place, increasing sales becomes easier. There are two ways that this happens, repeat sales to those customers who are ripe for it based on the information in your CRM or referrals from existing customers because they are happy with the seamless experience you have provided thanks to the information access provided by your CRM.

Customer retention

In a smaller business or startup, the loss of a single important account or customer can have a big impact and therefore customer retention is of vital importance. The importance of CRM is showcased here when all your customer-facing teams are able to provide a comfortable and pleasant experience to customers. Imagine the delight customers will express when your accounts receivables team thanks for them timely payments instead of calling them to make payments, which happens by default when there is no CRM.

Easy access to data

Whether your business is a large one or a small startup, data is the fuel that keeps your business running. Want to know how much sales have happened or want to know which product has the most complaints or want to understand the trend for sales volumes across various time periods, the CRM can mine the data and enable better decision-making.

9 Major benefits of CRM

Improved market understanding

In today’s market conditions, only those companies that listen to customers and understand market trends can thrive. And carrying out market surveys and purchasing expensive reports can be time-consuming. With the CRM, you can pick out information from various sources, including leads that did not get converted, to get an understanding of market trends and the pulse of customer needs.

Better internal coordination

As a startup, it is likely that you are operating with a smaller team for each department and this often burdens the people working on different teams. As a result, the customer experience could suffer because people did not have enough time to share the information. With CRM, all teams have access to real-time information making coordination easier.

Source for business expansion ideas

The importance of CRM software for SMBs and startups can be felt the most when you want to expand your business and want some ideas. Not only with the CRM point you in the right direction but also substantiate the idea with solid data collected over the course of time.

Competitive advantage

In a world where competition is rife, it is essential to stay ahead and the differentiator in most cases, is the way you make your customers feel. With the CRM software in place, you will be able to ensure that the customer needs are anticipated and met with, giving you the competitive advantage.

Reduced operating costs

As a growing business, cutting costs is one of the topmost concerns and CRM for small businesses can offer a ready solution. The CRM helps you do more with less, ensures that data mining is easy, cuts down the lead time to close a deal, and reduces paperwork, thus, helping reduce costs.

At EnKash, Asia’s 1st & smartest spend management platform, we believe in empowering our customers with the best fintech solutions to manage their needs. Check out solutions to find the one that fits you the best.

If you are a small business or startup that has come up with an innovative concept or idea, then read on to understand more. You will understand what patent filing is, and why you should consider patent filing and patent filing in India in simple steps.

What is a patent?

Let’s start by looking at what a patent means. By definition when you or your business has come up with a unique product or concept that has not been invented or discovered until now, then you can patent the idea or concept as belonging to you. Having a patent for a product or concept means that you have the exclusive right to the idea and that others who want to use the idea will have to pay you patent fees.

Why file for a patent?

Today, one of the most valuable assets is intellectual property. In a world where information on any aspect is available online, if you have a unique idea, it is better to patent that concept. There are several reasons for doing this.

Protecting your intellectual property

Since a lot of effort has gone into the concept, you need to protect the rights of your business. In case somebody wants to use the concept, then they will need to pay you to get the rights to do so.

Curbing misuse or distortion

The way today’s market conditions are, makes competitors take a concept and slightly change or distort it to present it as their own. Patenting prevents this from happening and protects you.

Improve the valuation of your business

If your business has a unique idea, then it makes sense to consolidate your position as the market leaders and improve the valuation of your business. Patenting your idea helps you do just that.

Catch investors’ attention

As a small business or a startup, it is essential to catch potential investors’ attention so that your business can attract capital or debt as required to grow and flourish in a competitive market.

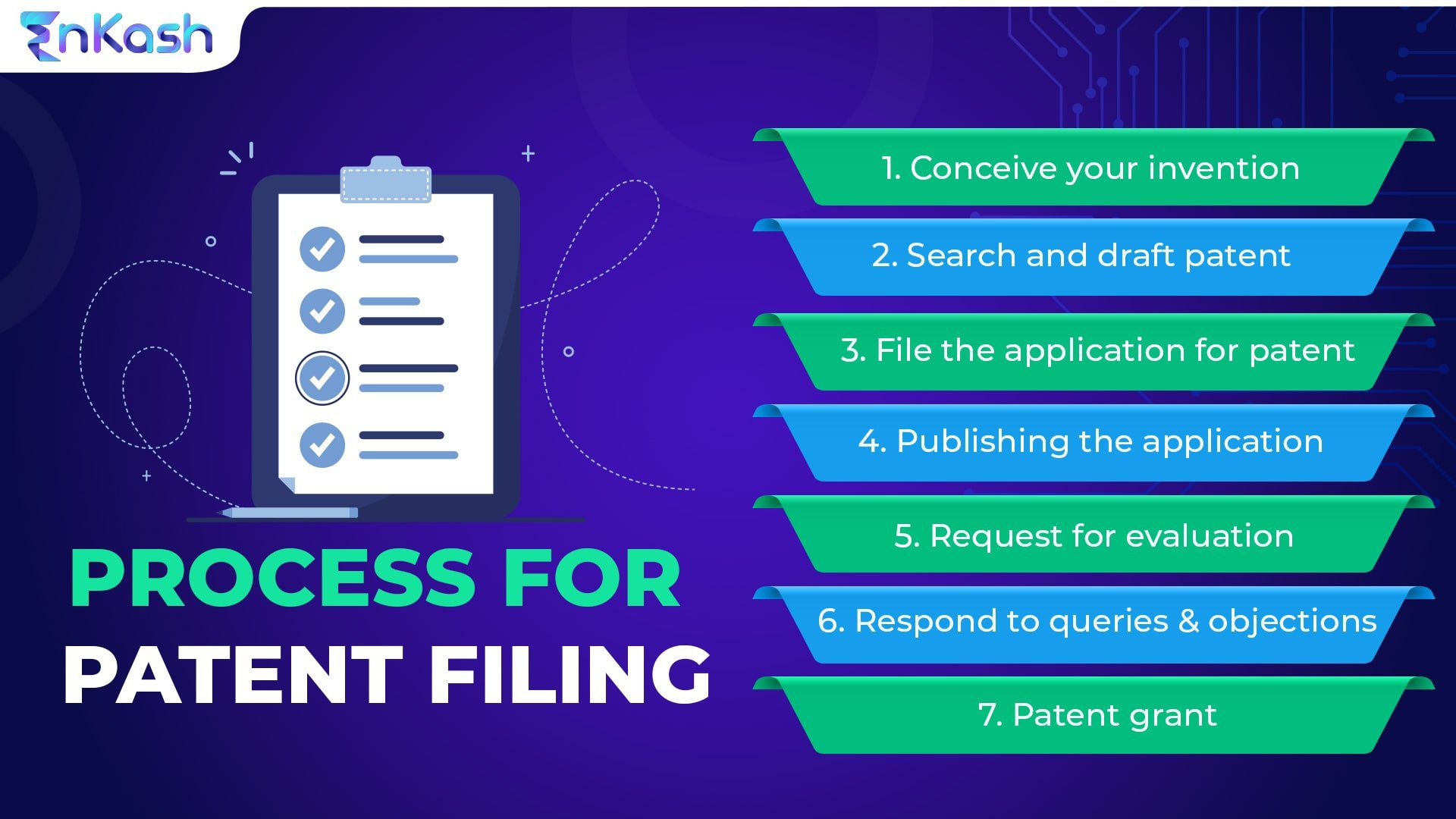

Now that we have understood what patent registration means and why you should register your patent let’s look at how to go about patent filing in India.

The first step is once your business has come up with your invention to get all information together. Factors like the type of invention, the advantages, how it help, and carrying out a search whether there is an existing patent needs to be done. Under the act, you need to ensure that the concept does not fall under the categories that are not patentable.

Search and draft patent

Once you are through the first part, you have to start searching in terms of patentability before drafting your concept. This search will identify the concepts that are closest to the one you are trying to patent.

File the application for patent

Process for patent filing

Once you have completed the draft, you can file it with the patent office, generally using form 1, and you will be given a receipt along with a patent application number. As a startup or a small business, you need to use Form 28 to file for patents.

Publishing the application

The application is filed after 18 months of filing the application. In case you do not want to wait for 18 months, you can request for early publication and pay the prescribed fee using Form 9. With this move, you can expect publication within one month of application.

Request for evaluation

Unlike the publication stage, the evaluation does not happen automatically and you have to file a request latest by 48 months from the date you file the application under Form 18. Once the controller gets the request, the application is passed on to the patent examiner who will look at it from different patentability criteria points of view. The application, usage, novelty, etc is looked at and the applicant is provided with the First Examination Report or FER. You can also request an expedition using Form 18A under Rule 24C.

Respond to queries and objections

Once you get the FER, you are supposed to respond to all the objections raised in the report in writing. As the applicant you can negate any objections and prove the applicability of the invention. This can be done by physical presence or through video conferencing.

Patent grant

Once all the objections are addressed, and if the patent application is found to meet all criteria, then it could be placed for a grant and the patent granted to the applicant. Anybody who wants to oppose the patent will have to do so within 12 months of the patent grant via a notice to the controller.

What is the cost of patent filing in India?

The cost of patent application is around INR 4000 for smaller businesses, INR 8000 for larger businesses, and additionally, there could be attorney fees ranging from INR 20000 to INR 35000.

Visit EnKash to learn how as Asia’s 1st & Smartest Spend Management Platform, we help businesses like yours grow to their full potential.

Human Resources (HR) is an important department for every profitable business. The human resource department forms the organization’s backbone by hiring suitable people. The success of any business enterprise is measured in terms of staff satisfaction and work performance.

The Human Resource (HR) Department undeniably plays a vital role in any organization, whether a startup or a multinational. In a startup, HRs are responsible for supporting the growth of the business by defining and attracting the ‘right’ talent, determining the organizational structure, creating clear communication channels, framing the code of conduct, and so much more.

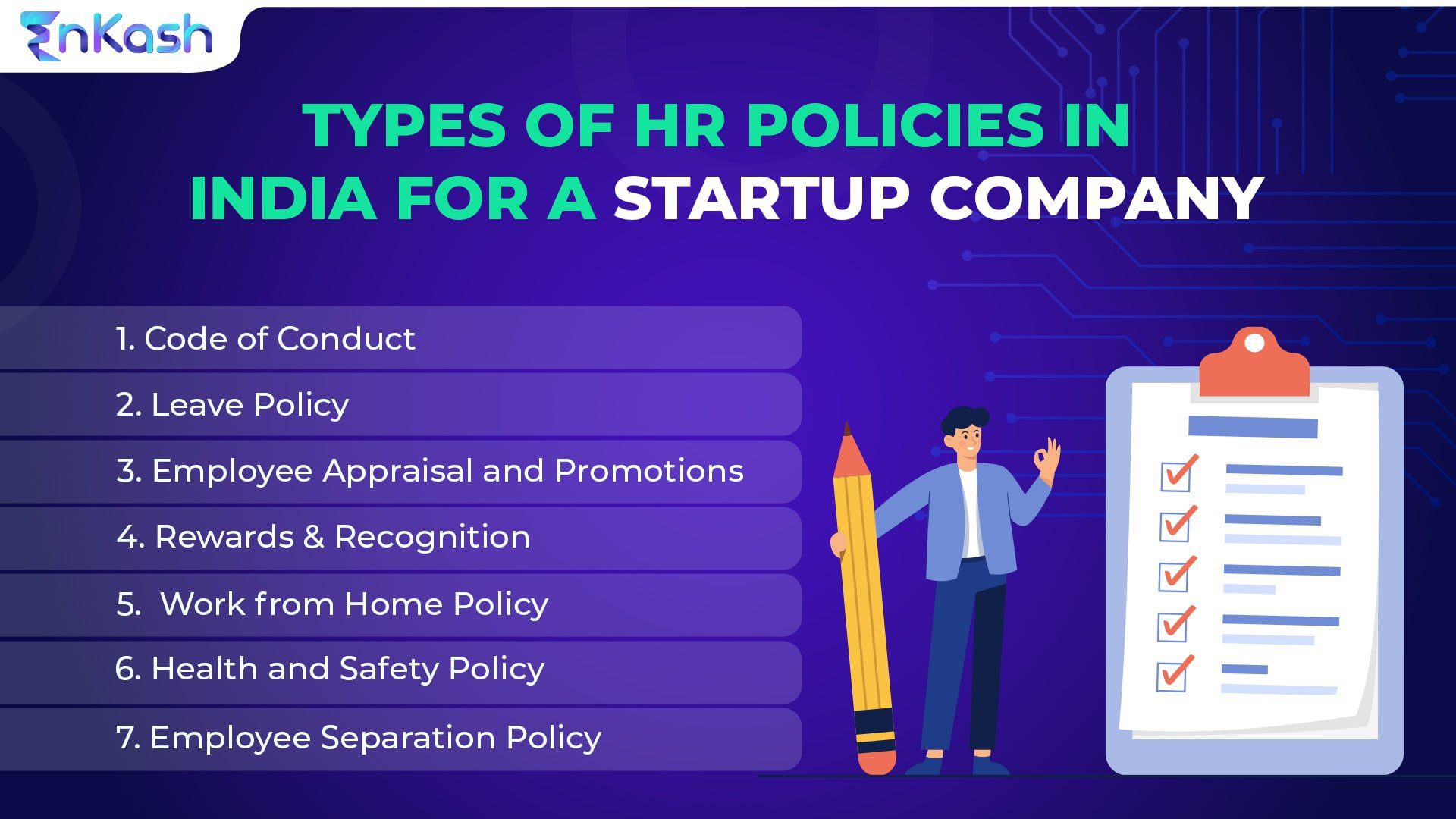

HR Policies for a Startup in India

Code of Conduct: The code of conduct HR policy consists of the aim, vision, and mission of any startup. It also helps to build and maintain the right workplace for the employees. Most importantly, it contains rules and regulations for the employees to abide by.

Leave Policy: This is one of the most important policies for any employee of the organization as it outlines the various types of leaves an employee can avail in different situations like maternity leave, female-day care leave, casual leave, sick leave, annual leave, and more. Many organizations have a non-paid leave policy as well depending on the situation where the salary of the employee will be deducted.

Employee Appraisal and Promotions: This is another policy company that stands as one of the important HR policies for a startup. In this, the founders, and the top-level management evaluate the employee’s performance over a period of six months or annually and provide them critical feedback on their performance, and then reward them accordingly with an increase in salary and promotions.

Rewards & Recognition: When the employees are appreciated, they tend to work better. As part of many HR policies, this policy states how the employees must be rewarded based on values, goals, and priorities. Many companies reward employees quarterly with monetary rewards or gift vouchers to boost employee morale.

Work from Home Policy: Ever since the novel coronavirus hit the globe, various organizations have shifted away from the traditional way of only working from the office to working from anywhere i.e. working from home. Some startups are working completely remotely whereas others are insisting their employees come to the office full-time, or a fixed number of days a week.

Health and Safety Policy: For any startup, the well-being of its employees is the foremost concern. It includes not only physical well-being but also mental and emotional well-being. Hence, the HR department frames various health and safety policies for the employees to ensure that every employee is provided with the best work environment at the workplace.

Employee Separation Policy: When the employee decides to leave the organization, once again the role of HR comes into place where various documentation work is exchanged amongst the employees and the employers. There are various exit formalities that are to be cleared by the employees before the company in order to avail the full & final payment, relieving letter, or experience letter.

Types of HR policies in India

Why does a startup need an HR policy?

There are various reasons why a startup needs an HR policy. Listed below are a few reasons:

In a startup, clear-cut HR policies help to treat employees fairly across the organization.

Such HR policies serve to preempt various misunderstandings between employees and the employer regarding employees’ rights and obligations in the workplace.

These policies help early-stage & growth-stage startups in saving valuable time and resources.

The absence of clear HR policies leads to a decline in employee morale, deterioration in employee loyalty, and increased vulnerability to even legal penalties.

Conclusion

This blog gives an overview of any organization’s most commonly used policies. These policies majorly depend on the company size, type, and industry, and these policies must come into action based on the same. When framing the HR policies and procedures, it is imperative for the Human Resource team of every organization to keep in mind all the business practices and all the applicable national, state, and local laws.

When running a business, be it small or large, its management is certainly not an easy feat. A growing business requires a lot of strategizing cash flow, investment in the right areas, planning for maximizing profits while minimizing business expenses, and much more.

However, while running a growing business, there are high chances that obstacles to business growth are a common challenge faced by various entrepreneurs/business owners. This happens due to various reasons, such as vastly overestimating the value of the business, lack of understanding of the market, etc.

In this post, various credit mistakes are highlighted that must be avoided by a growing business.

Use of both Personal and Business Credit for Growing Business

One of the most common mistakes made by a growing business is mixing personal and business finances, thinking it will help them build a good business credit score. In fact, paying anything relating to your business expenses with personal credit will only increase the chances of harming your personal credit score.

However, you must try to build the credit profile of your growing business by always making all the purchases either through a business credit card or a business account so that there is a complete track of all your business expenses. Moreover, you must know that the credit limit issued to businesses is very high in comparison to the limit issued to individuals owning personal cards.