If you are a small business or startup that has come up with an innovative concept or idea, then read on to understand more. You will understand what patent filing is, and why you should consider patent filing and patent filing in India in simple steps.

What is a patent?

Let’s start by looking at what a patent means. By definition when you or your business has come up with a unique product or concept that has not been invented or discovered until now, then you can patent the idea or concept as belonging to you. Having a patent for a product or concept means that you have the exclusive right to the idea and that others who want to use the idea will have to pay you patent fees.

Why file for a patent?

Today, one of the most valuable assets is intellectual property. In a world where information on any aspect is available online, if you have a unique idea, it is better to patent that concept. There are several reasons for doing this.

Protecting your intellectual property

Since a lot of effort has gone into the concept, you need to protect the rights of your business. In case somebody wants to use the concept, then they will need to pay you to get the rights to do so.

Curbing misuse or distortion

The way today’s market conditions are, makes competitors take a concept and slightly change or distort it to present it as their own. Patenting prevents this from happening and protects you.

Improve the valuation of your business

If your business has a unique idea, then it makes sense to consolidate your position as the market leaders and improve the valuation of your business. Patenting your idea helps you do just that.

Catch investors’ attention

As a small business or a startup, it is essential to catch potential investors’ attention so that your business can attract capital or debt as required to grow and flourish in a competitive market.

Now that we have understood what patent registration means and why you should register your patent let’s look at how to go about patent filing in India.

Also Read:

- Why Startups should invest in technology

- 5 Credit Mistakes to Avoid as a Growing Business

- Business vs Personal Credit Cards: What’s the Difference?

What is the process for patent filing in India?

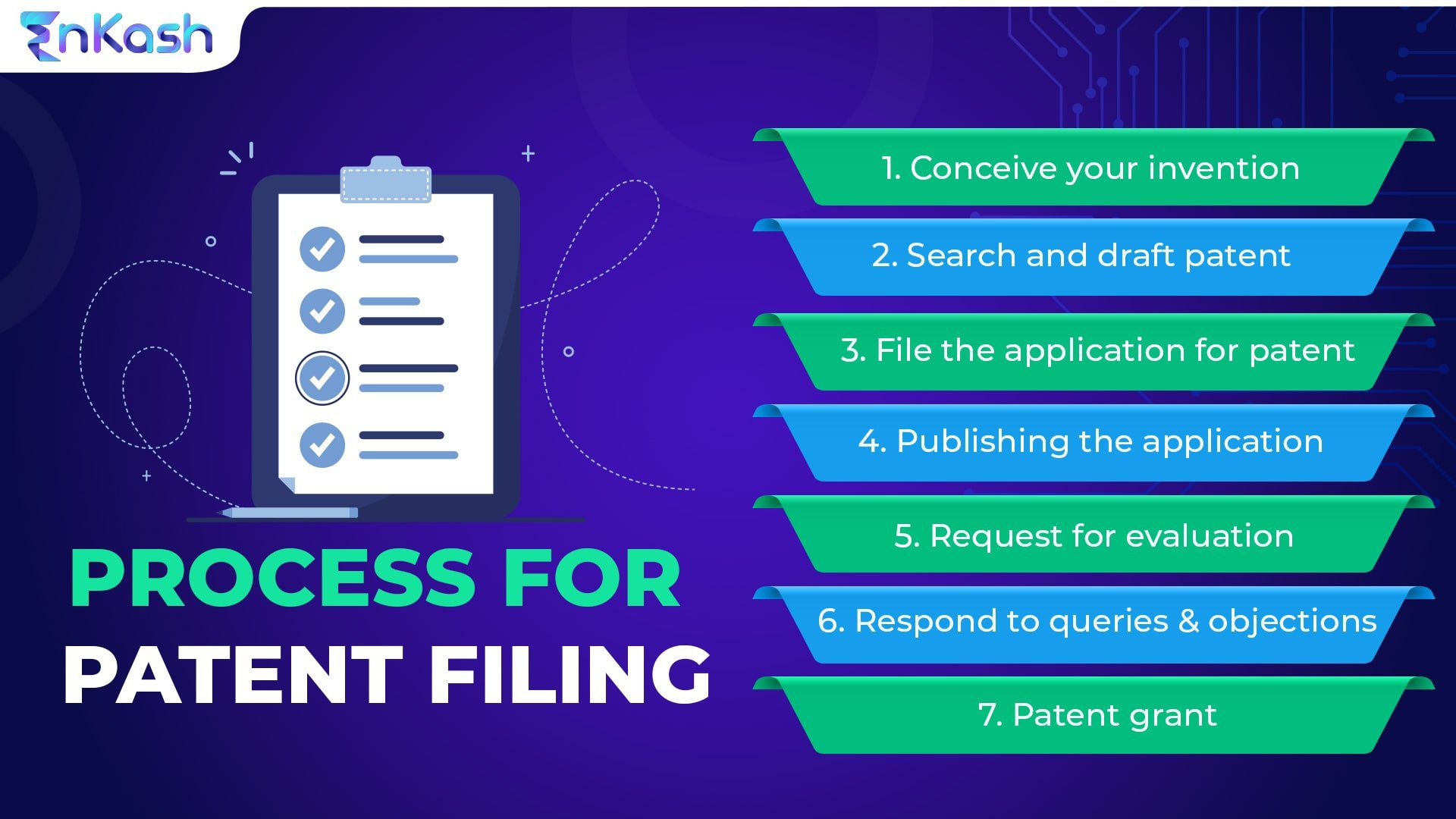

Conceive your invention

The first step is once your business has come up with your invention to get all information together. Factors like the type of invention, the advantages, how it help, and carrying out a search whether there is an existing patent needs to be done. Under the act, you need to ensure that the concept does not fall under the categories that are not patentable.

Search and draft patent

Once you are through the first part, you have to start searching in terms of patentability before drafting your concept. This search will identify the concepts that are closest to the one you are trying to patent.

File the application for patent

Once you have completed the draft, you can file it with the patent office, generally using form 1, and you will be given a receipt along with a patent application number. As a startup or a small business, you need to use Form 28 to file for patents.

Publishing the application

The application is filed after 18 months of filing the application. In case you do not want to wait for 18 months, you can request for early publication and pay the prescribed fee using Form 9. With this move, you can expect publication within one month of application.

Request for evaluation

Unlike the publication stage, the evaluation does not happen automatically and you have to file a request latest by 48 months from the date you file the application under Form 18. Once the controller gets the request, the application is passed on to the patent examiner who will look at it from different patentability criteria points of view. The application, usage, novelty, etc is looked at and the applicant is provided with the First Examination Report or FER. You can also request an expedition using Form 18A under Rule 24C.

Respond to queries and objections

Once you get the FER, you are supposed to respond to all the objections raised in the report in writing. As the applicant you can negate any objections and prove the applicability of the invention. This can be done by physical presence or through video conferencing.

Patent grant

Once all the objections are addressed, and if the patent application is found to meet all criteria, then it could be placed for a grant and the patent granted to the applicant. Anybody who wants to oppose the patent will have to do so within 12 months of the patent grant via a notice to the controller.

What is the cost of patent filing in India?

The cost of patent application is around INR 4000 for smaller businesses, INR 8000 for larger businesses, and additionally, there could be attorney fees ranging from INR 20000 to INR 35000.

Visit EnKash to learn how as Asia’s 1st & Smartest Spend Management Platform, we help businesses like yours grow to their full potential.