On 1st February 2023, Honorable Finance Minister Nirmala Sitharaman announced in the Union Budget 2023-2024 the extended tax holiday date for startups from 31st March 2023 to 31st March 2024 for availing tax benefits. Moreover, she also extended the benefit of carry-forward of losses on change of shareholding of startups from seven years to ten years of incorporation.

The tax holiday scheme was first introduced in the Union Budget 2017 for startups incorporated after 2017 who could avail of a tax holiday for three out of seven years from the day of their incorporation. However, for startups to be eligible for availing the tax incentives, their turnover should be less than Rs 100 crore in any of the previous financial years. Learn more about the announcement of Tax Holidays for Startups in this blog.

The Government of India runs an incentive program for startups, i.e., a tax holiday, which aims to stimulate foreign investment by reducing taxes on businesses. The objective is to foster the growth of the economic system of startups in India. However, it is revised by the government from time to time.

Did you know?

As per the survey, the number of recognized startups in the country has increased from 452 in 2016 to 84,012 in 2022.

Benefits of Tax Holiday for Startups

The following are the benefits of tax holidays for startups:

Helps startups meet their working capital needs in the first few years of driving

Helps domestic and foreign investors to take a larger bet on promising quality startups

The capital gains exemption motivates many businesses to launch new startups and provide new jobs for the youth

Startups get a breakthrough for growing their business in the long run, which ultimately generates higher taxable revenue in the future

Bottom Line

With this extension, it is a significant step taken by the government of India to support the startup ecosystem in India, which is adversely affected by the COVID-19 pandemic. Moreover, this will foster the growth of the startup industry and drive innovation in the country.

In the budget announcement, the expansion of DigiLocker will ease the KYC process, which can then be used to verify other services and cut FinTech costs, was also mentioned.

Keep watching this space to get further insights and updates on the Budget 2023.

If you are startup or smaller business in today’s economy, the budget 2023 would have been a much-awaited event. There have been many positive announcements in the budget that will help upcoming businesses. Further to our article on the highlights of Budget 2023 and how it will affect startups, small and medium businesses, we will explain a bit more DigiLockers.

The two updates with regard to DigiLockers were as follows:

Fintech Services: Fintech services in India have been facilitated by our digital public infrastructure including Aadhaar, PM Jan Dhan Yojana, Video KYC, India Stack and UPI. To enable more Fintech innovative services, the scope of documents available in DigiLocker for individuals will be expanded.

Entity DigiLocker: An Entity DigiLocker will be set up for use by MSMEs, large business and charitable trusts. This will be towards storing and sharing documents online securely, whenever needed, with various authorities, regulators, banks and other business entities.

Now that we know what the update was, let’s take a closer look at how it will affect your business.

What is DigiLocker?

DigiLocker is an initiative by the government to enable paperless governance. The aim of the DigiLocker is to empower you digitally by providing access to a digital document wallet. The idea is to facilitate individuals and business entities to store, share, and verify documents and certificates. Like a physical locker that is used for safekeeping of valuables, a digital locker or DigiLocker will store important documents like digital versions of PAN card, AADHAR card, and so on.

How does the budget announcement change the use of DigiLocker?

The government has proposed that it will expand the scope of the digital document repository by making it a part of the public digital infrastructure (PDI). As a result, fintech companies will be able to cut costs and also increase the ease of doing business by making the KYC (know your customer) process simpler and faster.

There is still a lack of clarity on the way forward about the functioning of the DigiLockers. As per the experts, they expect APIs (application programming interfaces) to be built on the lines of Aadhar. Since APIs allow the interaction between different applications, it can be a way to quickly verify the validity of the documents. However, further work has to be done to ensure the security of these documents, restricting unauthorized access, and ways to ensure that no misuse of these documents occur.

With this change, there is expected to be quicker access to finance as the KYC process will become simpler. There is also the possibility of reduction in cost of KYC resulting in improved efficiency and increased level of services to the underserved parts of the economy.

Now that we have an idea of how this update will affect fintechs and the way they approach KYC norms, let’s take a quick look at accessing DigiLocker.

Do you know how to register and activate a digilocker account?

Honorable finance minister Nirmala Sitharaman has just finished her budget announcement. She outlined seven priorities of the budget, which were inclusive development, reaching the last mile, infra & investment, unleashing potential, green growth, youth power, and the financial sector.

There is already a buzz among the business and salaried class about the changes and reforms she is proposing to bring about. It can often be confusing to know how the budget will impact you.

At EnKash, our mission is to enable small and medium businesses and startups to grow with the help of fintech solutions. We have put together a snapshot of the budget highlights that will have an impact on your business.

Capex Outlay hiked by 33% to 10 lakh crores: What this means is that the government will continue to invest in strengthening the infrastructure of our country. The positive impact on connectivity, communication, and logistics

Compliance complications reduced: More than 39000 compliance has been reduced to improve the ease of doing business. This means that your growth and development will become easier with the intention of the government to leapfrog growth.

AI for business and economic development: The creation of centers of excellence for AI development. This means that the government wants to use AI to unleash the potential of our economy.

KYC process simplified and PAN as digital identifier: KYC process to be simplified to become fully amenable to meet the needs of digital India. PAN is to be used as the common digital identifier for businesses to enable ease of operations.

DigiLockers to set up: One-stop solution for updating and reconciling identity to be established using DigiLocker and Aadhar as the basis. “An entity DigiLocker will be set up for MSMEs, large businesses, and charitable trusts. This will be towards storing and sharing documents online securely, whenever needed with various authorities, regulators, banks, and business entities,” Sitharaman said.

Contract relief for MSMEs: 95% forfeited amount to bid or security to be returned by the government to MSMEs. This means that if an MSME fails to carry out a contract during the COVID time, then relief will be provided by the government and government entities

Result-based financing introduced on a pilot basis: For better allocation of funds, now financing will be provided based on the results that businesses are showing rather than input-based.

Paperless onboarding facilitated: Entity DigiLockers would be set up as a critical move for businesses and would facilitate the paperless onboarding of businesses. The scope of documents available in the DigiLocker will be expanded to help with development—storing and sharing documents will be easier.

Credit guarantee to MSMEs: Financial inclusion at scale, credit guarantee for MSMEs – revamped with 9000 crores in the coffers from April 1 onwards. 2 lac crores will be available. What is more, the cost of the credit will be reduced by 1%.

National information registry for credit and financial inclusion: The setting up of this repository to collect, save, and share ancillary and financial data will encourage better flow of credit, ensure financial inclusion, and improve fiscal stability. This will be done in consultation with the RBI.

Digital transactions are up by 76 percent: Digital public infrastructure will get fiscal support and continue to do so.

Presumptive taxation for MSMEs and professionals: If you are an MSME with turnover of Rs.3 crores from Rs.2 crores or a professional with a turnover touching Rs.75 lakhs from Rs.50 lakhs, can get the presumptive taxation benefit as long as you have less than 5% cash receipts.

Keep watching this space to get further insights and updates on the Budget 2023.

FinTech is the combination of Finance & Technology which is constantly evolving and adapting to new technological trends and the needs of the customers by replacing the traditional banking system. In this blog, we have discussed a few potential trends in FinTech that may impact the banking and FinTech industry in 2023.

Digital-only Banking

With the evolving advances in technology and all that it can offer, changing rapidly, customer expectations are also changing with time. Moreover, the ever-increasing demands for instant and personalized experiences, especially after COVID-19, have permeated the banking ecosystem in the past few years. Hence, the same has pushed banks to operate digitally. To be specific, FinTech will continue to carve the path for digital-online banking in 2023, which will be more seamless, real-time, and transparent.

Contactless Payments

Since the novel coronavirus pandemic hit the world, contactless payments have become the new norm for making purchases such as UPI, payment links, wallets, etc. The payment industry in India has also undergone a drastic change, and it will continue for many years. Contactless payments are highly accessible and help lower entry barriers, especially for SMBs in India.

Blockchain Technology

Blockchain Technology revolutionized the FinTech industry by providing an extremely secure and transparent way of storing and transferring data in the past. It will likely continue to shape how businesses are conducted and information is exchanged. In 2023, it will allow the banks to conduct faster transactions at marginally lower costs, improve their security, and reduce excessive bureaucracy.

Artificial Intelligence

Similar to the past few years, the way Artificial Intelligence (also called AI) has been embedded in every aspect of our lives, covering almost every domain and offering a plethora of financial services as well. It is expected that in 2023, financial institutions and the entire FinTech industry will be relying heavily on it for business payments, customer support, analytics, seamless onboarding, detection of financial fraud, and much more.

Super Apps

Supers Apps meets users’ everyday needs by offering a wide range of services and functions in that single portal. It is a collection of various niche applications and an integrated ecosystem of third-party services supported by the payment system. Moreover, to work on multiple tasks, a mini digital operating system is created to offer the best customer experience.

However, in 2023, Super Apps will be trending a lot, especially with the help of various FinTech startups in the industry that are aiming to build a digital ecosystem.

Neo-Banks

Neo-Banks have been providing a complete banking experience through digital platforms such as mobile applications for a long time. Apart from offering primary banking services, neo-banks will continue to provide automated and near real-time accounting and reconciliation services for bookkeeping, balance sheets, and taxation services in 2023. Moreover, neo-banking will significantly simplify the financial world with a better customer-centric approach.

Spend Management

Most small to mid-level enterprises are still stuck with spreadsheets and manual tracking of business spending and expenses. Hence, as an immediate need for automation, the Spend Management trend will surely rule the fintech industry in India by effectively increasing process efficiency and organizational savings by more than 30-40%.

In the year 2023, Spend Management platforms will help SMBs gain greater visibility in the overall operational spending activities and will also be working on inefficiencies, computation, and reduction of financial risks. It will regularize cash flow, minimize financial risk, and ensure optimum utilization of the company funds.

Final Words

It is true to say that the COVID-19 pandemic was the impetus for the proactive development of technologies that had been in execution for many years. It is always challenging to know the exact state of the FinTech trends as it is a rapidly evolving field.

However, keeping in mind past experience, the above FinTech Trends can be the game changer for the entire FinTech industry as they focus on improving various security-related issues, operational risks, overhead costs, and much more.

At EnKash, Asia’s 1st and smartest spend management platform, we offer various FinTech solutions to simplify spending and amplify revenues.

The digital rupee was proposed to be launched in 2017 as a planned digital form of the Indian rupee or INR. The digital rupee will be launched and offered via a few select banks and you can use it for transactions from individual to individual or from individual to merchant. Users can carry out transactions with e₹-R via a digital wallet that will be provided by banks included in the launch. You can store digital rupee on mobile phones and devices.

Salient features of the digital rupee

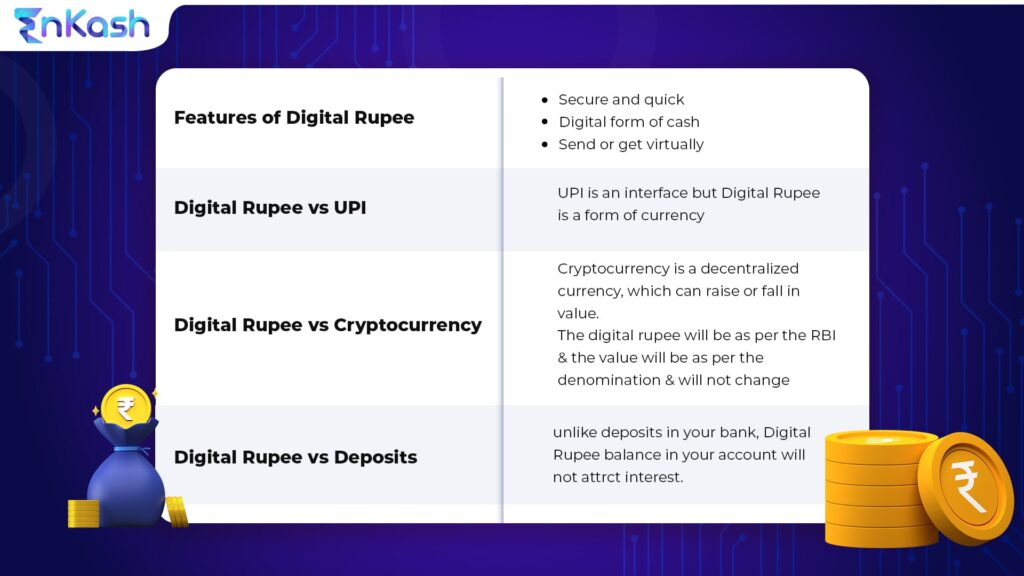

Secure and quick: Unlike the physical form of INR, blockchain technology enables the digital rupee can be transacted securely and in real time.

Digital form of cash: The Digital rupee is the digital or virtual form of rupees and you can avail of all the denominations like the physical currency.

Send or get virtually: You can send digital rupee tokens in digital form with ease instead of physical cash.

Given below are some frequently asked questions about the digital rupee and answers to these queries

Where is the Digital Rupee going to be launched?

RBI currently plans to launch the digital rupee in a controlled manner in a few cities. The cities include Bhubaneshwar, New Delhi, Mumbai, and Bengaluru.

Which banks are RBI planning to partner with to launch Digital Rupee?

RBI has partnered with IDFC First Bank, ICICI Bank, State Bank of India, and Yes Bank for the initial phase of the launch of the digital rupee.

How is Digital Rupee different from UPI?

The question that comes to mind is how is digital rupee different from the UPI. UPI or unified payments interface is a platform or interface that enables online transactions to happen but the digital rupee is a digital currency that will be regulated by RBI (Reserve Bank of India).

How is Digital Rupee different from Cryptocurrency?

The other doubt that most people have is around cryptocurrency and how the digital rupee is different from it. A cryptocurrency is a decentralized form of money that is not bound by the government or RBI. Cryptocurrency depends on blockchain technology for security and cannot be duplicated or counterfeited. Unlike Cryptocurrency, the value of the digital rupee will not fluctuate to go higher or lower. The denomination of the money will be indicative of the value of the digital rupee.

Will the Digital Rupee in your accounts attract interest?

The digital rupee will be the virtual form of INR and different denominations will have a unique identity. Like physical currency is held in wallets, the digital rupee can be held in virtual wallets. Unlike the cash balance in your account, which attracts interest, digital rupee will not attract interest.

Does using the Digital Rupee raise any privacy concerns?

Since the constant change in the market, the growth of the digital economy has been exponential in the past few years. The enforcement directorate of CBDC (Central Bank Digital Currency) has clarified that like the usage of the physical form of the rupee, the authorities will endeavor to ensure digital rupee usage will also remain private and the information will remain between the transacting parties. And the authorities are working actively to address the privacy concerns that have been raised.

How digital rupee is different from others

Watch this space for more updates on Digital Payments at EnKash, Asia’s 1st & Smartest Spend Management Platform, we always strive to serve our customers by dealing with all matters related to finance. From collateral-free credit limits to managing accounts receivables and accounts payable, EnKash has solutions for your fintech needs.

India is undoubtedly emerged as one of the fastest-growing countries in the FinTech Revolution in recent years, thanks to its economic growth. The country has previously introduced paperless loans, mobile banking, secure payment gateways, mobile wallets, and other concepts. In recent years, digital payments have made basic financial services more convenient to use and have witnessed widespread adoption. A variety of reasons have supported the growth and extension of India’s FinTech ecosystem, including the increasing availability of smartphones, improved internet access, and high-speed connectivity.

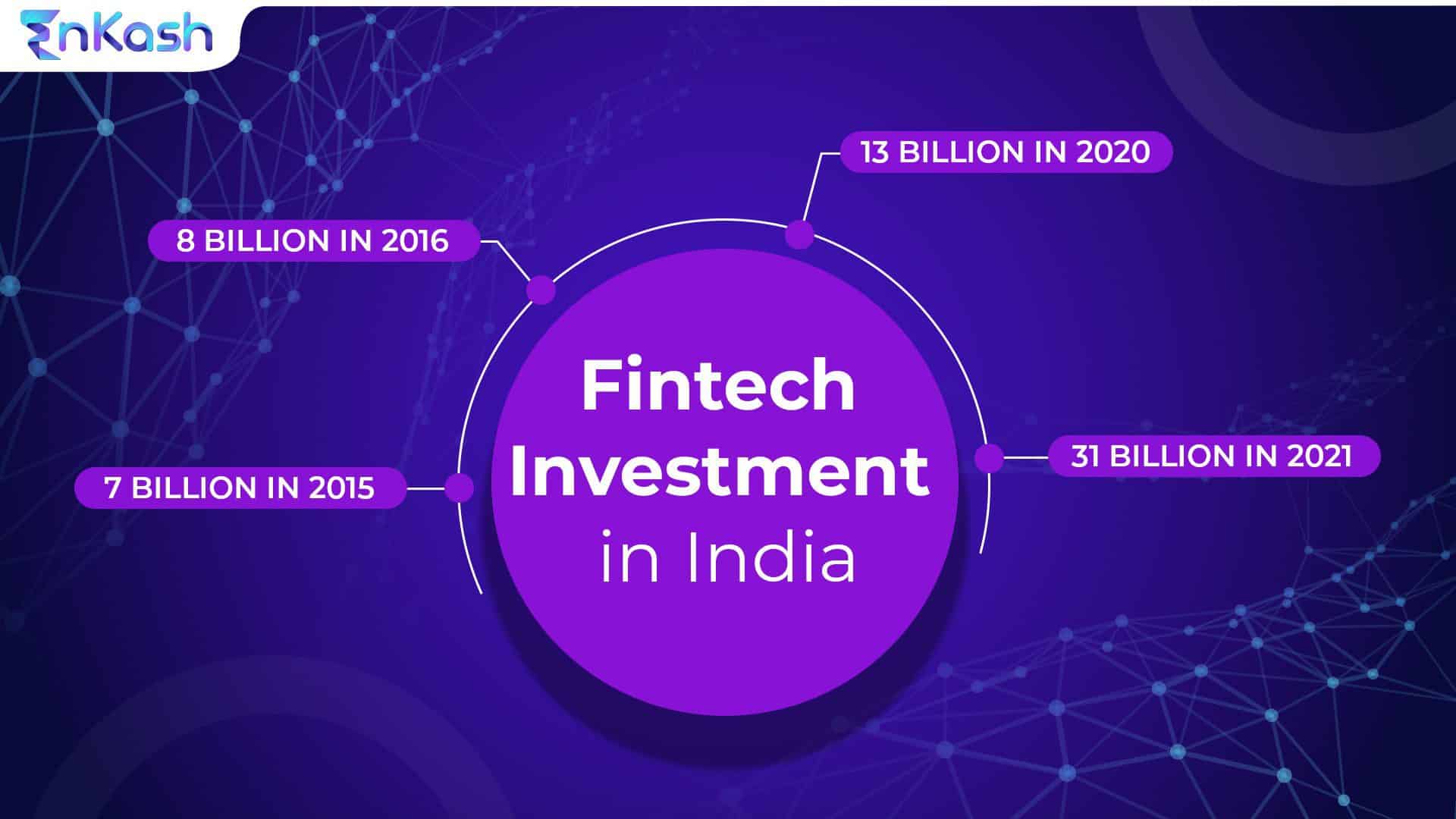

According to a study issued by Boston Consulting Group and FICCI, India’s fintech sector is well positioned to achieve a valuation of USD 150-160 billion by 2025 and it is estimated that about $20-25 billion in investments are likely to fuel this growth momentum over the next few years

India’s Digital Payments Industry: A Detailed Look

In India, banks have traditionally functioned as the only gateway to payment services. Nevertheless, with the rapid growth of technology, this looks no longer to be the case, as banks’ monopolies in this sector are gradually dissolving.

Digital India Payment infrastructure has improved significantly in recent years, owing to the introduction of new payment methods and interfaces, including the Immediate Payments Service (IMPS), Unified Payments Interface (UPI), Bharat Interface for Money (BHIM), and others. The government’s “Make in India” and “Digital India” initiatives also played a key supportive role in speeding up the fintech revolution. The country’s banking regulator, the Reserve Bank of India (RBI) has further enabled a policy environment that has led to increased use of electronic payments to establish a truly paperless society, which is commendable.

Government initiatives such as demonetization and the GST have generated a significant growth opportunity for fintech ventures across the country. Although demonetization caused widespread confusion and panic, particularly among the general public, it was ultimately the catalyst for a shift away from a paper-based, cash-based economy toward digital, electronic, technology-driven platforms, accelerating the country’s already-existing FinTech revolution.

The COVID-19 pandemic has further accelerated this digitization across a variety of categories, with contactless and cashless payments being marketed to foster social alienation.

In India, digital payments have become a way of life, with 10-15 million new users joining the digital bandwagon in the last year. Demonetization and the COVID-19 epidemic were two reasons that contributed to this shift. There is a massively complex ecosystem at the backend, but the reimagining at the backend has resulted in a fantastic experience for customers, resulting in massive adoption of digital payments. According to a survey, 67 percent of India’s more than 2100 FinTechs were formed in the last five years.

Digital payment systems have indisputably been the flag bearers of the Indian FinTech industry, thanks to the introduction of game-changing platforms such as Paytm, PhonePe, MobiKwik, and so on. Furthermore, the global relationship between Facebook and Reliance Jio is projected to transform India’s digital payments sector, with a specific focus on location-based e-payments that will cover tier 2 and 3 cities as well as rural areas.

FinTech Revolution in India: What the Future Holds

Despite India’s great diversity and population, a large chunk of the country remains unbanked, underdeveloped, and susceptible to a continuously shifting regulatory environment. Fintech, with its potential and capability to fundamentally modify and restructure India’s financial and banking services sector, comes into play here.

The country offers a great space for a FinTech revolution due to various factors such as an innovation-driven tech sector, a highly favorable market, increased smartphone and internet penetration levels, a young population, and government-led efforts to promote the industry. Furthermore, rising financial technology awareness has given the Indian Fintech industry a much-needed boost.

Fintech’s expansion in India is likely to further be aided by increased collaborations with traditional banking, insurance, and retail sectors, where they are aggressively adapting to changing client needs.

How Is FinTech Changing India?

Fintech is quickly changing the way banking and financial services operate in the country. These firms are at the forefront of this change, responding to changing customer demands and landscape. They are all expected to pick up speed and expand dramatically during the coming decade.

Fintech investment in India

Fintech companies have altered the face of the banking business in particular. Banks, too, are responding to new changes by digitizing transactions and spearheading the paperless and cashless process.

Simply put, Fintech companies seek to automate the supply and utilization of financial activities. Fintech, as the name implies, is a merger of the areas of finance and technology. The word was very recently invented, and it was mostly employed in the back-end systems of well-established and successful financial institutions. Fintech’s reach has recently broadened to include many areas of various businesses. Education, retail banking, and non-profit fundraising are a few examples.

Fintech makes use of specialized software and algorithms that have been devised and developed to give convenient financial solutions. Fintech not only benefits individual customers but also develops creative solutions for huge corporations and company owners. Fintech has also played an important influence in the creation and adoption of cryptocurrencies such as Bitcoin.

The Bottom Line

India is a vastly diverse and densely populated country, where a large proportion of the population is still unbanked. Fintech is an ideal financial option for this large group of people. When it enters the picture, it has the potential to alter India’s financial and banking sectors.

India is also a haven for innovative start-ups, with its favorable environment of smartphones and high-speed internet access. The government is also taking aggressive steps to accelerate the growth of the Fintech Companies making India a fantastic destination that is ripe for a Fintech revolution.

To know more, visit, EnKash. You can also click below on Signup Now, and we will reach out to you soon.