Does your business have access to a steady cash flow for day-to-day expenses? If not, have you thought of what the solution can be? While every business requires a steady flow of capital to operate efficiently, ensuring the same is hectic. So, while you plan to get your business a helping hand with daily expenses, you can get assistance from leading fintech management platforms such as EnKash.

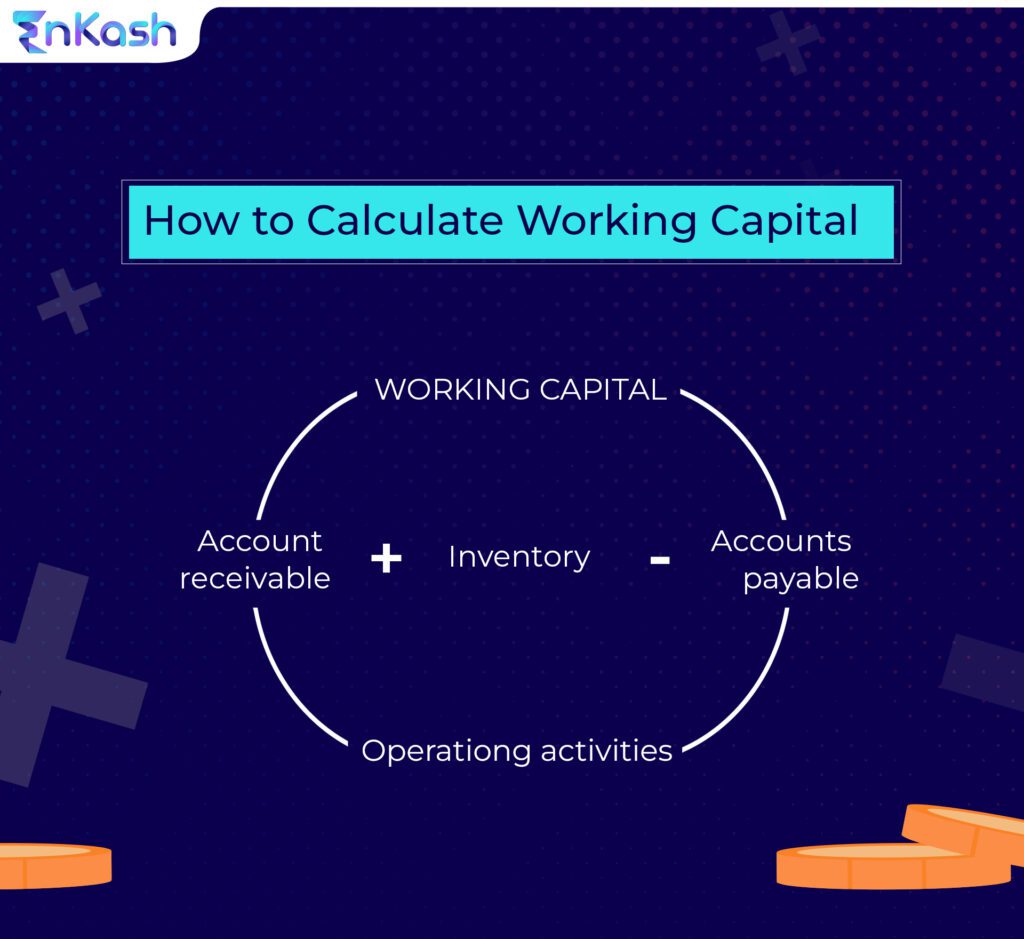

Whether running a small startup or a large corporation, having enough cash is essential to keep your business running smoothly. Working capital is the money available to a company to meet its day-to-day expenses. It’s the difference between your current assets and liabilities. Now, you must be wondering what do working capital loans mean. They are a type of financing that provides businesses with the necessary funds to cover their day-to-day expense.

This blog will discuss the features and benefits of working capital loans.

Features of working capital loans

Working capital loans are short-term loans (in most cases, revolving credit) intended to cover a business’s expenses for a short period, usually up to 12 months. Read further to learn about the features of working capital loans.

These loans come with a fixed repayment period and a fixed interest rate. Here are some key features of working capital loans:

- Quick access to funds: Unlike traditional loans that take a long time to process, working capital loans are usually approved within a few days. This makes it easy for businesses to get the funds they need quickly

- Flexible repayment options: Working capital loans come with flexible repayment options. Businesses can choose to pay back the loan in monthly or quarterly installments, depending on their cash flow

- Unsecured loans: Most working capital loans are unsecured, which means businesses don’t have to provide collateral to secure the loan. This is beneficial for small businesses that may not have enough assets to offer as collateral

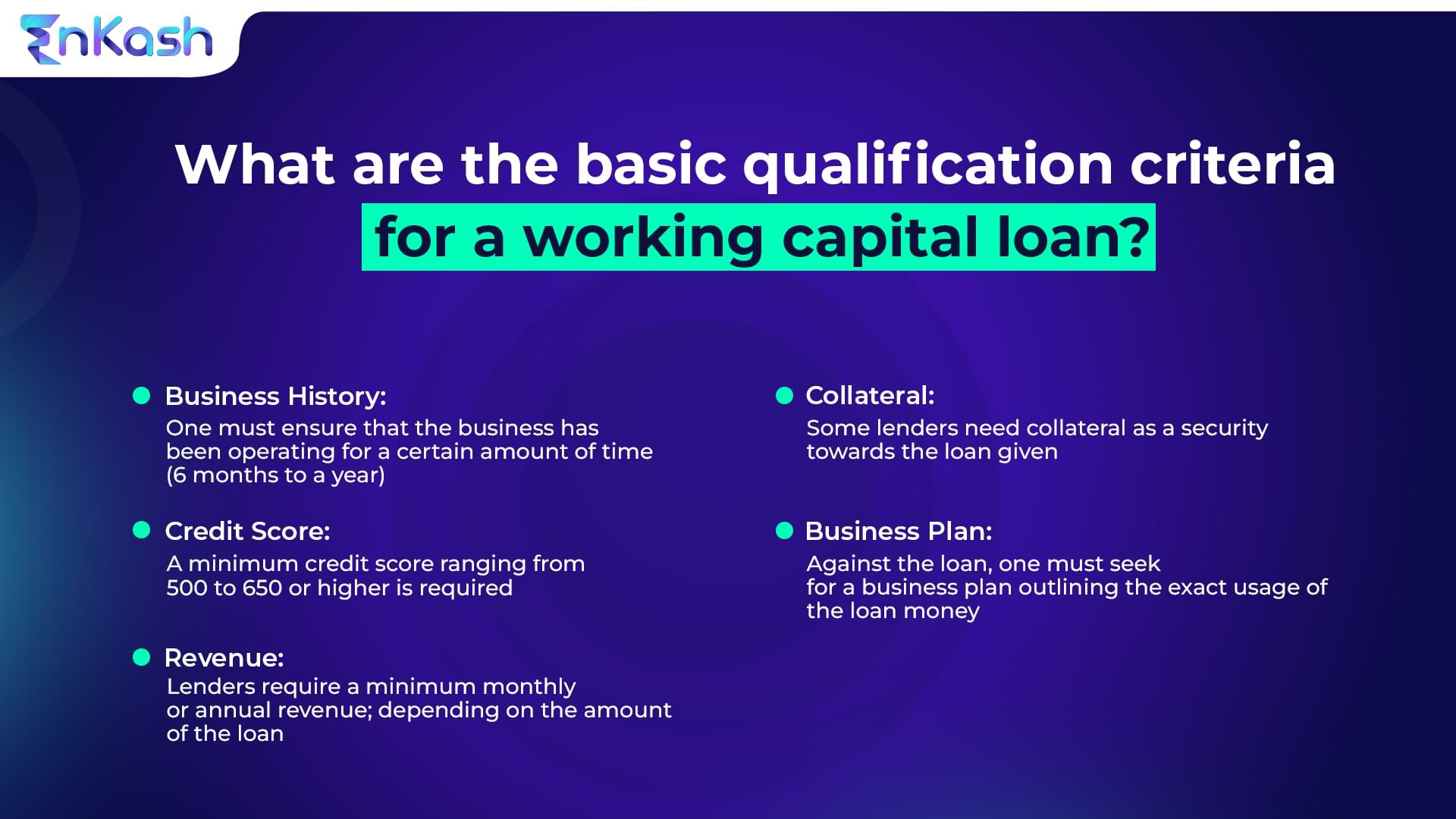

- Low credit score requirements: These loans typically have lower credit score requirements than traditional loans. This makes it easier for businesses with lower credit scores to get approved for a loan

Types of working capital loans

There are two main types of working capital loans: secured and unsecured. Let’s take a closer look at each of these types.

- Secured working capital loans: Secured working capital loans require collateral to secure the loan. Collateral can be in the form of assets such as property, equipment, or inventory. Secured loans usually come with lower interest rates than unsecured loans since the lender has some security in case the borrower defaults on the loan

- Unsecured working capital loans: Unsecured working capital loans do not require collateral to secure the loan. These loans are riskier for lenders since they have no security if the borrower defaults. Therefore, unsecured loans usually come with higher interest rates than secured loans

What are the benefits of working capital loans?

Working loans offer several benefits to businesses. Here are some of the top benefits of working capital loans:

- Maintains cash flow: Working capital loans help businesses maintain a steady cash flow, which is essential to meet their day-to-day expenses. This ensures that businesses have enough funds to cover their bills, payroll, and other expenses

- Helps businesses seize opportunities: Businesses need to act quickly when opportunities arise. Working capital loans can provide businesses with the necessary funds to take advantage of these opportunities, such as investing in new equipment or expanding their operations

- Businesses manage seasonal fluctuations: Many businesses experience seasonal fluctuations in sales. Working capital loans can help businesses manage these fluctuations by providing them with the necessary funds to cover their expenses during slow periods

- Helps businesses improve credit scores: By taking out and repaying working capital loans on time, businesses can improve their credit scores. This can make it easier for them to secure future financing at better rates

Conclusion

So, working capital loans are an essential financing tool for businesses of all sizes. If you wish to ensure that you get the working loan in time, make sure to keep your CIBIL score impressive. Use a corporate credit card to ensure a good CIBIL score.

Also Read: 5 Tips to Increase CIBIL Score

When considering financing options for your business, working capital loans should be at the top of your list. Whether you need funds to cover unexpected expenses, invest in new equipment, or expand your operations, working capital loans can provide you with the necessary capital to achieve your goals. By taking advantage of working capital loans, businesses can maintain cash flow, seize opportunities, manage seasonal fluctuations, and improve their credit scores.

If you’re looking to finance your business, consider a working loan. You agree that working capital loans are valuable for businesses needing quick access to funds. They offer flexible repayment options, lower credit score requirements, and the ability to maintain a steady cash flow.

For more such fintech-related queries and advice, visit our website today! Get the best assistance with EnKash now!