Today’s businesses are constantly looking for more modern and efficient ways to manage money. Every company now needs smarter tools to control costs and meet growing regulatory demands. One such tool is the prepaid card.

These cards are quietly changing how businesses manage expenses. Prepaid cards give more control, security, and flexibility than traditional credit or debit cards. This may sound surprising, but it’s true. These cards aren’t linked to bank accounts. They also don’t involve borrowing or credit.

In India, prepaid cards have grown quickly over the last decade. But what is prepaid card exactly? How does it work? And why are more businesses choosing it?

Keep reading to find out the answers and learn more about prepaid cards.

Prepaid Card: What You Need to Know

A prepaid card is a type of payment card that you load with funds before you use it. It’s essentially a plastic or digital card that functions like a mini wallet.

It may sound similar to a credit card. However, unlike credit cards, it isn't linked to a bank account or a line of credit. You top it up using cash, bank transfers, or other means. Then, you can spend only the amount that's already loaded on it.

The card carries a preset balance. Each time you make a purchase, that amount is deducted from the stored value. Once the funds run out, the card simply stops working. To use the card again, you will have to reload it.

Common prepaid card examples based on types include gift cards, phone recharge cards, and payroll cards. Gift cards, for instance, work only up to their loaded value, like a ₹2,000 store card. Modern prepaid cards, often issued under Visa, Mastercard, or RuPay, may be reloadable. That means you can keep topping them up for repeated use.

Prepaid Card Example

In India, prepaid cards fall under the Prepaid Payment Instrument framework, also known as the PPI framework. Many banks and fintech companies offer prepaid cards for different uses today in the country. For instance, there is an HDFC ForexPlus Card for international travel, an EnKash Meal Card for employee benefits, an SBI Gift Card for corporate gifting, and others.

Fintech platforms, such as Niyo, Enkash, Volopay, etc., offer reloadable prepaid cards. These cards are specifically designed for business expenses.. These cards often include real-time tracking and spending limits.

Paytm, PhonePe, and more such fintech platforms also offer prepaid cards. These cards are linked to digital wallets. They can be used both online and in physical stores. Most of these cards work on Visa, MasterCard, or RuPay networks, making them easy to use for both people and businesses.

How Prepaid Cards Work

A prepaid card is a payment card preloaded with money that you can use for purchases, bill payments, or ATM withdrawals — without linking it to a bank account or credit line.

It works like a digital wallet in card form: you load a fixed amount, spend it until the balance is exhausted, and reload it when needed.

A prepaid card means you spend only the money you load in advance.

Unlike debit cards (linked to your savings account) or credit cards (borrowed funds), a prepaid card operates on a prepaid balance only. This makes it ideal for controlled spending, online transactions, employee payouts, or gifting purposes.

Since the value is preloaded, prepaid cards offer spending security—but they are not the same as secured credit cards. Unlike credit cards, there’s no interest or unpaid balance. You can only spend what’s been loaded. In everyday use, prepaid cards often act like debit cards at checkout. They run on the same payment networks. But behind the scenes, they manage a stored balance and not a link to a bank account.

Read More: Corporate Credit Cards: Eligibility, Benefits & Application Process.

Types of Prepaid Cards

Prepaid cards come in different types:

Open-loop vs. Closed-loop:

- An open-loop prepaid card is branded by networks like Visa or MasterCard. It can be used anywhere those networks are accepted, even internationally.

- A closed-loop card works only at a specific store or chain. For example, a gift card that can be used only at one retailer.

Reloadable vs. Disposable:

- A reloadable prepaid card allows you to add money multiple times. It’s ideal for regular or ongoing use.

- A disposable card is for one-time use. Once the balance is finished, you throw it away. Gift cards are a common example.

International (Travel) Cards:

Many Indian banks offer prepaid travel cards with multiple currencies. You can load foreign currency before your trip and use the card abroad.

This helps you pay at locked-in exchange rates.

For example, a corporate employee traveling to the U.S. can use a USD prepaid card to avoid currency changes.

These cards work at most foreign ATMs and card machines.

Physical vs. Virtual:

- Physical prepaid cards are plastic. You can swipe or tap them to pay.

- Virtual prepaid cards are digital. They exist only as card numbers in an app or email. They are great for online shopping and offer better security.

Payroll & Incentive Cards:

Some companies pay salaries or bonuses using prepaid payroll cards. Others use prepaid gift cards for employee rewards or loyalty programs.

Key Differences

Types of Prepaid Cards in India (2025)| Type of Prepaid Card | Description / Features | Ideal Use Case |

|---|

| Reloadable Prepaid Cards | Can be loaded multiple times with funds. Can be linked to apps for online payments, corporate expense management, or payroll. | Businesses manage employee expenses, travelers, and regular online shoppers. |

| Gift / Disposable Cards | Preloaded with a fixed amount. Not reloadable. Usually used for gifting or one-time purchases. | Birthday or festive gifts, one-time online shopping, and rewards programs. |

| Virtual Prepaid Cards | Exists digitally without a physical form. It can be used for online transactions. Often safer due to limited validity and spending limits. | Online shopping, subscription payments, digital wallets. |

| Payroll / Corporate Cards | Issued for employees or vendors. Can be customized with spend limits and tracking. | Salary disbursement, vendor payments, and expense tracking for businesses. |

| Travel / Forex Prepaid Cards | Preloaded with foreign currency. Can be used internationally without currency conversion fees. | International travelers, students studying abroad. |

| Loyalty / Rewards Prepaid Cards | Issued as part of loyalty or reward programs. Can accumulate points or cashback. | Reward redemption, promotional offers, and corporate incentive programs. |

| Closed-Loop Prepaid Cards | Can be used only at a specific merchant, store, or group of stores. | Retail store gift cards, app-based reward cards. |

| Open-Loop Prepaid Cards | It can be used anywhere that accepts the card network (Visa, Mastercard, RuPay). Reloadable and widely accepted. | Travel, daily spending, online shopping, and global use. |

Prepaid Payment Instruments (PPIs) in India

In India, the RBI regulates prepaid cards under a system called Prepaid Payment Instruments (PPI). A PPI can be a card or a mobile wallet. It stores money that you can use for purchases or transfers.

Key RBI Points on PPIs:

- Value Stored: A PPI holds a fixed amount of money. You can use this stored value to buy goods, pay for services, or transfer funds. Prepaid cards fall under this category.

- Issuers: Banks and approved non-bank companies can issue PPIs. For widespread acceptance, businesses must get RBI approval.

- Types: The RBI divides PPIs into two types: Small PPIs and full-KYC PPIs. Small PPIs have lower limits and fewer features. Full-KYC PPIs allow higher balances and offer full banking features. Most corporate prepaid cards fall into the Full-KYC category. These can also be used to withdraw cash and are widely accepted.

- Reloading: PPIs in India can be reloaded in different ways. You can add money using cash, bank transfers, or other cards. However, reloading must adhere to RBI-imposed limits. For example, companies can reload corporate prepaid cards when departments need more funds.

Read More:

Supercharge Your Business with a Purchase CardHow Prepaid Cards are Different from Debit and Credit Cards

Understanding the difference between a debit card, a credit card, and a prepaid card is essential for managing your money wisely. Though these cards may look similar, they work differently based on funding source, spending limit, and repayment structure. Here’s a detailed comparison:

Comparison: Debit Card vs Credit Card vs Prepaid Card| Feature | Debit Card | Credit Card | Prepaid Card |

|---|

| Source of Funds | Directly linked to your bank account — funds are deducted immediately after each transaction. | Issued by banks or NBFCs that offer a credit limit. You borrow funds and repay later. | Works on a preloaded balance. You must load money before using it. |

|---|

| Spending Limit | Limited to the available balance in your account. | Determined by the issuer based on your credit profile. | Limited to the amount you’ve loaded onto the card. |

|---|

| Interest / Fees | No interest charges; nominal annual or transaction fees may apply. | Interest is charged on unpaid dues after the billing cycle. | No interest; may include minimal reload or issuance fees. |

|---|

| Usage Type | Suitable for cash withdrawals, online, and POS transactions. | Ideal for purchases, EMI conversions, and online payments. | Best for controlled spending, online transactions, and gifting. |

|---|

| Example | SBI Debit Card, HDFC Bank RuPay Debit Card | ICICI Coral Credit Card, HDFC Millennia Credit Card | EnKash Prepaid Card, SBI Gift Card, ICICI Bank Prepaid Card |

|---|

| Best For | Individuals who prefer spending within their means. | Users who want to build credit scores and earn rewards. | Those who need budget control, travel, or business expense management. |

|---|

Best Prepaid Cards in India

Top Prepaid Cards in India (2025)| Card Name | Issuer | Key Features | Ideal For |

|---|

| EnKash Prepaid Cards | EnKash | RBI-approved, customizable limits, real-time tracking, virtual & physical options, automated bookkeeping | Businesses managing expenses, payroll, and vendor payments |

| Volopay Prepaid Cards | Volopay | Multi-currency support, real-time tracking, ISO-certified security, customizable spend limits | Businesses seeking global expense management |

| HDFC Bank Prepaid Cards | HDFC Bank | Customizable spending limits, online account management, and cashback offers | Individuals and businesses seeking versatile payment solutions |

| SBI Business Debit Cards | State Bank of India | Expense control, easy tracking, and cashless payment options | Small and large businesses are integrating banking and expense management |

| Axis Bank Prepaid Cards | Axis Bank | Online shopping, utility bill payments, global acceptance, and chip and PIN technology | Individuals making online purchases, traveling abroad |

| Yes Bank Prepaid Cards | Yes Bank | Easy loading, online account access, and competitive exchange rates for international transactions | Individuals traveling abroad, students studying overseas |

| Bank of Baroda Prepaid Cards | Bank of Baroda | Secure and convenient payment options, contactless payments, balance inquiry, mini statements, and ATM withdrawals | Individuals seeking easy-to-use payment options for everyday transactions |

Prepaid Card Benefits for Modern Businesses

Prepaid cards are becoming more popular among businesses in today’s cashless world. They simplify expense management. They also give businesses more control, which makes them perfect for modern corporate needs.

Better Budget Control

Businesses can give prepaid cards to each team or employee. Each card can have a fixed budget.

For example, a manager may load ₹20,000 on a prepaid travel card. The employee can spend only up to that limit. This helps enforce department budgets. It also stops overspending. Managers can easily reduce or increase card limits when needed.

Reduced Debt and Fees

Prepaid cards don’t carry any debt or interest, unlike credit cards. A company spends only what it loads on the card. If the card has no balance, there's no financial loss. This is great for startups or small businesses. They get the convenience of a card without credit lines or interest. It also avoids surprise bills from credit card usage.

Enhanced Security

If someone loses a prepaid card or it gets stolen, the maximum loss is the money on the card. It doesn’t affect the company’s main bank account. These cards usually come with PINs and chips for added protection. RBI also asks card issuers to give loss coverage, just like with debit cards. This makes company funds safer than giving cash or employee debit cards linked to bank accounts.

Cashless Operations

Going cashless reduces the hassle of managing petty cash. Prepaid cards work like corporate wallets. They can be used at POS machines, online, or even at ATMs.

Companies don’t need to keep petty cash or handle reimbursement manually. Employees can use these cards for meals, vendor payments, or travel. They can use them anytime, from anywhere.

In emergencies, they can even withdraw cash within set limits. This keeps daily operations smooth.

Spending Compliance and Control

Prepaid systems allow companies to set rules in advance. They can block certain vendors or categories.

If the card has no funds or a vendor is blocked, the expense won’t go through. This helps enforce spending rules automatically.

For instance, a procurement card can be set to work only with approved suppliers. Any extra spend is denied.

Real-Time Tracking & Reporting

Modern prepaid programs come with apps and dashboards. Each transaction is recorded right away. Managers can see who spent how much, where, and when. This helps with accounting and saves time.

There’s no need to chase lost receipts. Live data also makes it easier to track budgets and spot trends.

Employee Empowerment and Retention

Companies also use prepaid cards as rewards or perks. They can add a bonus to a card or use it to pay wages in advance. Employees can access funds immediately, like for reimbursements or emergency needs. This flexibility boosts employee satisfaction and engagement..

For example, they allow instant bonuses or early wages. This helps improve engagement. More companies now use prepaid cards to recognize employees. Happy and valued employees are more likely to stay.

Branding and Customer Loyalty

Businesses can issue cards with their logo. Each time the card is used, the company brand is visible alongside Visa or Mastercard. Retailers offering gift cards can encourage customers to stay within their brand ecosystem.

Loyalty cards on prepaid platforms encourage repeat shopping. Customers also trust companies more when they offer branded cards. And since these cards work in more than one store, they offer both brand exposure and convenience.

Wide Acceptance

Prepaid cards linked to Visa, Mastercard, or RuPay work almost everywhere. Employees can use them at stores or ATMs in India or abroad. This widespread use means businesses don’t need to worry about location limits.

For example, an employee with an international Mastercard prepaid card can spend in Europe just like in India. The global reach ensures the card works wherever business takes place.

Easy Use and Reload

Prepaid cards are simple to use. You just load money and spend. There are no complex terms or credit rules. Most cards have apps to show balance and past transactions. Reloading is also easy. It can be done through bank transfer, online platforms, or partner stores.

This ease means employees use them comfortably, like a regular debit card. It also helps businesses embed them into payment processes.

Integration and Automation

Today’s prepaid cards work with accounting tools and software. They can connect through APIs. This means expenses are logged as soon as a card is used.

Some systems even sync these transactions with the company’s ERP. This reduces manual entry and paperwork. Prepaid cards can thus become part of a company’s digital finance system with little extra effort.

In summary, prepaid cards help businesses spend smarter. They keep payments cashless and controlled. There’s no credit debt. Budgets stay on track, and companies get real-time insights. Prepaid cards help businesses manage payments, reward people, and even create new income by offering branded cards.

Prepaid Cards in Practice: Business Use-Cases

Modern businesses use prepaid cards in many ways:

Travel and Expense Cards: Companies issue prepaid travel cards to employees going abroad. These cards, often multicurrency Forex cards, lock in exchange rates. They also help avoid ATM cash risks. These cards enable purchases in local currency. Corporations also use domestic prepaid cards for local travel. This helps avoid reimbursements and speeds up expense cycles.

Vendor and Subscription Payments: Instead of relying on expense reports, a firm might give each project lead a prepaid card. The card is loaded with the project budget. The lead uses it for supplier invoices or software subscriptions. There is no need for reimbursement paperwork. When the budget runs out, the card can be refilled on request.

Payroll and Cash Advances: Some companies pay low-wage or contract workers using prepaid payroll cards. This is helpful when workers don’t have bank accounts. These cards remove the need to cut cheques or handle cash. Workers can withdraw money or spend directly. Employers also avoid the hassle of managing cash.

Rewards and Promotions: Retailers often use prepaid cards for loyalty rewards. A customer may receive a reloadable brand card, like a store-issued Visa prepaid card. These cards can accumulate points or cashback. Every time the customer uses it, the brand gains visibility.

Embedded Finance Products: Some innovative businesses now offer prepaid cards as a product. For example, a ride-share firm might partner with a bank. Together, they can issue co-branded prepaid cards. Customers can use these cards for travel or general purchases. This increases customer engagement.

Payroll and Disbursements: Governments and NGOs sometimes distribute welfare payments through prepaid cards. Corporations use them in similar ways. They may issue them for scholarships, refunds, or expense allowances.

Read More: The Digital Journey of Cards from Plastic to Platforms

Online Prepaid Cards

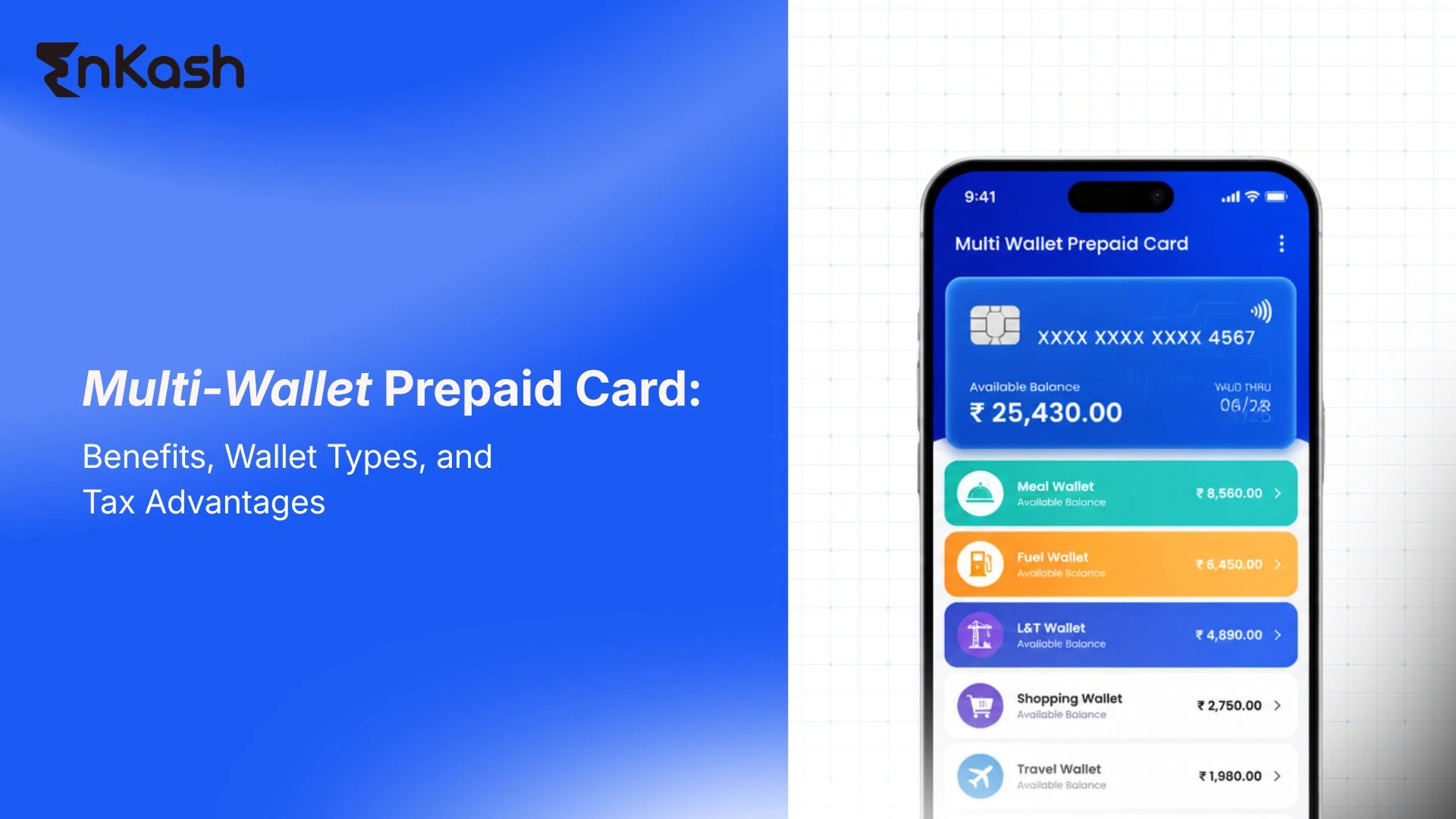

Prepaid cards also come in purely digital forms. Companies can generate virtual prepaid cards that have a card number and expiry date, but no physical form. These cards are ideal for online transactions or limited-use purchases such as trials. An online prepaid card can be created instantly and funded through net banking.

For example, a business might generate virtual cards for each online vendor subscription. This improves security and makes cancellations easier. These virtual cards work like regular cards on checkout pages. They can also be configured as disposable or single-use cards to enhance security and prevent fraud.

Virtual prepaid cards are digital-only payment instruments. You can generate and load them online. They are usually issued instantly after basic KYC. You immediately receive a 16-digit card number, CVV, and expiry date. You preload a fixed balance onto the card. This amount becomes your spending limit. Since the value is set in advance, overspending is not possible. If fraud happens, the loss is limited to the amount loaded.

Instant Issuance: One major benefit is that these cards can be created online in just a few seconds. After simple verification, often through OTP, the card details are issued instantly. You don’t have to wait days for a physical card. Once you set it up, the virtual card is ready to use.

Spending Limits & Budgets: Virtual cards automatically enforce budget limits. You choose how much to load, like ₹5,000. That becomes the card’s maximum spendable amount. Businesses can issue cards to each department or project with their own budgets. They can even assign sub-limits, like a ₹1,000 grocery card. This makes it easy to control how much can be spent.

Expiration and Validity: Most virtual cards have short expiry periods or expire after one use. Some are single-use cards. They expire right after one transaction. Any unused amount is returned to your account. Others remain valid for a few weeks or months.

Single-Use vs. Reloadable: You can choose between single-use and multi-use cards. A one-time virtual card is discarded after the first purchase. This is useful for gift cards or paying one-time vendors. A reloadable virtual card works more like a prepaid debit card. You can keep adding funds and using them for many transactions. These are good for regular expenses like travel or meals. Many platforms offer both options. This allows you to use single-use cards for safety and reloadable ones for ongoing needs.

Prepaid Cards in India Today

India’s market for prepaid cards has grown quickly. RBI’s new rules have helped launch many top-quality prepaid products for both businesses and consumers. Today, banks such as SBI, HDFC, Axis, and others offer corporate prepaid cards. Fintechs and payment networks offer their own versions, too. The “best prepaid card in India” depends on what you need. Some cards are great for international travel, like multi-currency Forex cards. Others are better for managing domestic expenses using apps.

India’s digital growth, including UPI and e-wallets, supports prepaid cards well. Businesses can connect prepaid cards to UPI payments or other digital payment systems for fast reloading.

Conclusion

Prepaid cards combine the ease of using cards with the control of using cash. For today’s businesses, especially in India’s fast-changing fintech space, they are a smart solution for managing expenses and payments. Prepaid cards remove the risk of debt. They integrate seamlessly with digital systems, offering flexible payment options for both employees and customers. These cards have become essential tools for modern companies. They help streamline spending, increase security, and even open new ways to earn by offering branded cards.

In short, a prepaid card is simply a card loaded with money in advance. For businesses, it offers an efficient, secure, and controlled way to send or receive payments. With wide acceptance, online access, and multi-currency features, prepaid cards are changing how companies manage money, from budgeting to employee rewards.

FAQs

1. Can prepaid cards be used to build credit history in India?No, prepaid cards do not help in building a credit history. Since they do not involve borrowing or repayments, credit bureaus do not track their usage. For building credit, tools like secured credit cards or traditional loans that report to credit agencies are more suitable.

2. What happens if a prepaid card expires with the balance remaining?If your prepaid card expires while still carrying a balance, most issuers allow you to request a replacement or transfer the funds. However, terms may vary. Always check the card’s expiry date and issuer’s refund or renewal policy in advance to avoid losing funds.

3. Are prepaid cards safer than using cash for businesses?Yes, prepaid cards are generally safer than cash. They reduce the risk of theft or misuse since spending is limited to the preloaded balance. Most cards also include PIN protection, transaction tracking, and loss recovery options, making them more secure for managing company expenses.

4. Can prepaid cards be used for recurring payments like subscriptions?Yes, some reloadable prepaid cards can be used for recurring payments, such as software or service subscriptions. However, single-use or disposable cards may not support this. Businesses should ensure the card remains funded and check with the issuer if recurring billing is supported.

5. Do virtual prepaid cards have the same legal protection as physical ones?Yes, virtual prepaid cards typically offer the same legal protection under RBI’s guidelines as physical cards. They follow the same rules around KYC, transaction security, and consumer rights. As long as the issuer is licensed, both card formats are treated equally in terms of usage and protection.