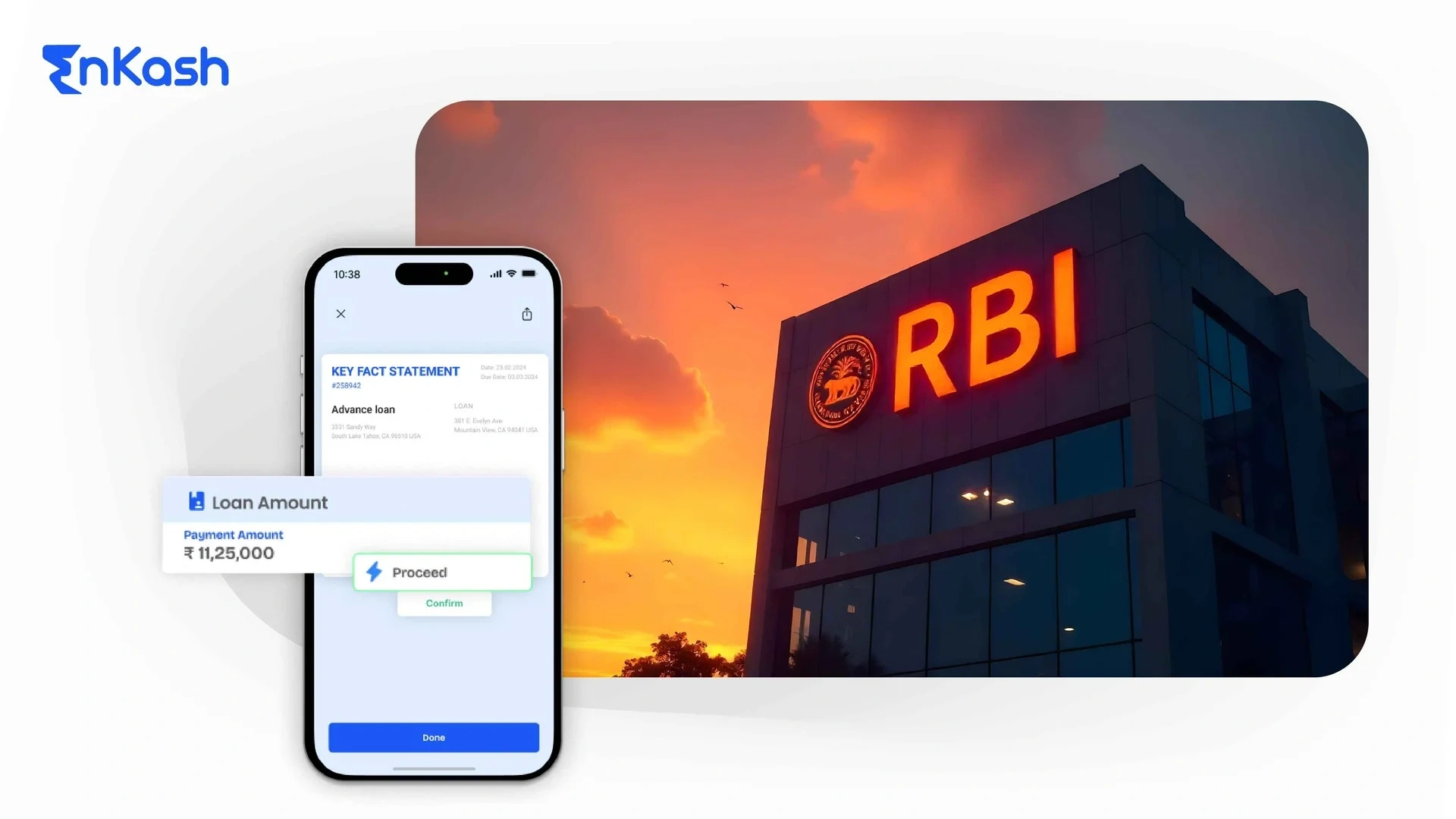

On Monday, the Reserve Bank of India (RBI) introduced a new regulation aimed at simplifying loan information for borrowers. This initiative called the Key Fact Statement (KFS), will be mandatory for all new retail and MSME term loans sanctioned on or after October 1, 2024. This move aims to enhance transparency and make it easier for borrowers to understand the true cost of borrowing.

What is a Key Fact Statement (KFS)?

A KFS is a standardized document provided by lenders (banks, NBFCs etc.) to borrowers in a clear and easy-to-understand language. It summarizes the key facts of a loan agreement, empowering borrowers to make informed financial decisions.

The KFS will include details like:

- Loan amount and type

- Disbursement schedule

- Loan term (duration)

- Repayment details (instalment amount, commencement date)

- Interest rate (fixed, floating, or hybrid) with calculation for floating rates

- All applicable fees and charges (both from the lender and third parties)

- Annual Percentage Rate (APR) – representing the total cost of borrowing

- Details of contingent charges (prepayment penalties, foreclosure charges, etc.)

- Grievance redressal mechanism details

Implementation And Applicability

The RBI’s directive mandates that all REs, including Commercial Banks, Co-operative Banks, and Non-Banking Financial Companies (NBFCs) (including housing finance companies), implement the KFS for all retail and MSME term loan products. The applicability of the KFS extends to all new loans sanctioned on or after October 1, 2024, without exceptions. REs are required to establish robust systems and processes to ensure full compliance with these guidelines. While the KFS covers a wide array of loan products, credit card receivables are exempted from these provisions.

Fees & Charges

The KFS prominently displays the Annual Percentage Rate (APR). This crucial metric factors in all applicable interest rates and fees, giving you a clear picture of the total cost of borrowing. This includes charges levied by the lending institution itself as well as those recovered on behalf of third-party service providers (like insurance or legal charges). These charges are factored into the APR but are also disclosed separately for your reference. Additionally, the lending institution must provide you with receipts and related documents for any third-party service provider charges within a reasonable timeframe.

The KFS ensures you are aware of all applicable fees and charges upfront. This means that the lending institution cannot charge you any additional fees or charges beyond those outlined in the KFS during the loan term unless you explicitly agree to them.

Validity Period

The KFS comes with a unique proposal number and a validity period. This period gives you time to review the KFS thoroughly and ask any questions you may have. For loans with a term of seven days or more, the validity period is at least three working days. For shorter loans (less than seven days), the validity period is one working day. During this timeframe, the lending institution (referred to as “RE” in the circular) is bound by the terms outlined in the KFS if you agree to them.

Benefits of KFS for Borrowers

Informed Decisions: KFS empowers you to compare loan offers from different lenders and choose the one that best suits your needs

Clear Communication: No more hidden charges or confusing terms. The KFS ensures you understand exactly what you’re signing up for

Better Budgeting: Knowing the APR helps you plan your finances effectively and avoid any unexpected costs