Introduction

Business has changed in India. There was a time when customers paid mostly in cash or by cheque. Today, people scan QR codes, tap cards, or pay directly from their phones using UPI. For small and mid-size businesses, the way money comes in has shifted completely.

Whether it’s a home-run boutique, a tuition center in a small town, or an online seller of handmade goods, accepting payments online isn’t a luxury anymore. It’s part of everyday survival. The good thing is that the tools available now make it easier than ever. The challenge is understanding what fits best.

This blog explores the journey of how businesses in India can simplify payments from UPI-based systems to full-stack payment sites and platforms. Along the way, it highlights how options like easy payment gateway tools, payment aggregators, and secure payment systems are quietly changing the game for businesses of all sizes.

The Shift in Indian Payments: From Cash to Clicks

India’s payment behavior has undergone a quiet revolution. Earlier, many businesses operated strictly in cash. Card swipes were most commonly seen in large cities. However, even tea stalls now have QR codes, and many kirana stores accept mobile payments.

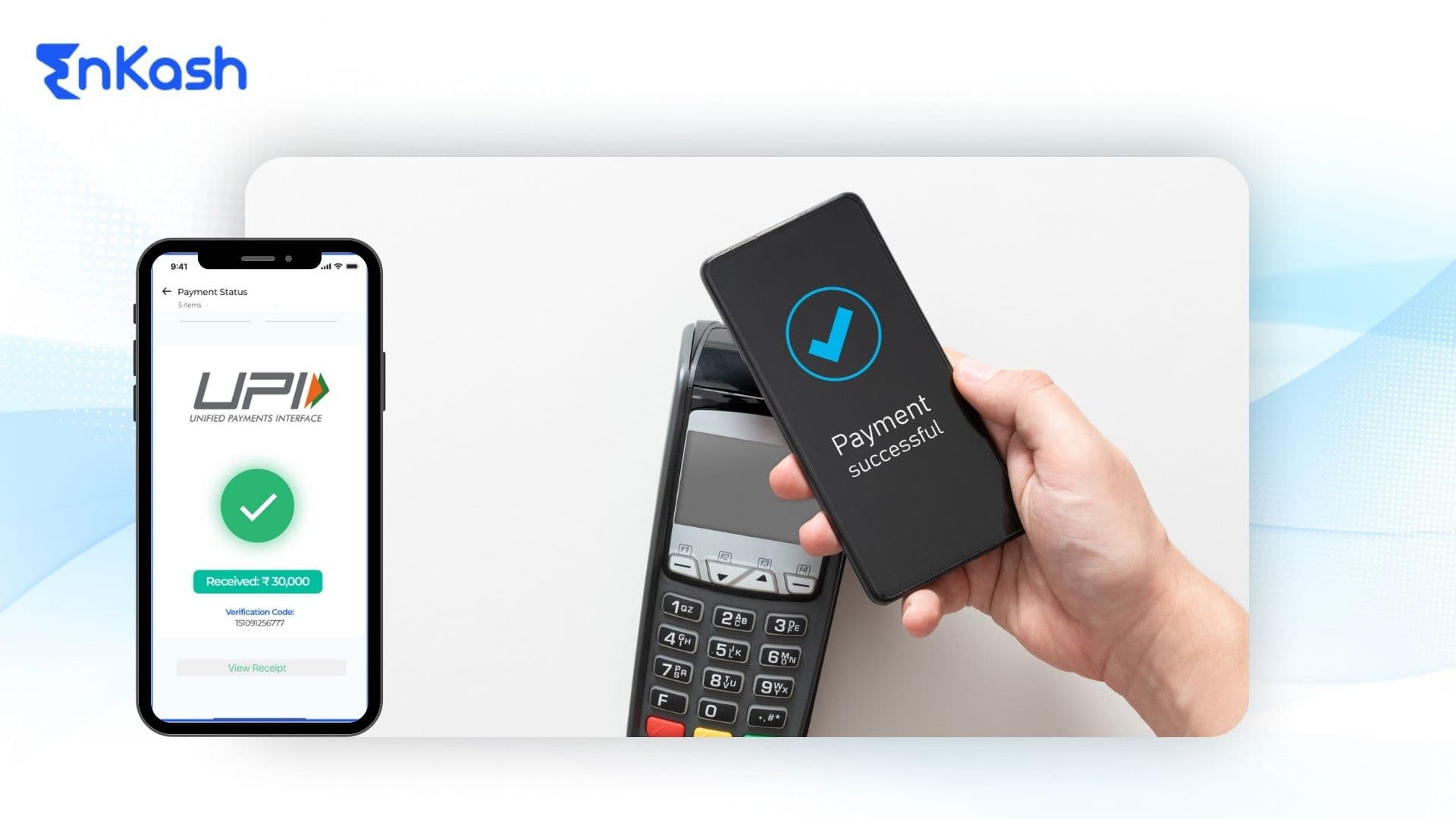

UPI has played a big role in this. It made payments real-time, reduced the need to share bank details, and made it possible for anyone with a smartphone to send or receive money in seconds. This opened the door for millions of small businesses to go digital without expensive setups.

But not every customer uses UPI. Some still prefer cards, net banking, or even cheques. It’s important to offer more than one way to pay. At that point, using payment sites and apps becomes useful for handling all kinds of payments.

What Makes a Payment Gateway Easy?

A business payment gateway lets money move from the customer to the seller, securely and quickly. It can be as basic as a UPI-based QR code or as detailed as a dashboard that tracks multiple payment sources, settlements, and refunds.

But what makes it easy? It’s not just about being fast. For most businesses, ease means:

- No lengthy setup or paperwork

- Fast onboarding

- Options for different kinds of customers

- Clear settlement timelines

- Transparent pricing

- Reliable support when things go wrong

The gateway should do its job quietly, without adding friction. If a customer can't pay or if the business owner doesn’t understand the system, that’s lost trust and money. Simplicity builds confidence. Especially when the business owner is juggling stock, delivery, bills, and customer service all at once.

EnKash makes it simpler for businesses to manage payments without adding extra layers of complexity. With customisable features that suit different operational needs and scalable options that can grow alongside a business, it fits into existing systems much like flexible API-based solutions. What also helps is that support isn't just automated responses; real people are available to guide when needed, making issue resolution feel less mechanical and more reliable.

Payment Aggregators in India: A Quiet Backbone

A payment aggregator connects businesses to multiple payment methods through one account. This removes the need to set up links with different banks or payment networks separately. Payment aggregators simplify backend integration and centralize access to multiple payment methods, although onboarding and compliance steps are still necessary.

In India, these aggregators are often used by:

- Online sellers

- Local service providers

- Coaching centers

- Subscription-based platforms

They let a business accept UPI, cards, wallets, and net banking from a single dashboard. Many also offer tools like payment links, invoices, recurring billing, and refund management.

For small businesses with limited resources, these features reduce time spent chasing payments or manually tracking transactions. The aggregator handles all the back-end work.

What’s the Difference Between a Payment Gateway and a Payment Aggregator?

These two terms sound similar. Many people think they’re the same thing. But they do different jobs in the online payment process.

A payment gateway is just the technology that helps a payment go from the customer to the business. It checks if the payment details are correct, sends the request to the bank, and tells both sides if the payment worked or failed. It’s like a digital messenger that carries payment info safely.

A payment aggregator, on the other hand, is a service that collects the money from the customer and then passes it on to the business. Instead of the business talking to different banks one by one, the aggregator handles everything in the middle.

| What to Compare? | Payment Gateway | Payment Aggregator |

|---|

| What it does | Moves the payment safely from one side to another | Collects the payment and sends it to the business |

| Who needs it | Used by all online businesses | Helpful for businesses that don’t have direct bank tie-ups |

| Handles money? | No, just moves the request | Yes, holds and settles the money |

| Is it regulated? | Yes, needs to be secure (like encrypted) | Yes, needs RBI approval and follows strict rules |

| Good for? | Secure and fast payments | Easy setup and all-in-one payment collection |

In real life, both are usually used together. For example, a small shop that takes card payments or UPI might be using a payment gateway provided by an aggregator, all in one app.

In 2022, the RBI made it clear that only licensed aggregators could handle customer funds. This made things more secure but also formalised the space. Now, most online payment apps in India work as aggregators. Gateways still exist, especially for businesses that want to build their own tech layer on top.

So, how does a business decide?If there’s a tech team, custom platform, or need for deeper control a gateway setup might make sense

If the goal is to start fast, use readymade tools, and manage everything in one dashboard aggregator is usually easier

It’s not really about which one is better. It’s about what works based on scale, time, and resources. And for many small or mid-size businesses, getting started with an aggregator is often the more practical choice.

Payment Aggregators in India: A Quiet Backbone

A payment aggregator connects businesses to multiple payment methods through one account. This removes the need to set up links with different banks or payment networks separately. Payment aggregators simplify backend integration and centralize access to multiple payment methods, although onboarding and compliance steps are still necessary.

In India, these aggregators are often used by:- Online sellers

- Local service providers

- Coaching centers

- Subscription-based platforms

They let a business accept UPI, cards, wallets, and net banking from a single dashboard. Many also offer tools like payment links, invoices, recurring billing, and refund management.

For small businesses with limited resources, these features reduce time spent chasing payments or manually tracking transactions. The aggregator handles all the back-end work.

Real-World Examples of How Indian Businesses Use Gateways

1. A Tailoring Boutique in NagpurThey use a UPI QR code for walk-ins. For bulk orders, the owner sends a payment link over WhatsApp. The gateway dashboard shows which payments are pending. No need to maintain a manual register.

2. An Online Language Tutor in KeralaThe tutor offers monthly packages. Students pay using cards or net banking. The platform uses a payment aggregator to automatically collect payments every month.

3. A Small Cafeteria in BhopalThe cafe accepts UPI, cards, and wallet payments using a single payment app. At the end of the day, they check the settlement report to match sales. No extra staff needed to handle accounts.

These aren’t high-tech businesses. They are regular people using simple tools to make payment collection faster and smoother.

What to Look for in a Payment Gateway

Every business has different needs. But there are a few things that matter across the board.

1. Cost and Hidden ChargesSometimes, the cheapest payment gateway upfront may end up costing more in the long run. It's important to check for hidden fees like:

- Setup charges

- Maintenance fees

- Charges for failed transactions

- Settlement delay fees

Low transaction charges are attractive, but clarity matters more than just cheap rates.

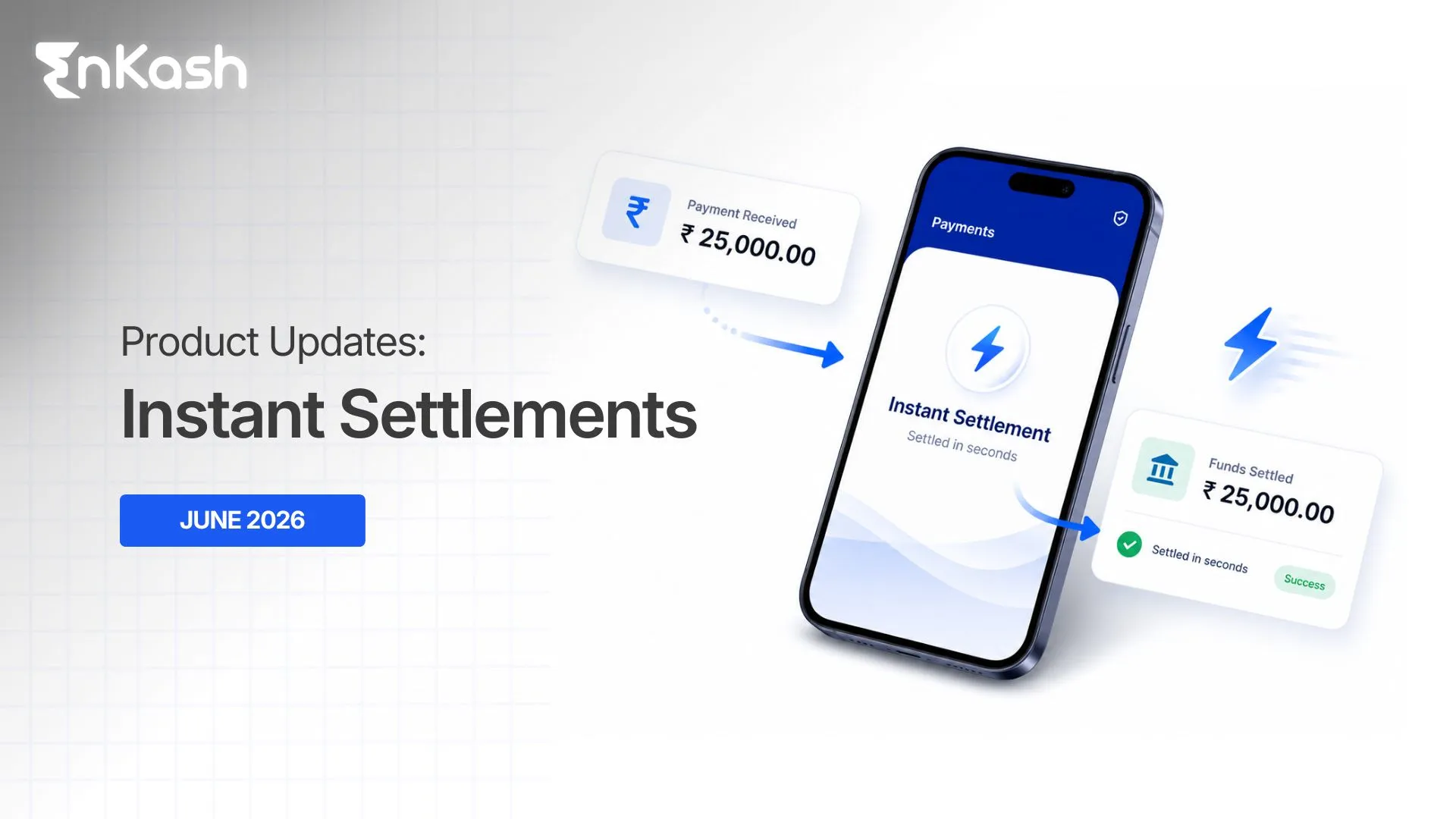

2. Speed of SettlementSome gateways settle funds on the same day. Others take 2–3 working days. A business that depends on daily cash flow needs fast settlement. Waiting for a week can slow down everything, from paying suppliers to managing staff wages.

3. Ease of UseIf the platform is difficult to understand or full of technical terms, it will slow things down. Many small businesses work with limited digital knowledge. A simple layout, clear options, and regional language support can go a long way.

4. Customer SupportPayment failures and delays can frustrate both the customer and the business. Having access to real support, not just automated replies matters. Especially during peak hours or festival seasons.

5. Security FeaturesA secure payment gateway must be PCI-DSS compliant and should support features like tokenization, real-time fraud detection, and multi-factor authentication. Things like SSL encryption, OTP-based approvals, and fraud detection mechanisms are now basic requirements.

Also Read:

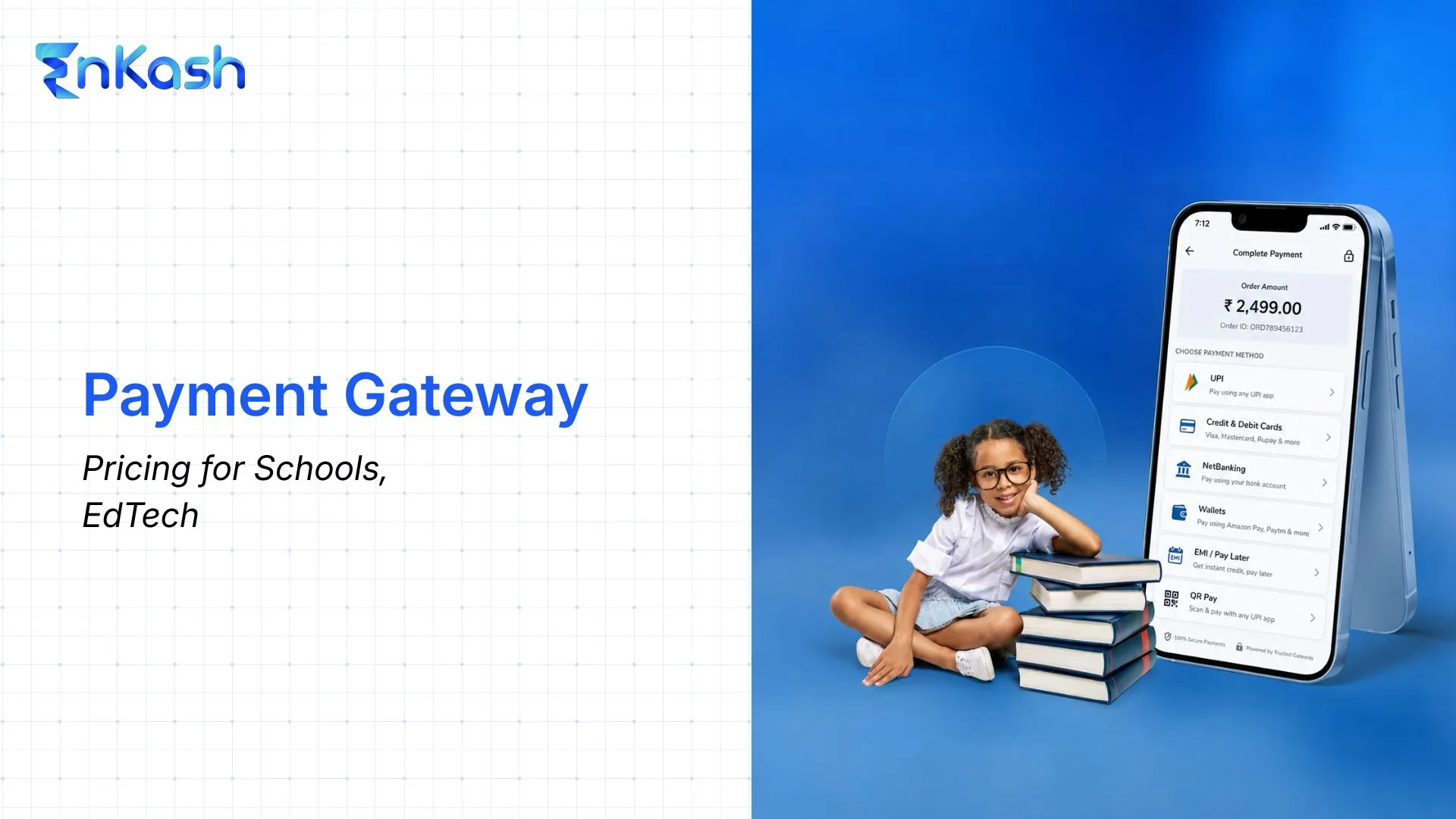

How to Choose the Best Payment GatewayCommon Payment Options Available Through Gateways

- UPI Gateway: Great for instant, small-ticket payments. Works well for retail and services.

- Cards (Debit and Credit): Needed for higher-value payments or EMI-based purchases.

- Net Banking: Some older or business customers prefer this for a more “official” feel.

- Wallets: Popular with younger customers. Useful for recharge or quick purchases.

- EMI/Buy Now Pay Later: Useful for education, electronics, and wellness industries.

- Pay by Check Online: Some businesses may request traditional NEFT/RTGS transfers as they resemble old cheque-based settlements in documentation and flow. It's slow but sometimes necessary.

A smart payment gateway should support at least three to four of these, based on customer type.

Why Do Some Payments Take Longer to Settle?

Most people assume online payments are instant. But anyone running a business knows just because a customer pays at 3 PM doesn’t mean the money hits the account right away.

So why do delays happen?There are a few common reasons. Some gateways follow T+1 or T+2 settlement cycles, which means the money is settled one or two working days after the transaction. If there's a weekend or bank holiday in between, the wait gets longer. Some tools also have different timelines based on the payment method. UPI might settle faster than a credit card.

The RBI does have rules around settlement. Aggregators need to stick to defined timelines, and they’re expected to keep merchant money separate from their own. This is to prevent situations where a business doesn't get paid because the platform messed up its own finances.

But even with these rules, delays still happen. Sometimes it’s because the business hasn’t finished full KYC. Or there’s a flag on a high-value transaction. Or there’s an issue at the customer’s bank end.

For small businesses, even a one-day delay can affect daily cash flow.

Especially when the money is needed to restock, pay vendors, or manage wages.

So before signing up with any gateway or aggregator, it’s worth asking:

- What’s the standard settlement time?

- Do weekends or holidays affect it?

- Will UPI settle faster than cards?

- Are there payout thresholds or minimum balances?

Sometimes, just getting these answers upfront saves a lot of stress later.

RBI Compliance Isn’t Optional Anymore

There was a time when small shops and online sellers didn’t think much about compliance. As long as payments came in, that was enough. But things have changed. Today, if a payment service isn’t following RBI rules, it could block or delay business payments sometimes without warning.

The Reserve Bank of India (RBI) has made it clear: payment aggregators need a valid license to operate. They must also meet strict conditions like:

- Keeping merchant money in separate escrow accounts

- Following proper KYC and business verification

- Settling money within the allowed time frame

- Reporting transactions transparently

These aren’t just rules on paper. In 2023 and 2024, the RBI even paused or restricted several payment services that weren’t meeting these requirements. When that happens, businesses using those platforms suffer payments stop, refunds are delayed, and trust is lost.

For small and mid-size businesses, this becomes even more important. Many rely on one single provider to accept payments, issue invoices, track customer dues everything. So if that provider isn’t compliant, the entire system can get stuck.

Now, how to know if a provider is compliant?

- Check if they’re listed as an RBI-approved aggregator

- Look for clear KYC, onboarding steps

- Ask how they handle merchant funds

- Avoid platforms that skip due diligence just to get started quickly

It may feel like a longer process upfront, but it’s safer in the long run. Compliance isn't just about ticking boxes. It’s about knowing the money comes in on time without getting stuck, the data is secure, and the business won’t suddenly get stuck during a routine transaction.

This part often confuses people, especially those who are just starting to accept payments online. Many see one big number deducted from each payment and assume it's a flat fee. But it usually isn’t that simple.

There are two types of charges that typically apply: settlement charges and platform or service fees. They sound similar but serve different purposes.

Settlement charges are what the provider takes for processing and settling the payment to the business account. It's linked to how the money moves, UPI, card, net banking, wallet, etc. Each method may have a different cost. For example, UPI might have no charge, while a credit card transaction may come with a small percentage cut.

On the other hand, platform fees cover the tools and services that come with the gateway things like dashboards, invoice creation, auto-reminders for customers, recurring billing, or even simple things like daily payout reports. Some providers include these in the transaction fee itself. Others show it separately. It depends on the model.

And then there’s GST on top of all that. That gets added to whatever the provider charges. Not many talk about it, but it shows up in the invoice at the end of the month.

Why is it important?

Because for a business running on tight margins, even a small difference in fee structure changes the math. Imagine receiving ₹10,000 in online payments daily. If one provider takes 2% and another 1.5%, that’s a ₹150 difference every single day. Over a month, that’s ₹4,500 gone.

So, before choosing a platform, it's worth asking:

- What is the actual % cut on each payment type?

- Are there fixed charges per transaction?

- Are there monthly platform or software fees?

- Is GST included in the quoted rate, or added later?

Sometimes providers show only the base transaction fee up front. Everything else appears in fine print or later invoices. Reading the full pricing breakdown saves money and surprises.

Conclusion

Running a business in India today means staying in step with how people like to pay. Cash still works, but now many walk in expecting UPI, cards, wallets, or even payment links. The shift is already here. What matters is how smoothly a business handles it.

Choosing a payment setup isn’t about using the fanciest tool. It’s about picking something that quietly fits into daily work. No extra headache. Just something that makes it easier for customers to pay and for owners to stay on top of things.

There’s no one-size-fits-all. Some businesses need just a QR code. Others need more tracking, reminders, maybe recurring payments. Either way, if it reduces friction and builds trust, it’s doing its job.

Payments are no longer just about money coming in. They’ve become part of how a business runs. The easier the flow, the more time and energy stays focused where it’s needed.

FAQs

1. Can small businesses use payment gateways without a website?Yes. Many modern gateways let merchants use payment links, QR codes, and mobile apps. A website is helpful, but not required.

2. Is UPI better than card payments for small stores?It depends on the customer. UPI payment is faster and has lower charges. But cards may be preferred for large purchases or EMI-based deals.

3. How safe is it to accept payments through aggregators?If the aggregator is RBI-compliant and uses SSL encryption and 2FA, it is generally safe. Always check reviews and settlement timelines.

4. What is the average transaction fee for payment gateways?Most UPI transactions are free for small merchants. However, some PSPs may charge nominal fees (e.g., 0.3%–0.5%) for large-volume merchant accounts

5. Can someone still pay by cheque in a digital system?Some platforms offer cheque-style payment simulations through net banking. Mostly used by enterprises or traditional clients.