Introduction

Digital payments in India have transformed how people and businesses handle money. From small purchases to large transactions, payments now happen in seconds — quick, secure, and completely cashless. Customers across India expect the same ease everywhere, whether they’re shopping online,

paying utility bills, or

managing subscriptions.

For businesses, this shift has created new opportunities but also complex challenges. Building a digital wallet in-house requires regulatory approvals, multiple banking partnerships, and continuous audits. Wallet integration becomes even more demanding when businesses attempt to manage compliance, settlement flow, and KYC layers on their own.

Wallet as a Service (WaaS) enables businesses to launch a compliant, co-branded digital wallet through simple wallet APIs, without building the underlying infrastructure. Businesses can embed wallet capabilities directly into their apps and platforms, reducing development time and operational load.

In a country where UPI processes around 19 billion transactions each month (as per RBI data), WaaS supports the growing need for fast, reliable, and integrated digital payment experiences in India.

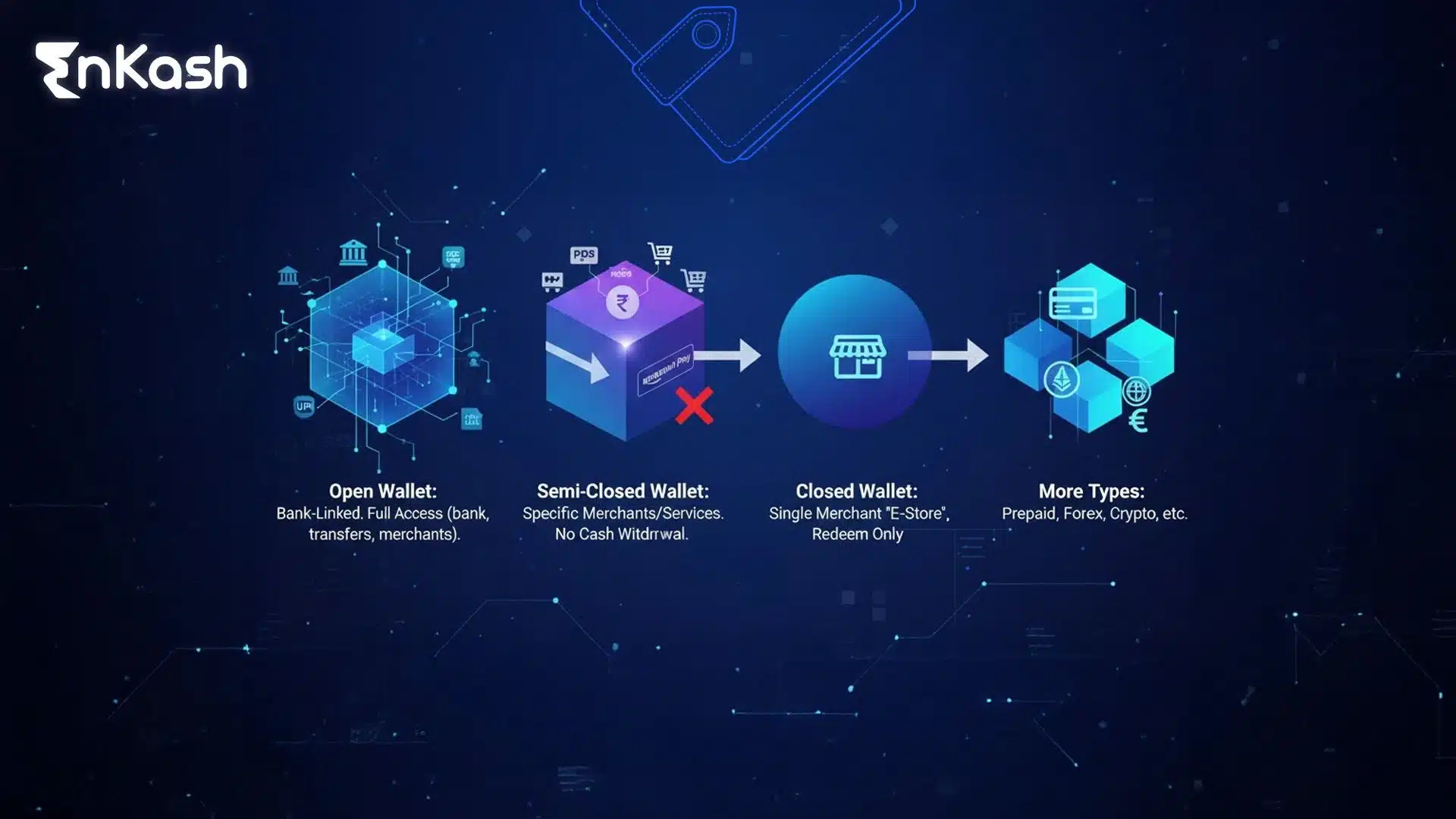

Get Co-Branded WalletsWhat is Wallet-as-a-Service (WaaS)?

Wallet-as-a-Service (WaaS) is a pre-built platform that enables businesses to quickly and securely launch their own digital wallets. Instead of building a wallet from the ground up, managing licenses, and connecting with multiple banks, a company can use a WaaS provider that already has the technology and regulatory approvals in place. The partners can simply procure the API from the digital wallet service provider, aka the WaaS provider. The wallet API is then integrated into the respective apps, and your co-branded digital wallet is ready.

With WaaS, all the key functions of a wallet, like creating accounts, loading money, making payments, processing refunds, or even issuing cards, are available through simple APIs or SDKs. This means a business can offer its customers the same smooth experience as any leading digital wallet, but without the long setup time or compliance challenges.

The provider handles everything in the background from RBI regulations and KYC verification to settlements, reconciliation, and reporting. Businesses get a secure and compliant wallet system that’s ready to use, while focusing their time and effort on building products, features, and growth.

WaaS is becoming an essential part of India’s digital ecosystem. As more platforms want to embed payment features and manage user balances directly, WaaS gives them the power to do it faster, more safely, and without depending on traditional banking infrastructure.

Watch this short video to understand WaaS.

How Wallet-as-a-Service (WaaS) Works

Every time a user pays through a digital wallet, there is a complete flow working in the background. A Wallet-as-a-Service provider builds the wallet infrastructure and APIs, while the business integrates these APIs into its own app or platform. The result is a fully branded, open-loop digital wallet that operates inside the business’s existing ecosystem.

Here’s how the flow works:1. API Built by WaaS Provider, Integrated by the Business

The WaaS provider builds the core wallet APIs and compliance infrastructure.The business integrates these APIs into its app, website, or internal systems. This creates a co-branded digital wallet that lives entirely inside the business’s platform with its own UI, branding, and workflows.

2. Wallet Created Inside the App

Once the integration is complete, a wallet account is created for each user inside the business’s app.

The wallet is issued under the provider’s RBI-approved PPI license, ensuring it is compliant from day one.

3. KYC Completed to Activate the Wallet

To activate the wallet, users complete KYC as per RBI norms.

This can be done through digital onboarding and real-time verification.

Once KYC is approved, the wallet becomes ready for transactions.

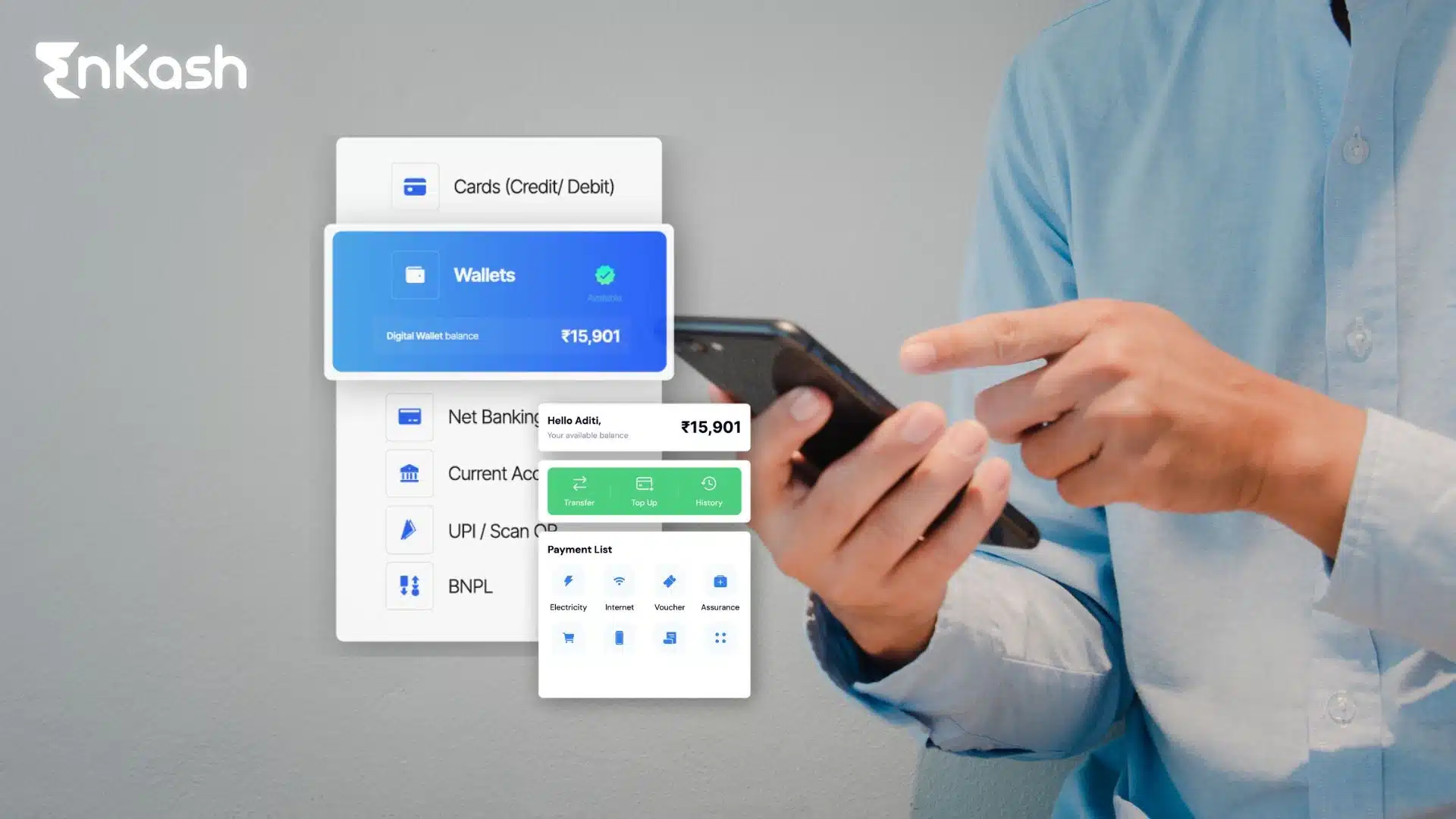

4. User Loads Money

Customers can add money via UPI, cards, or bank transfers.

The funds are stored in an RBI-regulated prepaid account linked to the co-branded wallet.

5. Payments Are Made Using the Open-Loop Wallet

A fully activated open-loop wallet allows users to pay for a wide range of utilities and services, such as: electricity, water, DTH, mobile recharge, online purchases, subscriptions, travel and more.

The WaaS system routes every transaction through secure, compliant payment rails.

6. Funds Are Settled to the Merchant

After the payment is made, the merchant receives funds from the wallet’s escrow account. Settlements follow RBI rules, generally within T+1 timelines. All transactions are reconciled in real-time for audit and reporting.

7. Compliance and Monitoring Stay Automated

All KYC data, ledger entries, settlement records, and transaction logs are automatically stored as per RBI requirements.

Businesses do not need separate compliance systems or audits.

In short, WaaS brings together users, businesses, banks, and regulators on one secure, unified system. It allows companies to run their own wallets with all the checks, balances, and protections already in place.

Why Businesses in India Are Choosing WaaS (Wallet as a Service)

Digital payments in India are growing faster than ever. The UPI network alone handled more than 19 billion transactions in a single month, and instant, cashless payments have become a normal part of everyday life. As customers expect speed and convenience in every app, more businesses are looking for ways to offer built-in wallet experiences.

Building such a system independently can take months and requires deep regulatory knowledge. Wallet-as-a-Service (WaaS) offers a faster and more reliable alternative. It allows businesses to launch compliant, ready-to-use wallets without spending resources on complex setups or multiple partnerships.

Key reasons businesses are choosing WaaS:

- Faster launch timelines

A pre-built and regulated system allows wallets to go live within weeks, helping businesses respond quickly to market needs.

- No license or compliance effort

The platform already operates under RBI approval, removing the need for separate PPI or PA licenses, audits, or escrow accounts.

- Reduced operational cost

One unified platform replaces several vendors and integrations, cutting both time and expense.

- Improved customer engagement

Wallets make payments effortless, support cashback and loyalty programs, and keep customers returning.

- Scalability and reliability

WaaS platforms are built for high uptime and performance, even during peak transaction loads.

WaaS has become a practical choice for any business that wants to simplify payments, reduce operational effort, and deliver a seamless experience in India’s growing digital economy. Among the growing number of digital payment solutions in India, few offer the combination of regulatory approval, technology depth, and enterprise reliability that businesses truly need. EnKash brings all these strengths together as a trusted and licensed provider of Wallet-as-a-Service infrastructure.

EnKash is one of the few fintech companies in India authorized by the Reserve Bank of India (RBI) to operate as both a

Prepaid Payment Instrument (PPI) issuer and a

Payment Aggregator (PA). These licenses form the regulatory base that powers its full-stack Wallet-as-a-Service platform.

Designed for both scale and compliance, EnKash allows businesses to build and manage wallets, prepaid cards, vouchers, and payouts through a single, secure platform. It brings together every essential layer, such as licensing, technology, and settlement, into one connected system, helping businesses save time, stay compliant, and focus on expanding their operations.

What EnKash WaaS Is and How It Helps You Launch Your Own Wallet

EnKash Wallet-as-a-Service helps you build and launch your own digital wallet without worrying about licenses, audits, or complex integrations. It’s a complete platform that lets you create secure, compliant, and customizable wallet experiences for your customers, employees, or partners.

The platform is built on a strong regulatory base, operating under RBI-approved Prepaid Payment Instrument (PPI) and Payment Aggregator (PA) licenses. This gives your business direct access to a trusted and compliant payment infrastructure from day one. EnKash also follows PCI-DSS and SOC 2 Type II standards, ensuring that every transaction and customer detail is managed with the highest level of security.

With EnKash, you can launch wallets that support multiple payment use cases from digital payments and refunds to payouts and rewards. The platform also allows the integration of prepaid cards and vouchers, helping you design complete financial ecosystems that fit your brand and audience.

Everything from onboarding and KYC verification to fund settlements and reporting is automated, transparent, and audit-ready. This allows your team to focus on growth, while EnKash handles the technology, compliance, and day-to-day operations behind the scenes.

Key Features That Power EnKash WaaS

EnKash Wallet-as-a-Service brings together everything a business needs to run a compliant and scalable wallet system.

Here are some of the key features of the EnKash platform:

1. Regulated and Secure FoundationBuilt on RBI-approved PPI and PA licenses, EnKash gives you access to a fully compliant wallet infrastructure from day one. The platform also meets PCI-DSS and SOC 2 Type II security standards, ensuring that every transaction, KYC record, and settlement remains protected.

2. Frictionless KYC and OnboardingEnable quick and seamless onboarding round-the-clock KYC. The platform supports instant digital verification and seamless wallet activation, and easy upgrades from minimum to full KYC, keeping the process smooth for every user.

3. Unified Payment and Settlement LayerManage all wallet operations, creation, loading, payments, refunds, and settlements on a single system. The built-in payment gateway integration ensures that fund flow stays fast, traceable, and error-free.

4. Developer-First InfrastructureIntegrate easily with REST and GraphQL APIs and test everything in a dedicated sandbox environment. Real-time webhooks keep your system updated on every event, from transaction approvals to settlement confirmations.

5. Flexible Payment InstrumentsGo beyond wallets with prepaid cards and vouchers linked to wallet balances. These can be used for multiple applications, such as payouts, rewards, and loyalty programs, all controlled and monitored within the same platform.

6. Real-Time Monitoring and ReportingAccess a detailed dashboard for transactions, balances, settlements, and compliance reports. Automated logs and audit trails make tracking and reconciliation effortless.

Together, these features make EnKash WaaS a complete, future-ready infrastructure that blends compliance, control, and convenience, helping your business scale digital payments with confidence.

Real-World Use Cases

A well-designed wallet infrastructure can serve a wide range of businesses, from fast-moving consumer platforms to large enterprise systems. EnKash Wallet-as-a-Service gives every organisation the flexibility to build wallet experiences suited to its users, operations, and goals.

- Gig and Payout Ecosystems

For gig and on-demand platforms, wallets enable instant and transparent payouts to workers and partners. Instead of relying on time-consuming bank transfers, payments can be credited instantly to wallet-linked cards. This improves efficiency, reduces delays, and helps maintain better partner satisfaction.

- Marketplaces and Online Platforms

E-commerce and service marketplaces deal with thousands of daily transactions, refunds, and merchant settlements. A built-in wallet system simplifies this flow — allowing faster refunds, smoother reconciliations, and better control over fund movement. Businesses often report significantly faster transaction processing and lower operational overhead when moving to embedded wallets.

- Education and Campus Networks

Schools, universities, and edtech apps can move towards cashless ecosystems by introducing digital wallets for students, teachers, and staff. From cafeteria payments to transport fees, every transaction becomes easy to trace and manage. Institutions adopting wallet-based systems typically see a sharp reduction in cash handling and greater transparency.

- Consumer and D2C Brands

Retail and D2C brands can use wallets to strengthen customer engagement. Loyalty rewards, cashback, or store credits can be stored in branded wallets, encouraging repeat purchases and long-term retention. Businesses often report up to 25% improvement in repeat purchase rates after introducing wallet-linked rewards.

- Utilities, Travel, and Recharge Apps

Apps that manage utility bill payments, ticketing, or mobile recharges can integrate wallets to process payments instantly and reduce failure rates. Wallet-based payments are faster, support credit card top-ups, and create a smoother user experience across frequent transactions.

Across sectors, Wallet-as-a-Service helps simplify payment operations and improve efficiency for both users and businesses.

Conclusion

Every business is finding new ways to make payments simpler and more connected. EnKash Wallet-as-a-Service brings the stability and structure needed to support that change. It allows businesses to modernise their payment systems without losing focus on what truly matters: efficiency, trust, and growth.

As digital transactions continue to evolve, EnKash remains focused on one goal: making enterprise payments simpler, safer, and built for scale.

Go live with EnKash. Power the next generation of digital wallets.

FAQs

1. What is the full form of WaaS?WaaS full form is Wallet as a Service. It is a ready-to-use digital wallet infrastructure that allows businesses to integrate wallets into their apps through simple APIs instead of building the entire system from scratch.

2. What can an open-loop wallet be used for?Open-loop wallets allow customers to make a wide range of payments such as electricity bills, mobile recharge, DTH, water bills, travel bookings, online shopping, subscription payments, and other utilities commonly used across India.

3. Is KYC mandatory for users in a WaaS-based wallet?Yes. As per RBI guidelines, every user must complete KYC to activate the wallet. WaaS platforms support fast, digital KYC so users can start transacting quickly.

4. What are the benefits of using a co-branded digital wallet for businesses?A co-branded wallet improves customer retention, boosts repeat transactions, supports reward programs, reduces payment failures, and gives businesses more control over user balances and payment flows.

5. What is a Wallet API?A Wallet API is a set of programmable interfaces that allow businesses to create wallets, load money, process payments, issue cards or vouchers, handle refunds, and manage settlements inside their platform.

6. How is Wallet-as-a-Service different from building an in-house wallet?With WaaS, you skip licensing, audits, banking integrations, and complex technical work. The provider already manages these layers, allowing your team to focus on product growth instead of backend compliance.

7. Is EnKash WaaS secure?Yes. EnKash operates under RBI-approved PPI and PA licenses, follows PCI-DSS and SOC 2 Type II standards, and manages settlements through regulated escrow accounts, ensuring end-to-end security.

8. Can small businesses or startups use WaaS?Absolutely. WaaS is ideal for startups and digital-first businesses because it reduces cost, removes regulatory complexity, and offers a fast way to launch a branded wallet experience.

9. Does WaaS support prepaid cards and vouchers?Yes. EnKash WaaS allows businesses to link prepaid cards, vouchers, rewards, and loyalty credits to the wallet balance, enabling a complete financial ecosystem.

10. How does wallet integration benefit Indian apps?Wallet integration ensures faster payments, fewer failures, better conversion, and improved customer stickiness, especially across high-volume categories like travel, recharge, bill payments, food delivery, and e-commerce in India.