What is a Prepaid Wallet?

A prepaid wallet is a digital balance that you load with money before you use it. Think of it as a small payment space on your phone or card that holds a fixed amount you add in advance. People use it for everyday payments, small purchases, or quick transfers without touching their bank balance each time.

The prepaid wallet's meaning is quite straightforward. You add funds through your usual payment method, and the wallet uses that stored amount whenever you pay for something. It feels clean and predictable because you spend only what you have loaded. This setup helps with better control and gives a smooth way to pay without carrying cash.

Many platforms use this format today. It works in ticketing systems, retail payments, transit setups, fuel payments, and digital services. A prepaid wallet also supports tasks like recharges, bill payments, and small online purchases. In some cases, people use a prepaid card wallet for the same purpose. The idea stays the same, the form changes.

This kind of wallet works well for quick checkouts and for people who want a simple payment method without linking every transaction to their bank account. It also supports small-value transactions that need faster clearance.

When linked to transit platforms, the same structure helps users pay toll charges without stopping. Those cases use a prepaid wallet for FASTag. You load the balance, and the toll fee gets deducted automatically whenever the tag is scanned.

The growth of digital payments has made this format common. Newer systems use the same structure to support prepaid digital wallet solutions for businesses, apps, and loyalty systems. This shows how flexible the model is and how well it adapts to new situations.

Explore Prepaid Digital WalletTypes of Prepaid Wallets in India

A prepaid wallet can take different forms, and each one serves a slightly different need. The core idea stays the same. You load money in advance, and the system uses that stored amount whenever you pay for something. The variety lies in how the wallet is shaped and where it is used.

App-based Prepaid Wallets

These are the digital wallets people use through mobile apps. They hold a stored balance that works for recharges, shopping, bill payments, transport, and small everyday transactions. The process feels simple. You top up the balance, and the app processes the payment whenever you choose an item or service. Many users prefer this format because everything stays within the app.

Get a Prepaid Wallet For AppPrepaid Card Wallets

A prepaid card wallet works through a physical or virtual card. You load the card with a fixed balance and then pay with it at stores or online. Businesses use this format for employee spending because it gives clear control and helps track expenses without mixing company and personal payments. Individuals use these cards for daily purchases or travel based on their needs.

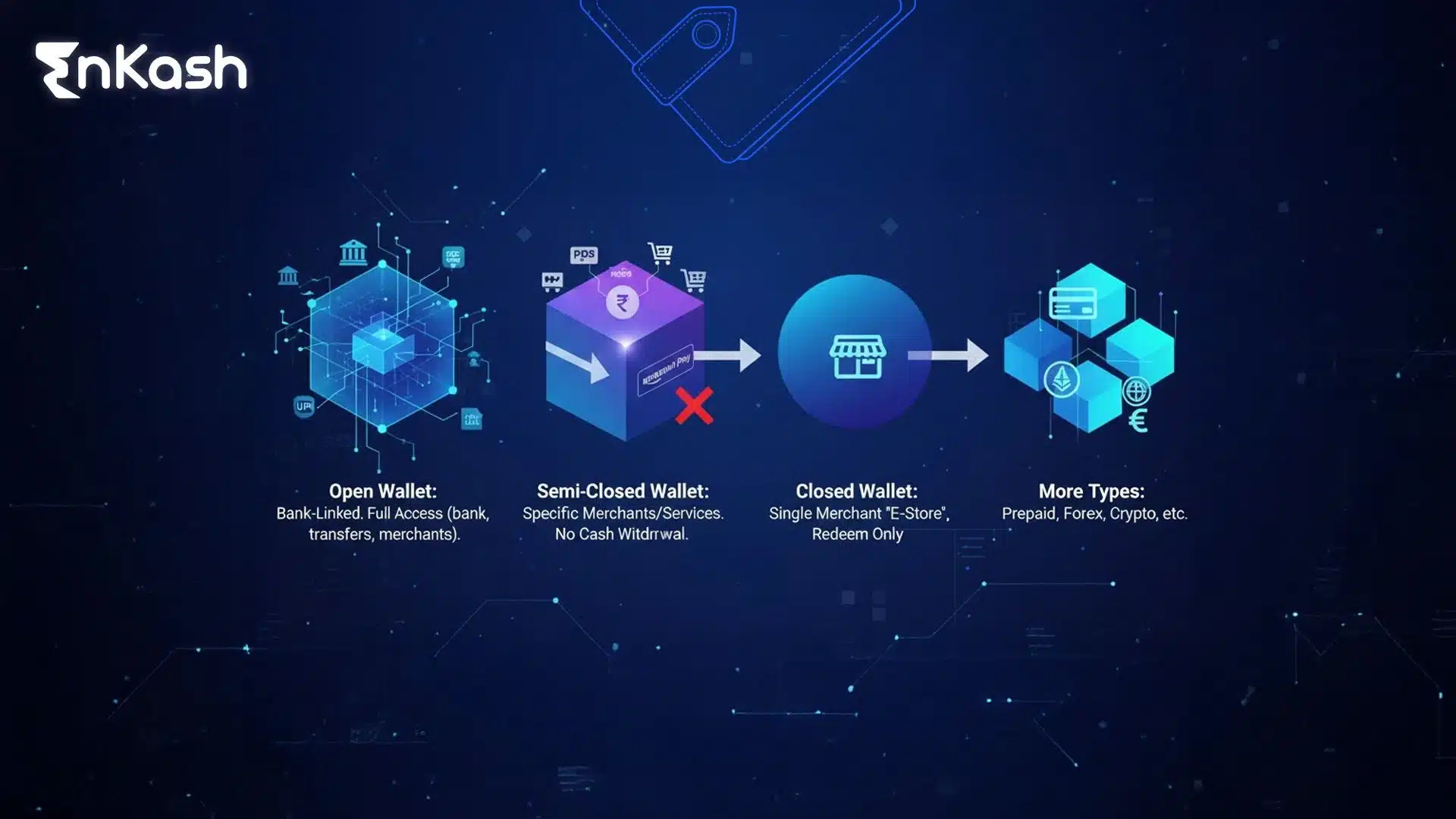

Closed, semi-closed, and open wallets

These categories are defined in RBI’s Prepaid Payment Instrument (PPI) framework.

Closed wallets hold value that can be used only within the same platform and are not classified as payment systems, so their issuance does not require prior RBI authorization.

Semi-closed wallets work across a wide network of merchants and are common in daily digital payments.

Open wallets support a larger set of services and allow cash withdrawals under specific conditions. They follow strict verification rules and serve broader use cases.

Prepaid Wallet for FASTag

A prepaid wallet for FASTag supports toll payments made without stopping at plazas. You load the amount before your trip, and the toll fee is deducted when the tag is scanned. This structure works well for regular commuters because the balance moves automatically and keeps the vehicle lane clear. It also supports quick recharges through digital channels.

These are the main forms that give structure to a prepaid wallet today. Each format has its own purpose, but the underlying idea stays simple. You load the balance first and use it wherever the wallet is accepted.

How Prepaid Wallets Work

A prepaid wallet runs on a simple flow. You add money first, and the system uses that balance each time you pay. The experience feels quick because the wallet does not ask for repeated bank verification for every small payment. It draws from the stored value and completes the transaction in a clean and steady way.

Loading Money

People load money through the usual digital methods. It could be through a payment card, net banking or a transfer from a linked account. Some users prefer using a mobile payment route for convenience. The amount reflects in the prepaid wallet almost instantly, which makes it easy to top up whenever the balance drops.

Making Payments

Once funds are available, the wallet processes payments across supported platforms. You can use it at checkout pages, merchant apps, ticketing windows or quick scan based payments. The wallet balance reduces by the exact amount you pay and the rest stays available for later use. This setup keeps transactions predictable and clear.

Integration With UPI and Mobile Apps

Several systems now connect wallet balances with faster payment tools. These connections help users pay through familiar touch points without shifting between apps. A prepaid digital wallet solution may also support features like instant balance updates or protected utility bill payments. These additions give the wallet a smooth feel and allow new services to tie into the stored balance.

Read More: Top UPI Apps in IndiaKey Features of Prepaid Wallets

A prepaid wallet offers a set of features that make daily payments simple and predictable. Each feature supports a clear purpose, whether it is convenience, safety, or controlled spending. The design stays user-friendly so people can move through transactions without friction.

Spending Control and Set Limits

A prepaid setup helps people manage their spending with ease. You load a fixed amount, and the wallet draws only from that balance. This helps users maintain clarity over their expenses. Parents use this structure for controlled spending. Businesses use it for employee payouts where each wallet reflects a defined budget.

Security Layers

Digital payments need strong protection, and prepaid systems add multiple security checks by design. A mix of device-level checks, passcodes, and identity verification keeps each payment safe. The wallet blocks unauthorised access and ensures that every transaction flows through a secure path. These measures help users trust the balance they load.

Instant Payments and Smooth Usage

A prepaid wallet moves funds quickly because the payment flows from the stored balance. This makes small transactions faster. People feel the difference in recharges, retail payments, and quick transport-related payments. The system updates the balance right after each transaction, which keeps everything transparent.

Business Features in Prepaid Card Wallets

A prepaid card wallet offers extra features that suit workplace needs. Companies use it to give spending access to teams without linking to core bank accounts. Each card carries a defined limit, and every transaction is visible in a central dashboard. This helps with tracking, accounting, and compliance. These features reduce manual work and keep records clean.

Prepaid Digital Wallet Solutions for Businesses

Businesses rely on structured payment systems that stay reliable and easy to manage. A prepaid digital wallet solution offers this kind of setup. It gives companies a controlled payment space for employees, vendors, or customers without exposing core bank accounts. The flow stays simple. Funds are loaded in advance, and the wallet uses that balance for approved transactions.

API Based Wallet Infrastructure

Many companies build their systems on wallet-based APIs. These tools help them create user wallets, manage balances, and run verification checks within their own platforms. The structure supports real-time updates, smooth onboarding, and a consistent payment path across large teams. This makes the wallet feel like a natural part of the business system.

Integrations With Expense, Payroll, Loyalty, and Transit Systems

A prepaid digital wallet solution can link with expense modules, reward programs, travel systems, and vendor payments. These connections help staff move through payments without shifting between multiple tools. They also help finance teams track usage in a single space. Every transaction leaves a trace, which makes reconciliation clearer.

Digital Onboarding and Automation Features

Modern wallet systems support guided onboarding, identity checks, and automated balance updates. These features reduce manual work and help teams manage high volumes of users with steady accuracy. Automated triggers can load balance, restrict misuse, and generate alerts when limits are reached.

Industry Use Cases

Different sectors use this structure based on their needs. Logistics firms manage driver payouts through controlled cards. Retail chains give staff fixed-value wallets for store-level expenses. Service platforms use the same format for customer credits and refunds. Each case shows how flexible a prepaid wallet can be when built into a business workflow.

RBI Guidelines for Prepaid Wallets

Regulations play a major role in shaping how a prepaid wallet works. The Reserve Bank sets clear rules to keep the system safe, transparent, and reliable for users. These guidelines define wallet types, verification norms, spending limits, and safeguards that protect every transaction.

Classification of PPIs

The framework divides wallets into categories based on how they function and the level of verification completed.

Small PPIThis wallet supports low value payments. It holds a limited balance and follows basic verification. It suits users who need a simple option for small, everyday transactions.

Full KYC PPIThis format allows a higher balance and a wider set of services. Once full verification is completed, the wallet supports transfers, larger spending and broader acceptance. It follows stronger security rules and carries higher trust.

Gift, Transit, and Other Restricted PPIsThese wallets carry a specific purpose. Gift cards have set loading limits. Transit formats, such as those used in ticketing or toll payments, hold value only for transport-related services. Each type follows its own restrictions.

KYC Rules

Verification determines how much the user can load and where the wallet can be used. Basic checks allow limited usage. Full verification unlocks higher limits and more features. The process uses accepted identity documents and must be completed within a defined timeline. This ensures that the wallet operates in a safe and accountable manner.

Load and Spending Limits

Every wallet category has clear limits. A small PPI carries a lower maximum balance and controlled spending options. A full KYC wallet supports a higher balance and smoother transfers. These limits protect users and keep the system compliant with payment regulations.

Interoperability Requirements

A fully verified wallet can work across supported payment networks. This includes the ability to link with wider merchant ecosystems and tools used for digital payments. It helps users shift between services without complexity and brings prepaid formats closer to mainstream digital payment flows.

Restrictions Under RBI

A closed-loop prepaid wallet cannot be loaded from credit lines. The issuer must maintain clear transaction records and follow all risk control standards. The wallet issuer must track suspicious activity, protect users from misuse, and follow reporting requirements. These steps maintain trust across the entire system.

Security and Authentication Rules

Every transaction follows strict security checks. Device binding, identity checks, and added authentication layers keep the balance safe. These steps guard against fraud and help users feel confident when they add money or make a payment.

Prepaid Wallet License in India

Building or issuing a prepaid wallet requires formal approval. The license process ensures that only qualified companies operate these systems. This protects users and keeps the payment environment safe. The Reserve Bank sets the standards and reviews each application with strict checks.

Who Needs a License

Companies that want to issue or manage regulated prepaid payment instruments (PPIs) that work with third-party merchants or allow transfers must apply for a prepaid wallet (PPI) license from the RBI. This includes fintech platforms, digital service providers, and businesses that plan to offer wallet-based payments as part of their product flow. The license confirms that the issuer can meet the operational and security expectations required for such systems.

Eligibility and Net Worth Requirements

The applicant must meet the minimum capital and net worth criteria defined by the Reserve Bank. These financial requirements help confirm that the company can maintain a stable and well-managed wallet system. It also shows that the issuer can support customer balances without risk.

Compliance, Reporting, and Operational Standards

Licensed issuers follow continual reporting rules. They must maintain transaction logs, safeguard user data and put strong risk controls in place. The system must support monitoring tools that track suspicious activity. These standards keep the wallet safe and ensure that each payment flows through a secure channel.

Technology, Security, and Governance Expectations

A wallet issuer needs reliable systems, protected servers, and strict access controls. Identity checks, data encryption, and regular audits keep the structure sound. A strong operational plan and a clear governance framework are essential parts of the license criteria. The issuer must show that they can keep the wallet running smoothly at scale.

RBI Approval Workflow

The license process follows a set path. The company submits its application, provides the required documents, and completes all technical checks. The Reserve Bank reviews the proposal, evaluates the systems, and assesses risk controls. After successful verification and testing, the approval is granted.

Advantages of Using Prepaid Wallets

A prepaid wallet offers an easy way to manage payments with clarity and control. People choose this format because it fits easily into daily life and gives them a steady hold over how money moves. The benefits apply to individuals as well as businesses, though each group uses the wallet for different reasons.

Benefits for Individuals

Users get a clean and straightforward payment method. The wallet holds a fixed balance, which helps them keep track of daily spending without thinking about multiple bank transactions. It works well for quick payments such as recharges, small purchases, transport related fees or online services. The setup reduces clutter and keeps the experience smooth.

Benefits for Businesses

Companies use prepaid formats for better control over outgoing payments. This structure helps them distribute funds to teams, vendors, or service partners without exposing core accounts. A prepaid card wallet supports expense caps, category-based usage, and detailed reports. These tools reduce the effort needed for reconciliation and bring discipline to routine spending.

Compliance Advantages for Enterprises

Enterprises must follow strict compliance rules when managing payments at scale. A regulated wallet system helps them meet these requirements. The structure supports clear logs, identity checks, and verified workflows that align with payment standards. This creates a safer operating space and helps teams maintain accountability.

Conclusion

A prepaid wallet has become a steady part of digital payments because it keeps transactions simple and predictable. Users add money once and pay across supported services without friction. The same structure helps businesses manage controlled payouts through reliable prepaid digital wallet solutions. RBI rules guide verification, limits, and security, which keep every wallet accountable and safe to use. These safeguards give people confidence and help companies build services around stored value. As digital platforms grow, the wallet model will continue to support quick payments, transport systems, rewards, and many everyday tasks with a clean and practical flow.

FAQs

1. How does a prepaid wallet differ from a standard mobile banking app?A prepaid wallet holds a stored balance that you load before spending, while a mobile banking app pulls money directly from your bank account. The wallet limits spending to the amount you add, which helps with controlled usage. Banking apps allow full access to account funds, but prepaid setups offer more predictable and restricted payment flows.

2. Can a prepaid wallet be used without completing full KYC verification?A user can start with basic verification, but the wallet will offer only limited features until full KYC is completed. Basic KYC allows small payments and a capped balance. Completing full KYC unlocks higher limits, broader usage and smoother transfers. This staged structure helps new users get started while keeping the system safe and regulated.

3. What happens if a prepaid wallet balance becomes inactive for a long time?Prepaid wallets follow specific rules for inactivity under the issuer’s policy and RBI guidelines. If the balance remains untouched for a set period, the issuer may restrict usage until the user verifies identity or updates account information. Funds do not disappear. They remain protected and can be accessed again once the required steps are completed. This process prevents misuse and keeps records accurate.

4. How safe is my personal information when I use a prepaid wallet?Personal data stays protected through secure servers, strict access controls, and verified identity checks. Issuers must follow strong data protection standards, including encrypted storage and controlled internal access. Regular audits and monitoring add another layer of safety. These measures prevent unauthorised access and help maintain trust in the prepaid system.

5. Can I link a prepaid wallet to recurring payments or subscriptions?Some prepaid systems support recurring payments, provided the balance covers the required amount. The wallet must maintain sufficient funds; otherwise, the payment will fail. This arrangement helps users manage controlled subscriptions where they prefer using fixed value balances instead of exposing full account access. Policies vary by issuer based on system design.

6. How does a prepaid wallet help with budgeting and personal finance?A prepaid wallet gives a clear spending boundary because you load only the amount you plan to use. Every transaction deducts from this stored balance, which makes it easier to track and limit daily expenses. This controlled system helps people avoid overspending and builds a steady habit of monitoring financial activity with minimal effort.

7. Can businesses customise prepaid wallets for employees or customers?Companies can customise features such as spending categories, daily limits, usage controls, and automated top-ups. This helps them manage travel expenses, staff allowances, refunds, or rewards from a single dashboard. The wallet structure keeps company spending separate from core bank accounts and supports detailed reports that make reconciliation easier for finance teams.

8. Do prepaid wallets work when a user travels outside their home state or region?Most prepaid systems work across regions without extra steps, as long as the merchant or service supports digital payments. Cross-region usage does not affect the stored balance. The wallet continues to process payments normally. Some travel-related services like transport or toll systems may have region-specific rules, but regular merchant payments remain unaffected.

9. What should I do if a payment fails but the amount gets deducted from my prepaid wallet?In the rare case of a failed transaction with a deduction, the issuer usually reverses the balance automatically after internal checks. Users can raise a ticket within the app to speed up the review. The wallet system keeps clear payment records, so tracing a failed transaction is straightforward, and the refunded amount is reflected once resolved.

10. Can a prepaid wallet support both personal and business use on the same account?Most issuers separate personal and business features to maintain clear records and avoid compliance issues. Personal wallets focus on everyday spending. Business wallets support controlled payouts, employee cards, or vendor payments. A user may hold both, but they are usually managed as separate profiles. This helps maintain accurate accounting and cleaner financial tracking.