Digital Wallets in India – Meaning, Growth, and Everyday Relevance

Digital payments have moved into daily life with surprising speed. Recent RBI and industry reports show that digital payments now account for a very high share of transaction volumes in India, reflecting how comfortable people have become with quick, screen-led payments. Another study reported more than 880 million internet users across the country. That scale creates room for tools that simplify money transfer, and a digital wallet fits directly into that space.

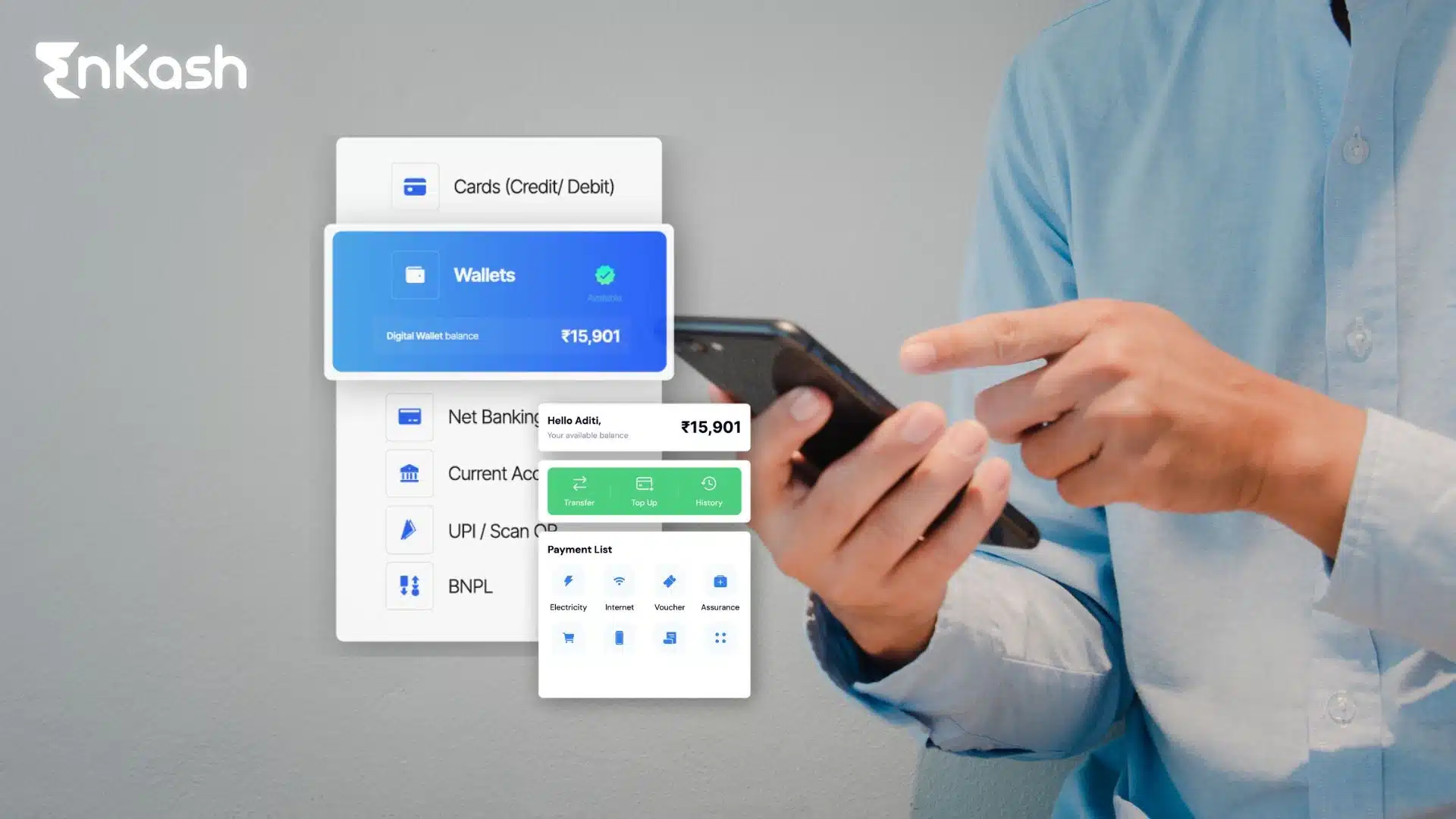

People usually understand the meaning of a digital wallet once they use it for something small, like paying a utility bill or booking a short ride. The app holds stored value or linked payment details, and the moment a user confirms a payment, the wallet handles the rest. It feels straightforward, which is why many first-time users search for what a wallet is before trying it. The experience then explains itself. A wallet behaves like a digital pouch that manages balance, rewards, past transactions, and quick payment paths.

Someone who wants to define an e-wallet might describe it as a secure digital space that holds prepaid funds or receives money from a linked account. It helps people move through checkout stages with fewer steps. The wallet account’s meaning becomes clearer when the user sees their profile, saved balance, and spending history arranged in one place.

Growth in e-commerce has made digital wallets familiar across cities, small towns, and even remote areas. People use it for groceries, mobile top-ups, short trips, and unexpected little purchases that appear during the day. These touchpoints help users recognise e-wallet examples without needing guidance. The presence of reliable digital wallet platforms turns simple payments into a habit, and that habit drives the steady rise of digital transactions across India.

Integrate Co-Branded Digital WalletHow Digital Wallets Work: Technology, Flow, and Security

Core Wallet Technology Explained

A digital wallet relies on secure layers that shape every action from the first tap to the last confirmation. Encryption protects stored information, and that protection stays in place whether the wallet keeps value on the device or through a controlled cloud setup. The system checks the user through simple prompts before it prepares a token for the transaction. This token replaces sensitive details and limits exposure during payment. People sense the stability even though the steps stay hidden. The structure reflects how modern payment systems maintain trust in high-volume environments.

What Happens During a Wallet Payment

A user initiates payment through a scan or a direct selection. A digital wallet prepares the request and moves it to the payment partner for validation. The partner reads the token, checks the available balance or linked source, and sends the instruction to the issuer or stored value system. Once verified, the merchant receives confirmation. A small transaction helps many users understand what a wallet payment is, since the movement feels natural. The payment clears quickly, yet behind it sits a sequence shaped by regulated processes and real-time checks.

Wallet Services Behind Daily Convenience

The range of actions inside a wallet keeps daily transactions organised. People load value, clear bills, recharge services, and monitor spending without switching between platforms. These features help the digital wallet feel familiar in routine moments. For many users, wallet technology supports predictable payments, while wallet services help reduce manual steps in situations that repeat throughout the week. These functions show why a digital wallet remains relevant in a country that values reliable and controlled payment flows.

Types of Digital Wallets in India

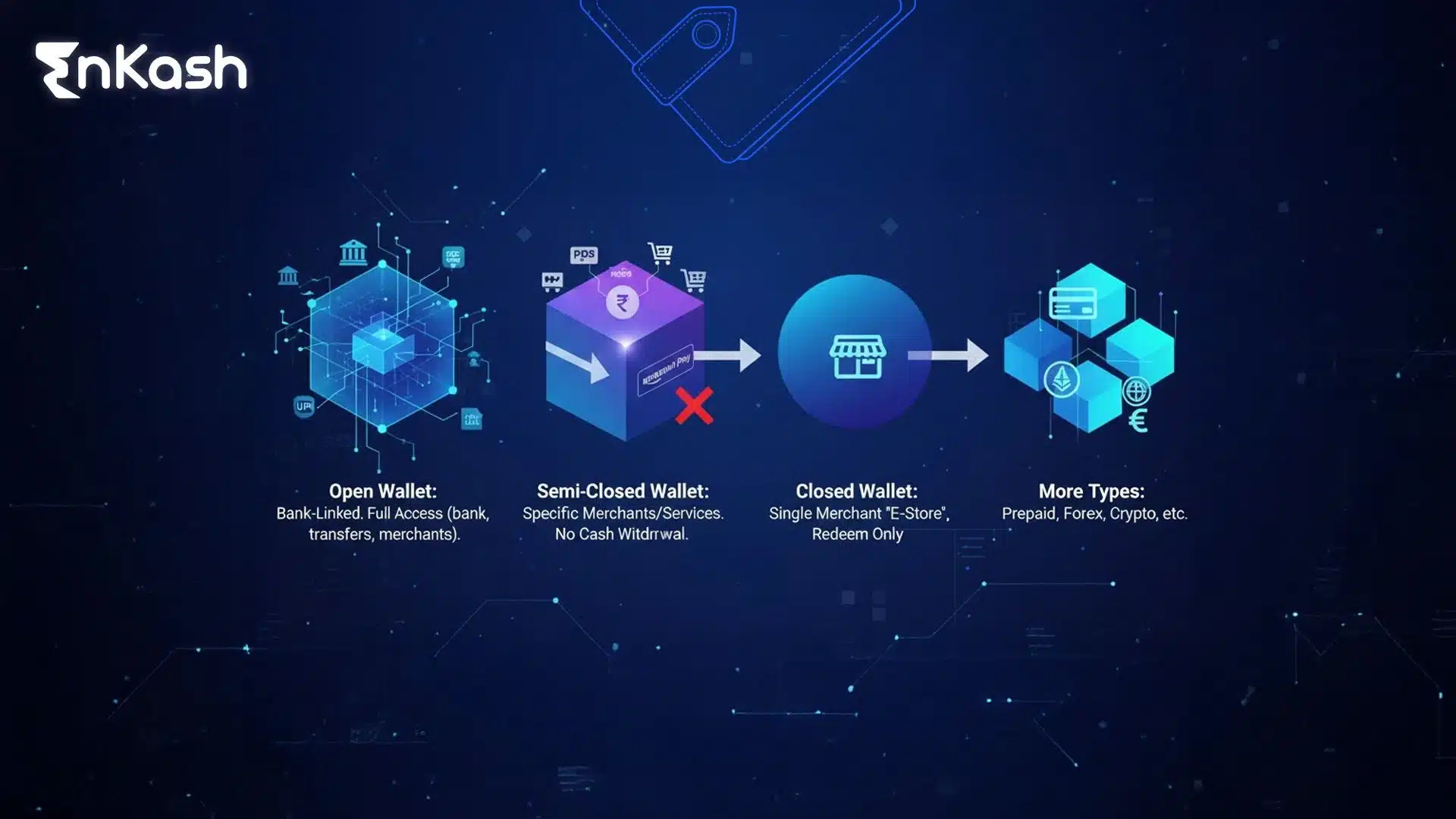

Closed Wallets

Closed wallets sit inside a single platform and feel familiar to anyone who revisits the same service during the week. Stored value stays within that environment, which gives users quick access during refunds, repeat orders, or reward adjustments. A digital wallet in this format behaves like a contained pocket of money. People rely on it because the movement of value stays predictable, and the wallet keeps every transaction tied to a clear purpose.

Semi Closed Wallets

Semi-closed wallets stretch a little wider. They support payments across authorised merchant networks that follow the required guidelines. Users load balance and spend it across shopping, travel, food delivery, and routine bill payments without shifting to a separate interface. These experiences help many identify e-wallet examples they already use without thinking about the category. The wallet clears payments with minimal friction, and that simplicity encourages repeat use.

Open Wallets

Open wallets carry a wider range. They support merchant payments but also allow transfers to bank accounts and cash withdrawals where permitted. This structure feels practical for users who manage varied spending in a single day. People exploring the wallet account meaning often understand it clearly once they see how the profile handles stored balance, transfers, and spending history. The design blends control with flexibility, and that mix appeals to many who want a wider financial tool.

Read more: Types of wallets

Device-Based Mobile Wallets

Device-based mobile wallets live directly on the phone. They store payment details securely and complete transactions through a simple tap or scan. The idea becomes clear once a user sees how the device confirms a payment without asking for repeated steps. It feels natural during short, time-sensitive moments such as quick store checkouts, metro entries, or any place where a fast and controlled payment makes the experience smoother.

Crypto and Blockchain Wallets

Crypto wallets handle digital assets and operate under frameworks that differ from regular payment tools. They store ownership keys and process value through blockchain ledgers. These wallets sit outside traditional digital wallet platforms, yet they help users understand how value can move inside systems built for transparency and controlled access. Their presence widens the idea of what a digital wallet can store, even if adoption remains limited within India.

Digital Wallet Examples Across Modern Payment Journeys

Digital payments have become a routine part of retail in India. People use wallets to clear grocery bills, settle food orders, or complete a purchase during a late evening scroll through an online marketplace. These payment flows rely on stored balance or linked sources, and the wallet moves the transaction forward without slowing the checkout. Users recognise many e-wallet examples in daily shopping because the experience feels direct. The wallet presents a clear amount, confirms the payment, and updates the balance in seconds.

Travel and Mobility Wallets

Travel payments have shifted toward simple digital flows. Users pay for cabs, auto rides, metro trips, or fuel stops through wallets that support small, time-bound transactions. The wallet handles these quick movements with accuracy, which helps people trust the method. Frequent travellers appreciate how the payment completes without interrupting their journey. It also helps that mobility platforms treat wallet payments as a reliable way to maintain consistency during high-volume hours.

Bill Payments and Financial Services Wallets

Routine bills create a predictable pattern across households. People use wallets to clear electricity bills, water charges, mobile recharges, and broadband payments. These actions reduce the need to remember multiple portals. The wallet brings everything into one view and completes the payment through a controlled flow. Users see the convenience and keep returning to it. Small financial services, like micro-recharges or short-duration plans, also align well with this structure.

Role of Digital Wallet in E-commerce

E-commerce benefits from wallet-driven checkouts because the process reduces steps. A digital wallet helps eliminate repeated entry of payment details, which lowers friction during busy sales periods or urgent orders. Refunds also move faster, since the value settles directly into the wallet balance. Many customers treat this as a safer way to manage returns. The presence of stable digital wallet platforms supports the wider shopping ecosystem by creating a consistent payment path.

Role of Digital Wallets in E Commerce

Smoother Checkout Through Wallet Technology

A digital wallet reduces friction across e-commerce journeys by removing long inputs and repeated confirmations. Wallet technology holds verified credentials, so the customer moves from cart to payment with fewer steps. This shorter flow keeps the user engaged during busy sale hours or fast-moving product drops. Merchants see clearer conversions when customers experience a direct, stable payment path.

Reliable Refunds and Simple Return Cycles

A wallet-driven refund settles value into the balance without delay, which helps customers track their money after a cancellation. This works well for e-wallets in e-commerce because returns tend to rise during seasonal sales. The wallet shows the credited amount instantly and keeps the payment trail clean. This clarity reduces follow-up issues and strengthens the customer’s trust in the platform.

Wallet Services That Support Loyalty and Rewards

Many platforms use wallet services to distribute credits, cashback amounts, or small-value rewards. These amounts settle within the wallet and appear automatically during the next payment. Users apply them without searching for codes or switching between screens. This encourages repeat purchases, and the process feels easy because the wallet manages the reward logic in the background.

Fast Payments for High-Frequency E-Commerce Purchases

Short, recurring transactions create steady movement across online marketplaces. A digital wallet helps customers handle these small purchases without slowing down the flow. Stored value or linked payment credentials clear the transaction in seconds. This predictable rhythm supports use cases such as food orders, low-value add-ons, and daily essentials, where customers expect fast, controlled payments.

Benefits of Using a Digital Wallet

Strong Security for Everyday Payments

A digital wallet protects sensitive information through encrypted storage and controlled access. Users confirm each action through simple device prompts, and the wallet replaces real payment details with secure tokens during transactions. This structure shields financial data from exposure. People feel safer using a wallet for recurring payments because the system keeps each transaction contained within a protected flow.

Faster Payments With Minimal Effort

Speed shapes many digital journeys, and a wallet helps users complete payments without long steps. Stored balance or verified credentials allow people to move through checkout in seconds. This rhythm benefits small, time-bound transactions where the user expects a quick response. The wallet maintains this pace across bill payments, food orders, recharges, and short travel expenses.

Clear Visibility and Better Spend Control

A wallet provides a single view of outgoing payments, rewards, and stored balance. Users revisit this section to track spending and manage routine costs. The structure brings clarity to small expenses that tend to get lost across multiple apps. People find this helpful when they want to create a simple pattern for digital spending without switching between tools.

Stable Experience for Low-Value Transactions

Low-value transactions appear throughout the day. A digital wallet handles these payments without slowing the user down or interrupting their task. The wallet completes the request with predictable timing, which makes it suitable for small purchases that demand speed and accuracy. Many users rely on this flow during high movement hours, where even a short delay can disrupt the experience.

Limitations and Risks of Digital Wallets

KYC Requirements and Balance Restrictions

A digital wallet operates within regulated guidelines, and these rules shape how much value a user can store or transfer. KYC checks are required for higher limits, and some users may find this step inconvenient when they want immediate access to full features. The structure protects the ecosystem, but it can create delays for people who prefer instant activation.

Issues Linked to Device Loss or Access Problems

A wallet depends on the device that holds it. If the phone is misplaced or damaged, the user must recover access through verification steps. These steps protect the account, yet the temporary pause can disrupt payments. People who rely heavily on wallet technology feel the interruption more clearly during busy hours or urgent transactions.

Merchant Acceptance Gaps Across Certain Use Cases

Digital payments continue to expand, but reliable acceptance still varies across smaller merchants and remote service points. Some businesses support direct wallet payments, while others focus on different digital methods. This inconsistency limits how people use wallet services during unplanned purchases or sudden expenses.

Restrictions on Higher Value Payments

Wallets excel in fast, low-value transactions. High-value payments create a different challenge. Regulatory caps and platform limits restrict how much a user can transfer or store at once. People handling large purchases must switch to other payment modes. The shift breaks the flow for those who prefer a unified digital method.

Setting Up a Digital Wallet in India

Creating an Account and Completing KYC

Setting up a digital wallet begins with a simple account creation flow. The user installs the wallet app, enters basic details, and verifies their identity through a secure prompt. To unlock higher limits, the customer completes KYC through a supported method. This step confirms identity and enables a wider range of transactions. People see the benefit once they start handling frequent payments, since a verified profile keeps the wallet stable across varied use cases.

Adding Payment Methods and Loading Value

A wallet functions smoothly when the user links a payment source or loads stored value. The process feels straightforward. The user selects the preferred method, confirms identity, and the wallet assigns the source to the profile. From this point, the user can load value, clear bills, or make quick purchases. The experience shows why many rely on wallet services during busy periods when manual entry slows the flow.

Setting Controls, Alerts, and Spending Limits

People use limits to keep spending structured. A wallet offers controls that help users set safe ranges for daily or monthly payments. Notification alerts also help track unusual activity. This mix of control and visibility appeals to those who want active oversight without checking multiple tools. It also highlights how wallet technology brings transparency into the payment journey.

Using Wallet Services Safely Across Daily Transactions

A wallet stays secure when the user follows simple habits. Keeping the device locked, avoiding unverified links, and confirming payment details before approving the transaction helps maintain safety. People also revisit their wallet history to ensure every payment aligns with their spending patterns. These actions support the digital wallet as a reliable partner for daily transactions where accuracy and speed matter.

Growth Driven by Policy and Digital Adoption

Digital payments continue to expand as more users gain access to reliable internet and secure mobile devices. A digital wallet benefits from this shift because people now expect quick, predictable payment flows. Policy frameworks also support this growth by encouraging safe digital transactions. These factors combine to create an environment where wallets move closer to the centre of everyday financial activity.

E-Commerce Expansion Strengthening Wallet Adoption

E-commerce platforms rely on fast payment cycles, and wallets support that expectation. People use stored value for small purchases, returns, and urgent orders that demand instant confirmation. As marketplaces grow, customers seek a consistent checkout experience. This drives interest in wallet-based payments and strengthens the position of digital wallet Platforms within the wider shopping ecosystem.

Evolving Wallet Technology and Smarter Features

The next phase of growth involves deeper integration of wallet technology. Smarter authentication methods, improved fraud monitoring, and contextual prompts are becoming common. These features refine how a wallet responds during high movement hours or large transaction spikes. People appreciate the controlled environment, and businesses value the stability it brings to their payment systems.

Users want a single space where they can track expenses, manage stored value, and complete payments without switching apps. Wallets meet this need through wallet services that organise transfers, recharges, rewards, and small recurring payments. As these features expand, wallets are likely to serve as unified spending tools that support both daily transactions and structured financial habits.

Summary

A digital wallet has become a trusted way to manage quick, structured payments. Users depend on it for small purchases, refunds, bill payments, and e-commerce checkouts because the wallet keeps each transaction organised and easy to follow. It also helps people monitor spending, maintain balance, and complete payments without unnecessary steps. As more users turn toward digital methods, wallets continue to shape how daily financial activity flows. Their simplicity, combined with secure design, makes them a steady part of routine transactions. This shift shows how digital payments are becoming a familiar and reliable part of everyday life.

FAQs

1. How secure is a digital wallet for everyday transactions?A digital wallet protects payment information through encrypted storage and controlled access. It replaces sensitive details with single-use tokens, which keep real data hidden during payments. This design helps users complete everyday transactions with confidence, even when they make frequent or small purchases across different services.

2. Can a digital wallet help someone new to digital payments?Yes. A digital wallet presents balance, history, and quick actions in a simple layout that feels easy to follow. New users appreciate how the app handles most steps automatically. It reduces errors, removes long forms, and creates a clear path for anyone learning digital payments.

3. Why is a digital wallet suitable for small, frequent purchases?Small purchases require speed, and a digital wallet delivers that by removing repeated inputs. The app uses stored value or verified details to complete payments instantly. This supports groceries, local travel, small orders, and other daily needs that appear throughout the day and demand a fast response.

4. Does a digital wallet work for people with limited banking access?It can. A digital wallet allows users to load value and spend it without constant interaction with a bank. This setup supports individuals who want a simple digital method but face difficulties with traditional banking tools or long authentication steps.

5. How does a digital wallet perform during high-traffic sale periods?A digital wallet shortens checkout time because the user avoids manual entry. During busy sale hours, this speed helps secure limited-stock items before they expire. The wallet processes payments through a stable flow that holds up even when the platform experiences heavy activity.

6. What happens when a refund goes back to a digital wallet?A refund settles into the wallet balance almost immediately, which gives users a clear view of the credited amount. This avoids long settlement delays and helps people manage replacements or follow-up purchases without waiting for the money to return through slower channels.

7. What does a digital wallet account include?A digital wallet account includes the user’s profile, balance, spending history, and reward information. It creates a central place where the user can track transactions and make payments without switching between multiple apps. This sense of structure makes the wallet practical for daily use.

8. Can a digital wallet support travel-related payments?Yes. A digital wallet works well for quick travel payments such as metro entries, cab bookings, or fuel stops. It processes these transactions instantly, which helps people move through checkpoints or complete bookings without breaking their travel rhythm or searching for cash.

9. Can a digital wallet improve personal budgeting?A digital wallet displays recent transactions in a compact, easy-to-read format. Users revisit this view to understand how they spend throughout the week. This simple tracking approach helps people stay aware of small expenses that usually slip past traditional budgeting tools.

10. How does a digital wallet simplify returns and replacements in online shopping?A digital wallet speeds up the return cycle because refunds appear in the balance without long delays. The user can track the amount and use it immediately for another purchase. This clear, quick cycle reduces confusion and makes the return process less stressful.