A closed wallet is a type of digital wallet where the stored value can be used only within the same business that issued it. This model is common across India’s online shopping, travel booking, food delivery, subscription apps, and gaming platforms. Since the value never leaves the company’s ecosystem, the setup is simple, secure, and tightly managed. This is why many users search for what a closed wallet is when trying to understand how store credits or instant refunds work.

In everyday situations, a closed-loop wallet makes the refund experience faster. When you cancel an order on an e-commerce or travel app in India, the money usually goes into your closed e-wallet instead of returning to your bank. The next time you buy something, the system automatically adjusts the balance. This keeps transactions quick and avoids the delays that occur in bank-led refund cycles.

For businesses, the closed-loop wallet in India supports smooth refund management, lower payment gateway dependency, and better control over internal credits. Since all activity stays inside one network, the platform can track refunds, purchases, and wallet movements without involving external systems.

Under the closed wallet RBI guidelines, this model does not require a closed wallet license because the value cannot be transferred, withdrawn, or used with other merchants. It remains outside the regulatory scope applied to semi-closed wallets or open wallets versus closed wallet setups, which have broader usage and stricter compliance requirements.

A closed wallet example can be seen when a cancelled flight ticket is refunded as travel credits or when returned products on a shopping app are added to a user’s wallet for future purchases. Each closed e-wallet example stays confined to the issuing brand’s platform, making the process predictable and fully controlled.

How a Closed Wallet Works in India?

A closed wallet works inside a single company’s system. The value stored in it can be refunds, store credits, loyalty points, or in-app balances. Since the money stays within the platform, the flow is faster and more predictable than external payment methods.

When a user adds money or receives a refund, the amount sits in the platform’s internal ledger. Payments made through the closed e-wallet are settled instantly because there is no involvement of banks or outside gateways. This structure gives the model the name closed-loop wallet.

In India, the working model is easy to understand. Cancel a meal order on a food delivery app or a bus ticket on a travel platform, and the refund appears immediately in the wallet. The next time you place an order, the app deducts the balance automatically. A closed wallet example also includes in-app gaming credits that can be used only within the same game or platform.

This system is different from a semi-closed wallet or a semi-closed loop wallet, which allows spending across multiple approved merchants. A closed model stays locked to a single brand and does not require the compliance measures that apply to the semi-closed format.

Because everything happens inside one controlled space, the experience is smooth for users and operationally efficient for businesses. The internal syncing keeps transactions consistent, secure, and easy to track.

Internal Structure and Security of a Closed Loop Wallet

Internal Setup and Working Model

A closed-loop wallet operates inside a single digital space. It connects the user, the merchant, and the system managed by the issuing company. Every transaction stays within this setup. Because it does not link to other merchants or banks, the process stays secure and easy to control.

When money is added to a closed e-wallet, it sits in a digital ledger that belongs to the same company. Each time a purchase happens, the wallet balance adjusts automatically. Refunds or returns are credited back to this wallet instead of going to a bank account. The record updates instantly, keeping everything transparent for both users and the business.

Security and Data Flow

Behind the scenes, each payment passes through a verification layer. The system checks transaction details before confirming them. This reduces errors and prevents misuse. A closed wallet does not require RBI authorization because it is excluded from the definition of Prepaid Payment Instruments. These steps help protect customer data and maintain transaction history.

Why Do Businesses Use Closed Wallets in India?

Faster Refund Processing

A closed wallet helps Indian businesses issue refunds instantly. When a user cancels an order or booking, the amount moves directly into the closed e-wallet instead of going through bank settlement cycles. Since everything stays inside the same digital network, delays drop sharply and customers receive their balance within seconds.

Lower Dependency on External Gateways

Using a closed-loop wallet reduces the need for multiple payment gateways. Companies can manage credits, returns, and in-app purchases internally, which lowers transaction costs and cuts down on technical failures. This is especially useful for platforms that handle high-frequency purchases like e-commerce, travel, and food delivery.

Better Control Over Transactions

A business gains complete visibility over how wallet balances are added, used, or refunded. All transactions inside the digital wallet follow predictable rules, making compliance and record-keeping easier. Since the model falls under closed wallet RBI guidelines, companies do not require a closed wallet license, provided the balance is used only for their own products or services.

Improved User Experience

Users benefit from quicker payments and easier access to refunds. Instead of entering payment details repeatedly, they can simply use the stored balance in the closed-loop wallet in India. This reduces friction and encourages repeat transactions, which is valuable for platforms relying on frequent user engagement.

Supports Loyalty and Credit-Based Transactions

Many Indian platforms use closed wallets to run loyalty programs, reward systems, or store credits. Because the wallet is locked to the brand, points and credits remain organised in one place. This system strengthens customer retention and keeps spending within the same ecosystem.

RBI Guidelines on Closed Wallets Explained

Position of Closed Wallets Under the PPI Framework

The Reserve Bank of India oversees all forms of digital payments through its Prepaid Payment Instruments framework. A closed wallet works differently from other wallet types because the stored value can be used only within the same business that issued it. Since the money cannot be transferred, withdrawn, or spent outside the platform, the setup remains outside the direct licensing requirements applied to semi closed or open wallets. This exemption is defined under the closed wallet RBI guidelines, which treat the model as low risk within the broader payment system.

Why Closed Wallets Do Not Need RBI Authorization

A business using a closed loop wallet does not require a closed wallet license as long as the balance stays confined to its own products or services. Refunds, credits, reward points, or in-app balances can move freely inside the platform without any approval from the regulator. The moment the value is allowed to reach other merchants, the wallet shifts into the semi closed wallet category, which requires a semi closed wallet license and additional compliance under RBI rules.

Responsibilities for Businesses Issuing Closed Wallets

Even with the exemption, companies must follow fair and transparent practices. They must clearly communicate refund rules, wallet validity, and how credits are managed. Accurate record keeping is essential because all wallet movements are stored in an internal ledger. Security measures should protect user data at every step, ensuring that the digital wallet functions smoothly within India’s regulatory environment.

Boundaries Between Closed and Semi-Closed Wallet Models

A closed wallet becomes a semi-closed loop wallet when users are allowed to spend the balance at external merchants. RBI monitors this transition closely. Businesses must report operational changes and seek approval before expanding usage. Defining these boundaries correctly prevents compliance issues and ensures that the platform remains aligned with semi-closed wallet RBI expectations.

Closed Wallet Exemption and Regulatory Classification

When Does a Closed Wallet Need Authorization

A closed wallet is the simplest form of stored-value account, but it still works under a clear set of financial boundaries. The Reserve Bank of India does not require a special license for companies that issue this kind of wallet, as long as the stored money is used only for buying products or services from the same company. The value cannot be transferred to another merchant or withdrawn as cash. Spending outside the platform turns it into a semi-closed wallet, which needs prior approval under the Prepaid Payment Instruments guidelines.

Every company planning to issue a closed wallet must assess its model carefully before launch. If the goal is to handle refunds or store credits internally, no extra permission is needed. However, once the platform grows and connects with external partners, the business must apply for a semi-closed wallet license to stay compliant.

Business Models That Qualify as Closed Wallets

Several use cases fit under the closed wallet license exemption. Retail brands use it to issue store credits for returns or cancellations. Travel and ticketing platforms use similar wallets for refund balances that can be used later for new bookings. Gaming and entertainment platforms maintain wallets for reward points or credits that work only inside their systems. Corporate service providers may use closed wallets for issuing credits for internal services, but not for payouts to employees or vendors.

All these examples follow one rule. The wallet must serve transactions linked directly to the issuing business. If the balance can be spent outside the brand ecosystem, it shifts into a semi-closed wallet category.

Compliance Risks if Misclassified

Companies that use wallet systems without understanding these boundaries face compliance challenges. Misclassifying a semi closed model as a closed wallet can lead to violations under the Payment and Settlement Systems Act. It can also result in penalties or restrictions on further operations.

To stay compliant, businesses must report wallet usage transparently, maintain updated policy documents, and include clear terms for users. Regular audits and internal checks help prevent errors and maintain alignment with the RBI guidelines.

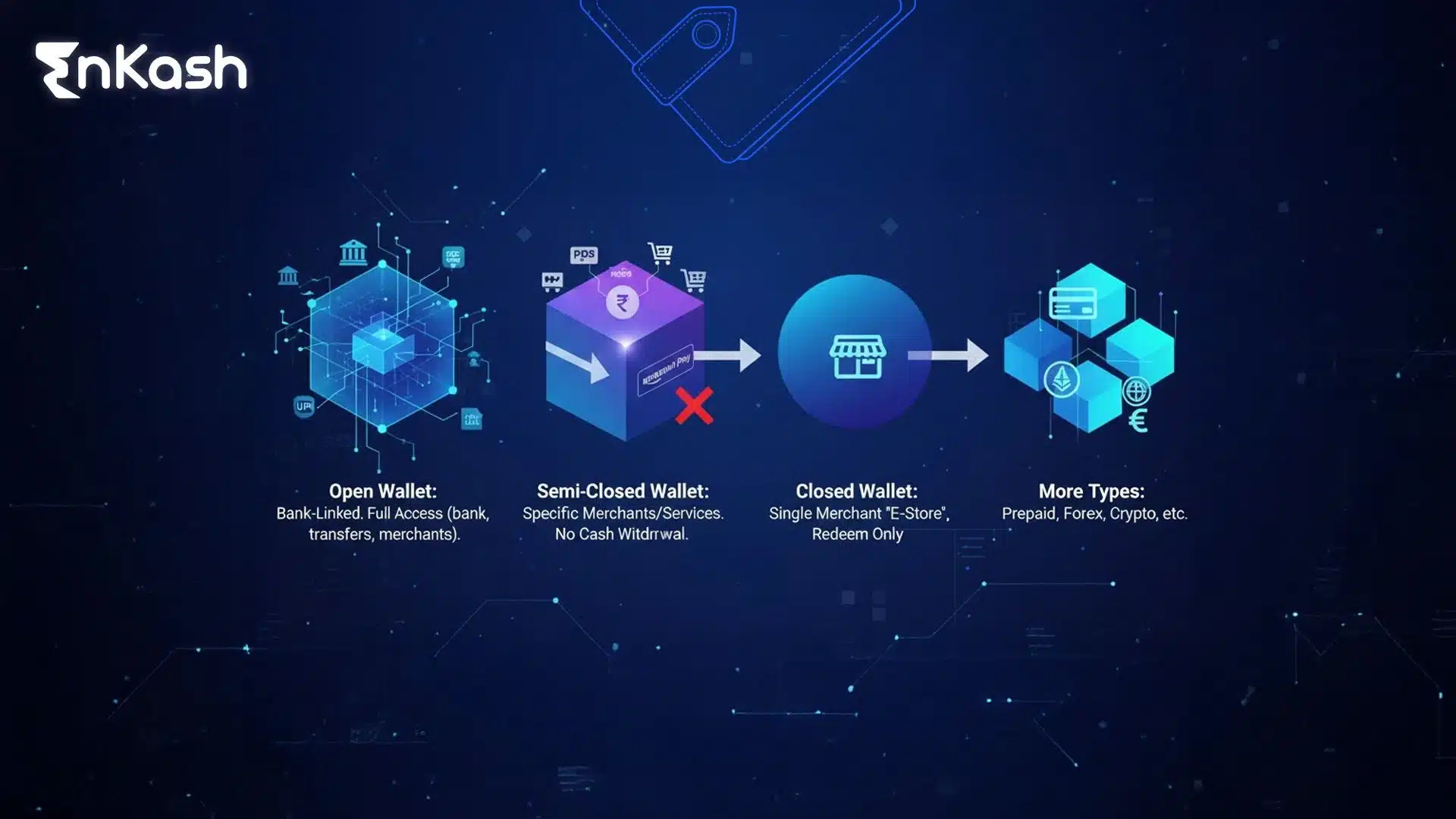

Comparison – Open Wallet vs Closed Wallet vs Semi Closed Wallet

Digital wallets do not work the same way. Each type serves a different purpose within the payment structure. Some are limited to a single company, others work across selected merchants, and a few allow full-scale transfers and withdrawals.

Before exploring how they are used, it helps to see their features side by side. The table below shows how a closed wallet, a semi-closed wallet, and an open wallet differ in usage, regulation, and flexibility.

| Feature | Closed Wallet | Semi Closed Wallet | Open Wallet |

| Authorization Required | No | Yes | Yes |

| Usage Scope | Single merchant or brand only | Multiple approved merchants | Universal usage across merchants and banks |

| Fund Transfer to Others | Not allowed | Allowed within the approved merchant network | Fully allowed, including peer-to-peer transfers |

| Cash Withdrawal | Not permitted | Not permitted | Permitted |

| Refund Handling | Stored as wallet credit | Stored as a wallet balance | Refunded to the wallet or bank |

| Example | Retail brand credit, travel refund wallet | Fintech wallet for merchant payments | Bank-issued digital wallet or payment card |

| Best For | Brand-specific transactions | Multi-merchant digital payments | Complete digital and cash-based transactions |

| Regulatory Status (RBI) | Exempt from PPI authorization | Requires a PPI license | Requires full authorization and bank partnership |

Benefits and Challenges of Closed Wallet Systems

Key Benefits

- A closed wallet creates value for both users and businesses by making digital transactions faster, safer, and more controlled.

- A closed wallet keeps all transactions within the company’s own system, reducing third-party dependency.

- Refunds are processed instantly, allowing users to reuse the amount for their next purchase.

- Businesses save on external payment gateway fees and improve operational control.

- The wallet helps companies maintain customer loyalty by encouraging repeat spending.

- It simplifies transaction tracking for users as they can view all their credits in one dashboard.

- Users enjoy a safer experience since no banking or card details are shared for each purchase.

Main Challenges

- Despite its simplicity, the closed wallet model has certain limits that affect flexibility and long-term usability.

- The stored balance can be used only within the issuing company’s platform.

- Funds cannot be transferred to other users or withdrawn as cash.

- If a company discontinues its service, wallet balances may be delayed or difficult to recover.

- Limited flexibility restricts users who prefer broader payment options.

- Businesses must manage refunds and record-keeping carefully to stay transparent and compliant.

- The closed wallet model depends heavily on user trust and consistent service quality.

The Future of Closed Wallets in India’s Digital Payment Ecosystem

Movement Toward Hybrid Wallet Models

The rise of digital payments in India is pushing many companies to blend the structure of a closed-loop wallet with features that resemble a semi-closed format. These hybrid systems allow brands to manage refunds and store credits internally, while also giving users limited flexibility during checkout. Some platforms already allow customers to combine their wallet balance with another payment method in a single transaction. This setup maintains the speed and safety of a closed wallet while offering more convenience for users.

Role in an Interconnected Digital Landscape

As interoperable payment systems expand, digital platforms in India are exploring new ways to manage internal credits and micro transactions. A closed-loop wallet in India continues to serve a clear purpose by handling refunds, reward points, and brand-linked transactions that do not need external merchant acceptance. Since the value stays within a controlled digital space, the model supports fast settlement and stable transaction flow across apps that depend on repeated customer activity.

Anticipated Regulatory Evolution

The Reserve Bank of India is expected to refine rules around data protection, security standards, and record keeping. Although a closed wallet does not require a license, businesses will still need strong internal systems to maintain accuracy and safeguard user information. Any platform planning to expand into a semi closed model must follow the requirements linked to a Semi closed wallet license and align with semi closed wallet RBI guidelines.

More Indian companies are expected to use closed or hybrid wallets to reduce transaction costs and improve user retention. These models work well for sectors where refunds, credits, and loyalty points play an important role. As digital commerce grows, the closed wallet will continue to offer a dependable method for managing internal transactions and supporting brand-specific payment flows.

In Conclusion

A closed wallet plays a steady role in India’s digital payment setup by keeping transactions simple, secure, and tightly controlled. Since the value stays within the issuing company’s system, users receive instant refunds, smoother checkouts, and a predictable way to manage credits. Businesses benefit from lower payment gateway dependency, accurate record keeping, and better control over refunds and loyalty-based transactions.

In many real-world cases, the closed-loop wallet in India helps manage store credits, refund amounts, and reward points without requiring a closed wallet license. The usability is limited to the same platform, but the reliability makes the model valuable for brands that depend on repeat purchases. As India’s digital economy expands, closed wallets, hybrid models, and credit-based systems will continue to support fast, low-risk transactions within a regulated framework.

FAQs

1. Is a closed wallet allowed under RBI rules in India?Yes. A closed wallet is allowed under RBI rules because the value stored inside it can be used only for buying products or services from the same business. Since the balance does not leave the platform, it stays outside the licensing requirements that apply to semi-closed or open wallets. The issuer must still maintain proper records and transparent refund policies.

2. How is a closed wallet different from a semi-closed wallet in India?It works only within the issuing company’s platform, while a semi-closed wallet allows payments across approved external merchants. The semi-closed format requires a semi-closed wallet license, KYC compliance, and additional regulatory checks. The closed model has no such approval requirement because the value never leaves the internal system of the business.

3. Can a closed wallet balance expire as per Indian regulations?The Reserve Bank of India does not prescribe a specific validity period for it. Expiry depends on the issuing company’s internal policy. Most platforms mention the validity of credits or refund balances in their terms of service. Users should check the wallet’s expiry rules to understand how long the balance remains active.

4. How fast are refunds processed into a closed wallet in India?Refunds to a closed-loop wallet are typically instant because they do not depend on bank settlement cycles. When a user cancels an order or booking, the value is added to the wallet’s internal ledger within seconds. This speed makes the closed model suitable for e-commerce, travel, gaming, and food delivery platforms that handle frequent cancellations.

5. Does a closed wallet require KYC in India?No. It do not require KYC because it is not classified as a Prepaid Payment Instrument requiring RBI approval. The balance can be used only for the issuing company’s services, so risk is low. KYC becomes mandatory only when the wallet shifts into a semi closed wallet format that supports external merchant transactions.

6. What happens to my balance if the company shuts down its service?If a platform using a closed e-wallet shuts down, users may have limited options because the balance cannot be transferred outside the company’s system. Most responsible businesses issue refunds or allow redemptions before closing operations. The outcome depends entirely on the issuer’s financial policy and how they manage customer credits during discontinuation.

7. Can a closed wallet later be converted into a semi-closed wallet?Yes. A company can change it into a semi-closed loop wallet if it plans to allow payments across multiple merchants. Before doing this, the business must apply for a semi-closed wallet license, meet KYC requirements, and follow RBI rules on merchant onboarding, data security, and reporting.

8. Are closed wallets safe for digital payments in India?They are generally safe because all transactions stay inside one controlled network. Businesses use encrypted payment layers, secure ledgers, and internal verification steps to keep data protected. Users also benefit because no card or banking details are required during repeat purchases. The internal structure reduces exposure to external risks commonly seen in open systems.

9. What kind of businesses in India benefit most from closed wallets?Platforms with high refund volumes or frequent micro transactions benefit the most. E-commerce, travel aggregators, gaming platforms, online learning portals, and food delivery services use closed-loop wallets to manage store credits and instant refunds. The system helps them reduce transaction costs, improve customer retention, and create predictable payment flows.

10. Does RBI’s grievance redress system apply to closed wallets?No. It is outside RBI’s grievance mechanism because it does not fall under the regulated Prepaid Payment Instrument category. However, businesses must maintain fair practices, provide reliable customer support, and resolve issues related to refunds or wallet usage. Users should contact the issuing platform directly for any wallet-related concerns.