E-invoicing under GST refers to electronic invoicing where a GST invoice, credit note, or debit note is verified by a GSTN-authorised

Invoice Registration Portal (IRP). It is an invoice prepared by the supplier that is reported in the IRP, which verifies the data and generates an

Invoice Reference Number (IRN), making the document compliant for

Goods and Services Tax purposes.

E-invoicing follows a standardized digital format that ensures the authenticity and uniformity of invoice data across different systems. Based on practical implementation experience, it not only reduces manual errors and duplication but also improves reconciliation, helps in faster

filing of GST returns, and creates a clear audit report. This standardisation improves tax compliance while bringing better transparency and operational efficiency to the

invoice management.

What is E-Invoicing under GST?

E-invoicing under GST is a system where B2B invoices are electronically authenticated by the Invoice Registration Portal (IRP), which generates a unique Invoice Reference Number (IRN), digitally signs the invoice, and adds a

QR code. Only invoices with a valid IRN are treated as GST-compliant e-invoices.

Businesses generate invoices in their own ERP or

billing software and upload the invoice data in a prescribed format to the IRP for validation. After authentication, the invoice data is automatically shared with GSTR-1 and the

e-way bill system, where applicable, reducing manual entry and improving accuracy in GST reporting.

The e-invoicing system was approved in the

35th GST Council meeting on 21 June 2019 and was introduced in phases, starting with large enterprises and later implement to businesses with a ₹5 crore or more turnover.

Once an invoice is authenticated, the data is automatically shared with GSTR-1 and the e-way bill system. This removes manual entry, reduces errors, and helps finance teams maintain accurate and compliant GST records.

Latest E-Invoicing Turnover Limit under GST

The applicability of e-invoicing is based on aggregate turnover in any financial year from FY 2017-18 onwards, not just the current year. In practical implementations, many businesses miss this point and assume the limit applies only to the present year, which leads to non-compliance. Once the threshold is crossed in any year, e-invoicing becomes mandatory going forward.

Current Turnover Criteria for E-Invoicing

| Aggregate Turnover (₹) |

E-Invoicing Mandatory

From |

Applicability

Status |

| ₹500 crore and above |

1 October 2020 |

Applicable |

| ₹100 crore and above |

1 January 2021 |

Applicable |

| ₹50 crore and above |

1 April 2021 |

Applicable |

| ₹20 crore and above |

1 April 2022 |

Applicable |

| ₹10 crore and above |

1 October 2022 |

Applicable |

| ₹5 crore and above |

1 August 2023 |

Applicable (Current limit) |

Who is Required to Generate E-Invoices under GST?

E-invoicing is mandatory for GST-registered taxpayers whose aggregate turnover is ₹5 crore or more in any financial year from FY 2017-18 onwards. The requirement applies on a PAN basis, meaning turnover across all

GST registrations of the same

PAN must be considered.

Persons Required to Issue E-Invoices

| Category of Supply |

E-Invoice Required |

Remarks |

| B2B supplies |

Yes |

Mandatory once the threshold is crossed |

| Exports |

Yes |

Treated as B2B for e-invoicing |

| Supplies to SEZ units/developers |

Yes |

With or without payment of tax |

| Deemed exports |

Yes |

Covered under notified transactions |

Important Applicability Rules

- E-invoicing applies only to B2B transactions and specified supplies, not to B2C invoices.

- The requirement becomes applicable from the date a taxpayer falls under the notified turnover category.

- Once applicable, it continues even if turnover falls below ₹5 crore in later years.

- E-invoices must be generated for all eligible GSTINs linked to the same PAN.

From an implementation standpoint, businesses should first perform a PAN-level turnover check and then configure their ERP to generate IRNs only for eligible document types. This avoids common compliance issues, such as generating normal invoices instead of e-invoices for B2B supplies after crossing the threshold.

Transactions Covered vs Not Covered in E-Invoicing under GST

E-invoicing applies only to specified document types and supply categories notified under

Rule 48(4) of the CGST Rules, 2017. In practice, the correct identification of covered transactions is essential because issuing a normal invoice instead of an e-invoice for an eligible supply makes the invoice invalid for GST purposes, which can lead to

ITC denial for the recipient.

Transactions Covered under E-Invoicing

| Type of Document |

E-Invoice Applicable |

Legal Reference / Remarks |

| B2B tax invoices |

Yes |

Rule 48(4), CGST Rules |

| Export invoices |

Yes |

Treated as a B2B supply |

| Supplies to SEZ units/developers |

Yes |

With or without payment of tax |

| Deemed exports |

Yes |

Notified under the GST provisions |

| Credit notes (B2B) |

Yes |

Linked to the original e-invoice |

| Debit notes (B2B) |

Yes |

Must be reported to IRP |

E-invoicing is required only for documents that are otherwise required to be issued under

Section 31 of the CGST Act, 2017, and fall within the notified turnover threshold.

Transactions Not Covered under E-Invoicing

| Type of Supply |

E-Invoice Required |

Legal Reference / Remarks |

| B2C invoices |

No |

Not covered under Rule 48(4) |

| NIL-rated / exempt supplies to unregistered persons |

No |

Outside B2B scope |

| Bill of supply |

No |

Not a tax invoice |

| Delivery challan |

No |

Not an invoice document |

| Job work challans |

No |

No IRN required |

| Entities specifically exempt from e-invoicing |

No |

As per notifications |

Step-by-Step E-Invoicing Process under GST

E-invoicing is a validation workflow prescribed under

Rule 48(4) of the CGST Rules, 2017. The invoice is first created in the business system and then authenticated by the Invoice Registration Portal (IRP) to obtain an Invoice Reference Number (IRN) and

QR code.

Step 1 – Invoice creation

The supplier generates the invoice, credit note, or debit note in their ERP or billing software as per normal business practice.

Step 2 – Preparation of e-invoice data

The invoice details are converted into the prescribed JSON format based on the standard e-invoice schema. Most modern ERPs generate this automatically.

Step 3 – Upload to IRP

The JSON file is uploaded to the Invoice Registration Portal through API integration, a GST Suvidha Provider, or the IRP portal interface.

Step 4 – Validation by IRP

The IRP verifies key parameters such as GSTINs, document number, financial year, tax values, and mandatory fields. It also checks for duplicate invoices.

Step 5 – IRN generation and digital signing

After successful validation, the IRP generates a unique IRN, digitally signs the invoice, and creates a QR code containing core invoice details.

Step 6 – Receipt of authenticated e-invoice

The authenticated invoice, along with the IRN and QR code, is returned to the supplier. Only at this stage does the document become a valid GST e-invoice.

Step 7 – System integration and reporting

The validated invoice data is shared with the GST system for GSTR-1 auto-population and is made available for

e-way bill generation, where applicable. This reduces manual data entry and reconciliation errors.

Note: For notified taxpayers, issuing a B2B invoice without generating an IRN makes the invoice non-compliant under GST, which can affect

input tax credit eligibility for the recipient. Maintaining proper ERP–IRP integration and real-time validation checks helps avoid rejections and ensures accurate GST reporting.

Time Limit for Generating E-Invoice under GST

The time limit for generating an e-invoice is governed by Rule 48(4) of the CGST Rules, 2017, along with specific IRP validation rules. An e-invoice must be reported to the Invoice Registration Portal (IRP) within the prescribed time from the date of invoice generation. If the IRN is not generated within this time, the document is treated as a non-compliant GST invoice.

Current Time Limit Rule

| Category of Taxpayer |

Time limit to generate the IRN from the invoice date |

| Turnover ₹100 crore and above |

Within 7 days of the invoice date |

| Turnover below ₹100 crore (but covered under e-invoicing) |

No fixed day limit, but the IRN must be generated before issuing the invoice to the buyer |

Important Compliance Conditions

For taxpayers with a turnover of ₹100 crore or more, the IRP blocks IRN generation after 7 days from the invoice date. This means backdated reporting beyond the permitted window is not allowed.

For other notified taxpayers, although a fixed number of days is not prescribed, the IRN must be generated in real time, that is, before the invoice is issued or shared with the customer. Generating an IRN after issuing the invoice can lead to the document being treated as invalid.

Cancellation Time Limit

An e-invoice can be cancelled only:

- Within 24 hours of IRN generation

- Through the IRP system

After 24 hours, cancellation must be done through the GST portal by issuing a

credit note.

Mandatory Fields in E-Invoice under GST

The mandatory fields for e-invoicing are prescribed in the e-invoice schema notified under Rule 48(4) of the CGST Rules, 2017. These fields must be reported to the Invoice Registration Portal (IRP) for successful IRN generation. Missing or incorrect mandatory details are one of the most common reasons for IRP rejection.

Core Mandatory Fields for E-Invoice

| Category |

Mandatory Details |

| Supplier details |

Legal name, GSTIN, address, state code |

| Document details |

Document type (Invoice/Credit/Debit note), invoice number, invoice date |

| Buyer details |

Legal name, GSTIN (for B2B), place of supply, state code |

| Item details |

Description, HSN code, quantity, unit, taxable value, GST rate |

| Tax details |

CGST, SGST/UTGST, IGST amount, total tax value |

| Invoice value |

Total taxable value, total tax amount, invoice total |

| Place of supply |

State code of supply for GST determination |

| Shipping details |

Ship-to GSTIN and address (if different from buyer) |

| Payment details |

Mode of payment and outstanding amount (if applicable) |

| Reference details |

Original invoice reference in case of credit/debit notes |

Documents Required for E-Invoicing under GST

E-invoicing does not require uploading physical documents or separate attachments. From a compliance standpoint, what is required is accurate invoice data in the prescribed e-invoice schema, which is reported to the Invoice Registration Portal (IRP) for IRN generation as per Rule 48(4) of the CGST Rules, 2017.

Key Data Elements Required for E-Invoice Generation

| Document / Data Type |

Requirement |

Purpose |

| Tax invoice details |

Mandatory |

Core document for IRN generation |

| Credit note / Debit note (if applicable) |

Mandatory for such transactions |

Must reference original invoice |

| Supplier GSTIN and details |

Mandatory |

Identification of the supplier |

| Buyer GSTIN and details (B2B) |

Mandatory |

Determines tax applicability and ITC flow |

| Item details with HSN |

Mandatory |

Tax calculation and reporting |

| Tax values (CGST, SGST, IGST) |

Mandatory |

Validation of GST liability |

| Invoice number and date |

Mandatory |

IRN uniqueness check |

| Place of supply |

Mandatory |

Determines the type of GST |

| Shipping details (if different) |

Conditional |

Required for e-way bill linkage |

Exclusions from E-Invoicing under GST

Certain taxpayers and document types are specifically exempt from e-invoicing, even if their aggregate turnover exceeds the prescribed threshold. These exclusions are notified under Rule 48(4) of the CGST Rules, 2017 read with Notification No. 13/2020 – Central Tax and subsequent amendments.

Entities Exempt from E-Invoicing

| Category of Taxpayer |

E-Invoicing Applicability |

Legal Basis |

| Banks and financial institutions |

Not required |

Notified exemption |

| Non-banking financial companies (NBFCs) |

Not required |

Notified exemption |

| Insurance companies |

Not required |

Notified exemption |

| Goods Transport Agencies (GTA) |

Not required |

Notified exemption |

| Passenger transportation services |

Not required |

Notified exemption |

| Multiplex cinema operators |

Not required |

Notified exemption |

| Government departments and local authorities (in specified cases) |

Not required |

Notified exemption |

| SEZ units (as suppliers) |

Not required |

Notified exemption |

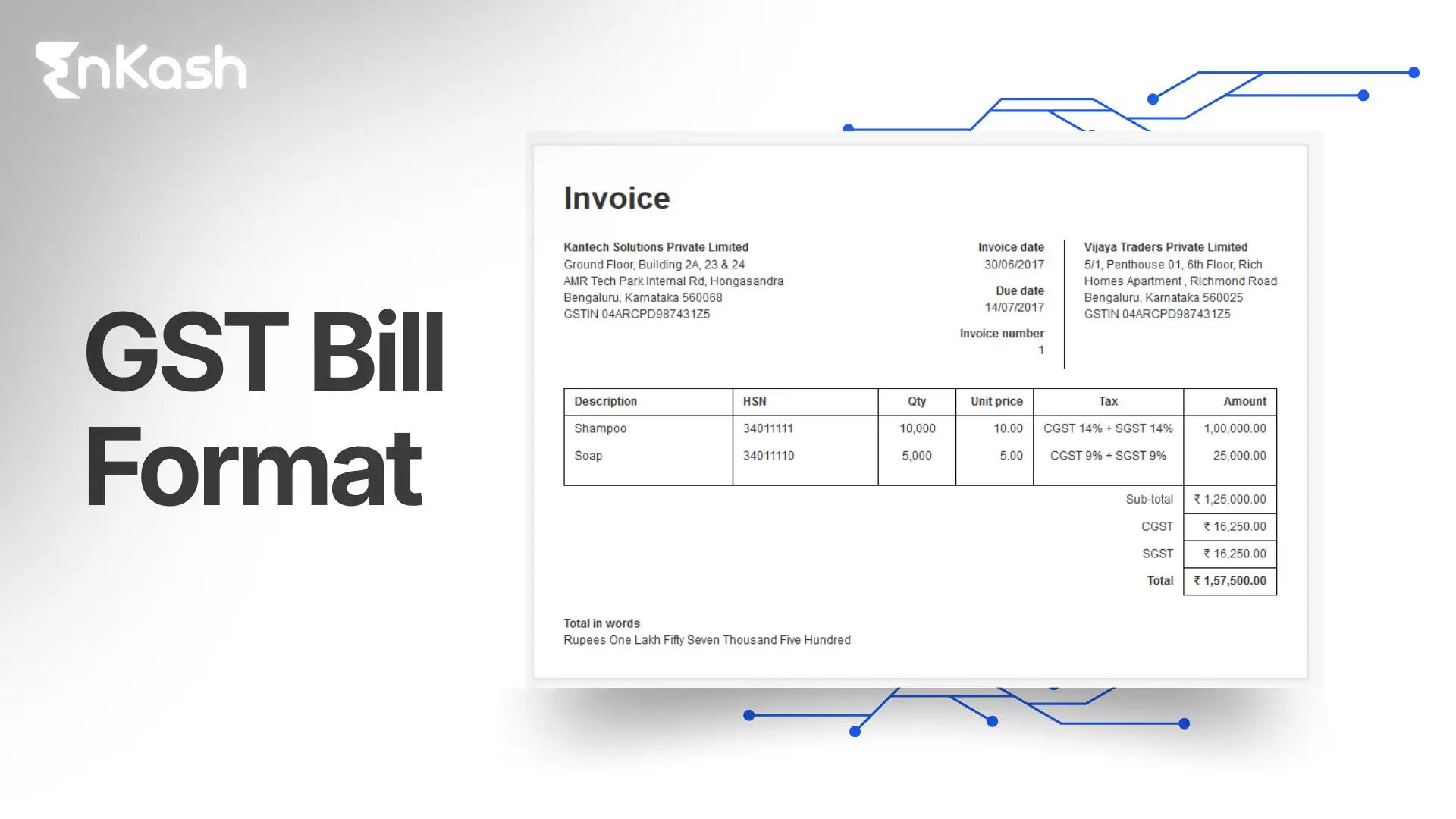

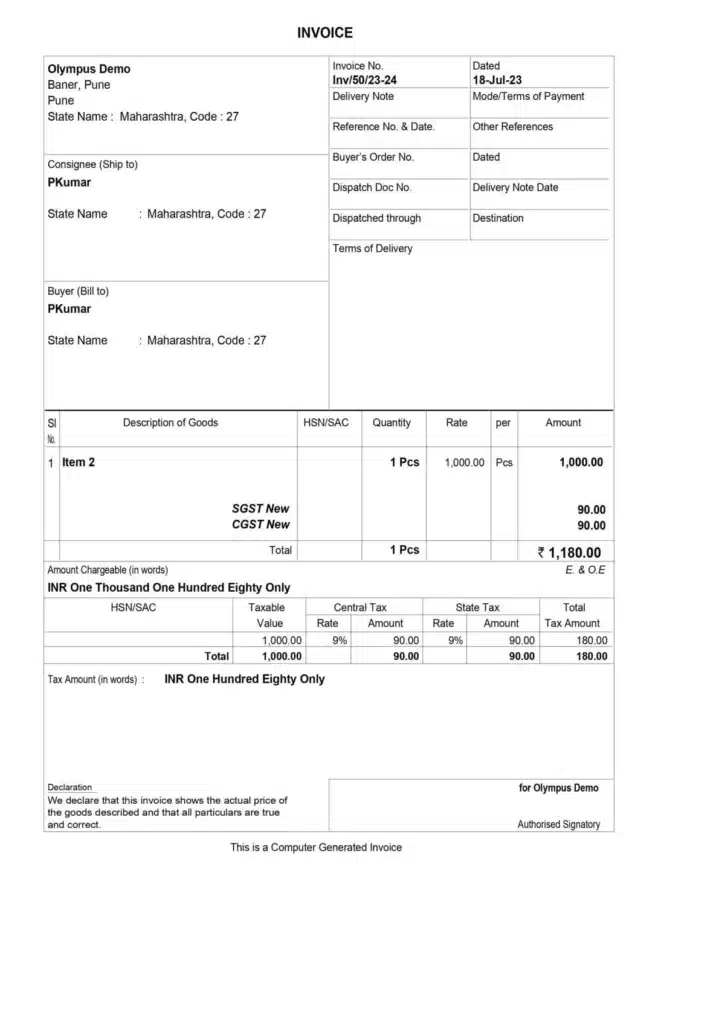

Format of E-Invoice

Benefits of E-Invoicing for Businesses

- Reduce GST errors because invoices are validated before sharing

- GSTR-1 gets filled automatically, saving filing time

- No repeated data entry for e-way bills.

- Easier ITC matching with customers

- Clear digital trail for audits.

- Faster month-end reconciliation

- Less risk of issuing invalid invoices

- Better control over high-volume billing.

Conclusion

E-invoicing has moved from being a regulatory requirement to a core part of GST compliance for businesses with ₹5 crore or more aggregate turnover. By validating invoices through the Invoice Registration Portal (IRP) and generating a unique IRN, the system ensures that only accurate and standardised invoice data is reported in GST returns.

From a practical implementation perspective, businesses that integrate their ERP with an IRP benefit from real-time validation, automatic GSTR-1 population, faster e-way bill generation, and fewer reconciliation issues. It also reduces the risk of invalid invoices and input tax credit disputes.

Adopting a structured e-invoicing workflow, maintaining accurate master data, and generating IRNs at the time of invoice creation are essential for consistent compliance. As GST reporting becomes more data-driven, e-invoicing plays a key role in improving transparency, audit readiness, and overall financial control.

Also Read

FAQs about GST