An employee tax benefit wallet is a prepaid wallet that lets a company route specific salary allowances — such as meals, fuel, gifts, telecom, and leave travel — into separate, purpose-controlled balances that qualify for tax exemptions under the Income Tax Rules. Employees spend from each wallet at eligible merchants, finance teams track every transaction digitally, and the company delivers higher take-home pay without increasing gross salary cost. A tax benefit wallet works best when HR, payroll, and finance agree on the benefit value, merchant rules, and payroll treatment before rollout.

Companies adopt tax benefit wallets to replace cash allowances, paper vouchers, and receipt-heavy reimbursement cycles with a single, auditable system. The wallet separates each allowance into its own category, applies spending controls at the point of payment, and produces the digital records payroll teams need at year-end.

What is an Employee Tax Benefit Wallet

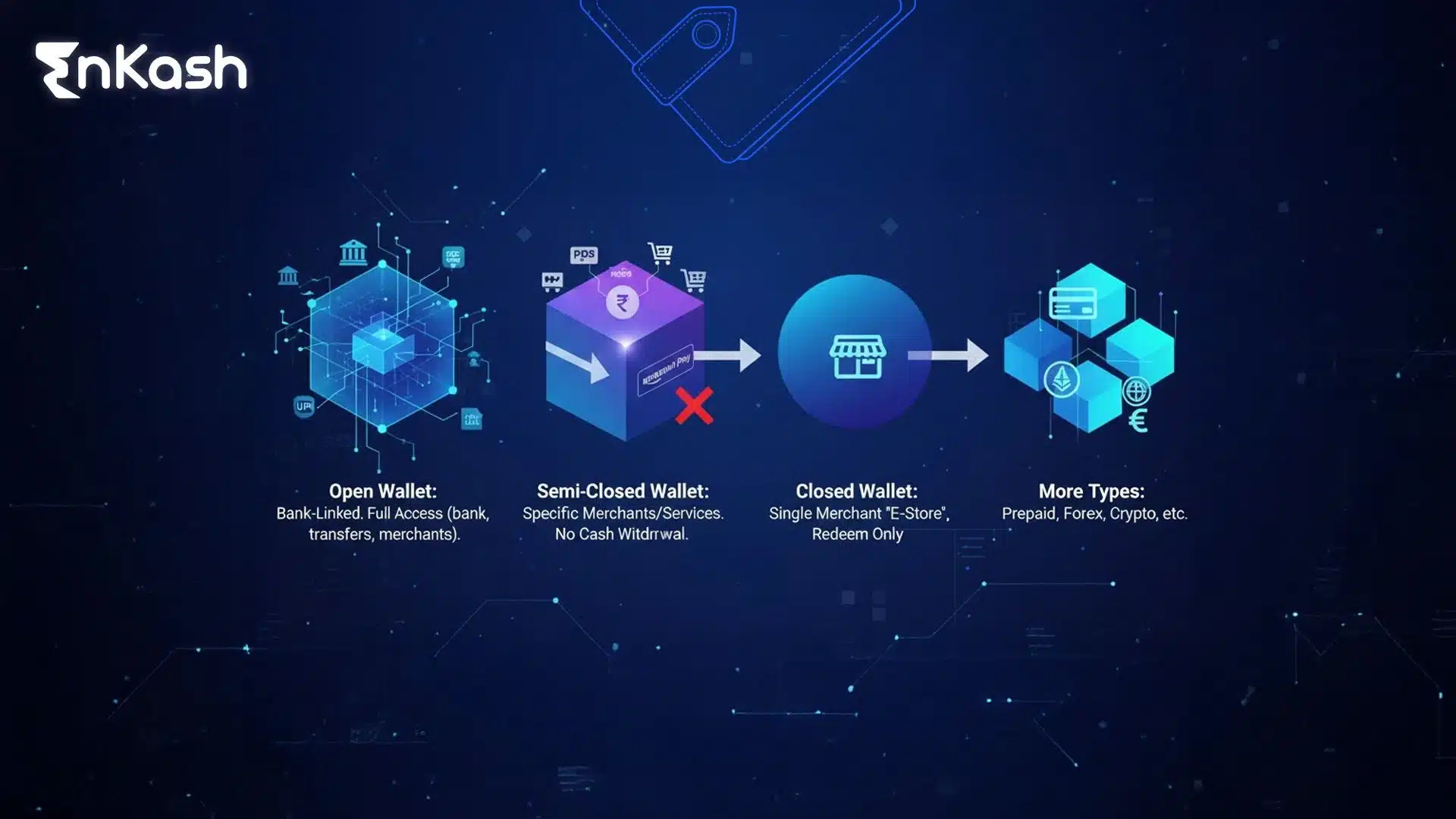

An employee tax benefit wallet is a digital wallet that holds one or more tax-exempt allowance categories on behalf of an employee. Each category — meal, fuel, gift, telecom, leave travel allowance (LTA), books and periodicals — sits in its own sub-wallet with its own balance, spending rules, and documentation requirements.

The purpose is narrow and deliberate. Unlike a general-purpose prepaid balance, a tax benefit wallet is designed so that each rupee is spent only on the category it belongs to. When category controls are enabled, an employee cannot use the meal balance to buy fuel, or the gift balance to pay a phone bill. This separation is what allows the benefit to stay compliant with income tax rules and survive a payroll review.

Read More: Multi-Wallet Prepaid Card: Benefits, Wallet Types, and Tax Advantages

A tax benefit wallet typically includes:

- Category-specific balances mapped to tax-exempt allowances.

- Merchant-category controls that restrict where each wallet can be used.

- Employer-defined limits, eligibility, and loading schedules.

- Digital transaction records for payroll and audit.

- A payment method — UPI, a physical or virtual card, or both.

- Receipt handling for categories that require proof of spend.

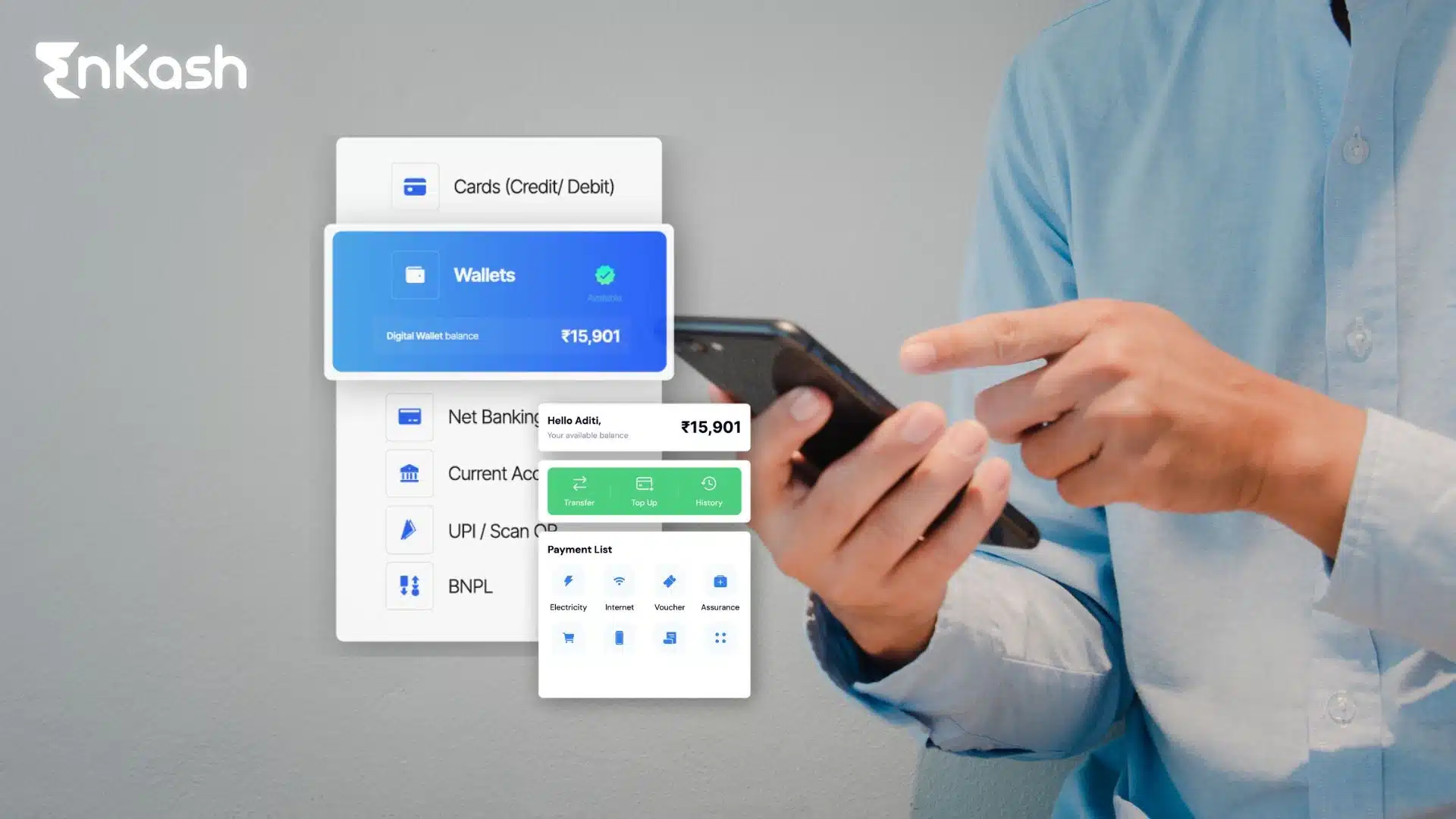

How Does an Employee Tax Benefit Wallet Work?

An employee tax benefit wallet works when the employer assigns allowance values to each category, funds the wallet, and the platform checks every payment against the balance, merchant type, and company rules before approving it. The employee spends at an eligible merchant, and the system records the transaction for finance and payroll review.

The workflow has clear stages:

- HR sets up eligibility and categories: HR uploads employee details, selects which wallet categories the company will offer, and maps each employee to the correct benefit structure.

- Finance confirms the loading amount: Finance sets the value per category based on the company's CTC structure, employee grade, and benefit policy.

- The platform funds the wallet: Funds move from the company account into the employee's category balances, either on a fixed schedule or through a manual load.

- The employee makes a payment: At the point of payment, the wallet checks the amount, available balance, merchant category, and permitted usage before approving or declining.

- The system records and validates the spend: Every transaction is logged. For categories that require proof, the employee submits a receipt, which the platform matches against the transaction.

- Finance reviews month-end activity: Finance checks loaded value, used value, unused balances, and exceptions before the next cycle and before year-end tax computation.

- Wallet Categories Companies Commonly Offer

- Most companies do not activate every category at once. They start with the highest-impact wallets and expand as their benefit policy matures.

This structure lets employers catch incorrect usage early and gives employees a clear reason whenever a payment succeeds or fails.

Wallet Categories Companies Commonly Offer

Most companies do not activate every category at once. They start with the highest-impact wallets and expand as their benefit policy matures.

| Wallet Category | Typical Use | Receipt Required |

|---|

| Meal | Daily food and non-alcoholic beverages at eligible F&B merchants | No — based on wallet usage |

| Gift & Rewards | Festival vouchers, birthdays, and work anniversaries | No — based on wallet usage |

| Fuel & Conveyance | Petrol, diesel, and conveyance within policy | Yes — on actuals |

| Telecom & Internet | Mobile and broadband bills | Yes — on actuals |

| Leave Travel Allowance | Travel during approved leave | Yes — on actuals |

| Books & Periodicals | Professional books, journals, and subscriptions | Yes — on actuals |

The meal and gift wallets are usually the starting point because they are the simplest to administer and do not require employees to submit a receipt for every transaction. Categories such as fuel, telecom, and LTA deliver value on actual spend and need supporting documentation, which is where a provider's receipt-management capability matters.

Employee Tax Benefit Wallet: The 2026 Rule Position

Under the Income Tax Rules, 2026, the employer-provided meal benefit limit is reported at ₹200 per meal, subject to conditions such as provision during working hours and use only at eating joints. This is a significant increase from the earlier ₹50 per meal limit. The gift and festival voucher exemption is reported at ₹15,000 per year.

A calculation many employers use for planning:

| Calculation Step | Amount |

|---|

| Eligible value per meal | ₹200 |

| Two meals per working day | ₹400 |

| Monthly value for 22 working days | ₹8,800 |

| Illustrative annual value | ₹1,05,600 |

This ₹1,05,600 figure is illustrative. The actual exempt value depends on the meal count, working days, payroll mapping, and company policy. If a company loads more than the eligible amount, payroll teams should review the excess because it may become a taxable perquisite depending on the salary structure.

One point every employer should confirm with its own tax advisor: the applicability of the meal exemption under the New Tax Regime (Section 115BAC) is a matter employers should verify against the final rule text and their own tax opinion before building it into salary structures or employee communication. Treat the exemption limits above as the reported position, and confirm regime treatment and payroll classification with a qualified advisor before rollout. An incorrect classification can turn a planned tax benefit into a taxable perquisite, so the payroll review is not optional.

Read More: Flexi-Benefits for Employees in India

Benefits for Employees

A tax benefit wallet makes allowances visible, usable, and easier to plan through the month, while supporting higher take-home pay when the benefit is structured correctly.

1. Higher take-home pay. By moving eligible

CTC components into tax-exempt categories, employees keep more of their salary compared with receiving the same amount as fully taxable cash — subject to correct structuring and applicable rules.

2. Less reimbursement follow-up.

For meal and gift categories, employees spend directly without saving every bill or waiting for claim approval.

3. Clear visibility. Employees can check each wallet balance and transaction history before spending, so they always know how much value remains.

4. One instrument for many benefits. A single card and app can carry meal, fuel, gift, telecom, and LTA balances, so employees do not juggle multiple cards or logins.

Benefits for Employers

For employers, a tax benefit wallet turns scattered allowances into a budgeted, auditable, and easy-to-update benefit programme.

- Cost-neutral CTC optimisation. Restructuring existing salary components into tax-advantaged categories improves employee take-home pay without raising the company's CTC outlay.

- Cleaner compliance trail. Category controls, digital records, and receipt validation give finance a defensible position during payroll checks and audits.

- Lower benefit leakage. Access can be paused or closed the moment an employee changes role, goes on leave, or exits — so benefits do not continue for people who no longer qualify.

- Better cost planning. Finance can compare loaded value against actual usage and adjust allocations for the next cycle with cleaner numbers.

- Stronger retention narrative. A visible, tax-efficient benefit strengthens the employer value proposition in a competitive hiring market.

Read More: Corporate Cards vs. Petty Cash vs. Reimbursements: The True Cost of Each

How to Choose an Employee Tax Benefit Wallet Provider

Not all tax benefit wallets are built the same way, and the differences matter more than the marketing suggests. The structure behind a provider — how it is licensed and how employees actually pay — determines how reliable, flexible, and future-proof the programme will be. Use these criteria to evaluate any provider, including the established names in the category.

1. Does the provider hold its own RBI licence, or does it operate through bank partnerships?

Some providers issue wallets under their own Reserve Bank of India Prepaid Payment Instrument (PPI) licence. Others operate through co-branded partnerships with banks, which means their feature rollout, transaction rules, and issue resolution depend on a partner bank's priorities and timelines. A provider that controls its own licensing stack can generally move faster on product changes and resolve operational issues without a third party in the loop. For reference, Zaggle operates through bank partnerships rather than holding its own PPI issuance licence, while some newer players issue directly.

2. Can employees pay by UPI, or only by card?

This is the single biggest usability difference in the category today. Legacy meal-card programmes — including long-established providers such as Pluxee (formerly Sodexo) — rely primarily on card swipes or a restricted merchant network. A wallet with native UPI support lets employees scan and pay at virtually any UPI-accepting merchant in India, from a neighbourhood restaurant to a fuel pump, without depending on whether a merchant carries a specific card network or is part of a closed loop. For a benefit employees are meant to use every day, everyday acceptance is decisive.

3. Is it a true multi-wallet with category controls?

A genuine multi-wallet card keeps meal, fuel, gift, telecom, and LTA balances separate on a single instrument, with merchant-category rules enforced at the point of payment. This prevents benefit mixing and keeps each category clean for payroll and tax review.

4. How does it handle compliance and receipts?

Categories such as fuel, telecom, and LTA require proof of spend. A provider with built-in receipt capture and OCR validation — matching submitted receipts against actual transactions — removes most of the manual review burden and strengthens the audit trail. Ask whether category-level merchant restrictions are enforced automatically, or left to the employer to police.

5. How fast can you go live, and how much runs on self-service?

Look for DIY onboarding, bulk employee upload, and a dashboard that lets HR add, pause, and offboard employees without raising a support ticket for every change. The best programmes are operational before the next payroll cycle.

6. Are the product and support built for the Indian market?

Roadmap and support responsiveness matter over the life of a contract. Providers whose product decisions are made for the Indian market — rather than set by a global parent's priorities — tend to ship India-specific features faster and respond to local regulatory changes sooner.

Common Mistakes Companies Make

- Loading above the eligible limit without flagging it. Any excess over the exempt value may be taxable. Payroll should review overloads before processing salaries.

- Treating the wallet like cash. Without category controls, spending can drift outside eligible use and lose its tax standing.

- Skipping the tax opinion. Relying on a headline exemption figure without confirming regime treatment and payroll classification is the most common — and most expensive — mistake.

- Choosing on price alone. A cheaper wallet that employees cannot use at everyday merchants delivers a lower real benefit than a slightly costlier one with broad UPI acceptance.

- Ignoring offboarding. Benefits that continue after an employee exits create leakage and reconciliation problems.

How EnKash Approaches the Tax Benefit Wallet

EnKash offers an employee benefit multi-wallet card built around the criteria above. Companies can activate meal, fuel, gift, telecom, LTA, and books & periodicals wallets on a single card, keep each benefit category separate, and track usage through digital records.

Own RBI PPI licence. EnKash issues wallets under its own Reserve Bank of India Prepaid Payment Instrument licence, so it controls its technology and compliance stack directly rather than depending on a partner bank for core issuance.

Native UPI and card. Each wallet supports UPI scan-and-pay alongside a physical and virtual prepaid card, so employees can pay at everyday merchants across India rather than being limited to a closed network.

Category controls and OCR receipts. Merchant-category rules are enforced at the transaction level, and a built-in OCR engine validates submitted receipts against actual spend for the categories that require proof — reducing manual review for HR and finance.

DIY onboarding and independent HR control. Companies can upload employees in bulk, configure allowances, and pause or offboard staff from the dashboard, with automated or manual fund loading to fit the payroll cycle.

The result is a tax benefit wallet designed for everyday usability and a clean compliance trail — the two things that determine whether a benefit programme actually delivers value once it is live.

Closing Thoughts

An employee tax benefit wallet gives allowances a clear, auditable structure and can meaningfully improve take-home pay when it is set up correctly. The important decisions come before rollout: which categories to activate, what value to load, how to map each benefit in payroll, and — critically — confirming the tax treatment, including regime applicability, with a qualified advisor. On the provider side, the structural questions matter most: whether the provider holds its own licence, whether employees can pay by UPI at everyday merchants, and whether compliance is built into the product rather than left to the employer. Companies evaluating options can consider the EnKash employee benefit multi-wallet card as a practical starting point and talk to the EnKash team for a walkthrough tailored to their CTC structure.

FAQs

What is an employee tax benefit wallet?It is a prepaid wallet that holds tax-exempt salary allowances — such as meal, fuel, gift, telecom, and LTA — in separate category balances. Employees spend from each wallet at eligible merchants, and the structure supports tax exemptions when set up in line with the applicable income tax rules and payroll documentation.

How is a tax benefit wallet different from a normal prepaid card?

A normal prepaid card holds a single, general-purpose balance. A tax benefit wallet holds multiple category-specific balances with merchant controls, so each allowance is spent only on its eligible category and stays clean for payroll and tax review.

Is the meal benefit available under the new tax regime?

Employers should confirm the applicability of the meal exemption under the New Tax Regime (Section 115BAC) with their own tax advisor against the final rule text before relying on it. Treat the reported exemption limits as the starting position and verify regime treatment and payroll classification before rollout.

How much can an employee save with a tax benefit wallet?

The savings depend on the employee's tax slab, the allowances activated, and correct structuring. As an illustration, an employee who fully uses a meal allowance calculated at ₹200 per meal (around ₹1,05,600 a year) can reduce taxable income by that amount, subject to eligibility and applicable rules. Payroll teams should confirm the treatment for each employee.

Do employees need to submit receipts for every wallet?

No. Meal and gift wallets are typically usage-based and do not require receipts. Fuel, telecom, LTA, and books & periodicals are on actuals and require supporting documentation, which OCR-based receipt tools can validate automatically.

Can one card hold multiple benefit categories?

Yes. A multi-wallet card carries several category balances — meal, fuel, gift, telecom, LTA — on a single instrument, applying the correct wallet based on the merchant category and configured rules.

What happens to unused wallet balances at year-end?

Treatment follows company policy. Unused amounts are commonly moved to a general-purpose balance and reported to HR, so the corresponding value can be added back as taxable income in the employee's final computation.

Does the provider's RBI licensing model matter?

Yes. A provider that issues under its own RBI PPI licence controls its product and compliance stack directly. A provider operating through bank partnerships depends on a partner bank for feature changes, transaction rules, and issue resolution, which can slow things down.

Why does UPI support matter for a meal or benefit wallet?

Because employees use these wallets daily. UPI support lets them scan and pay at virtually any UPI-accepting merchant, rather than being limited to card-network terminals or a closed merchant list — which directly affects how usable the benefit is.

How quickly can a company go live?

With a self-service provider, most companies can be operational before their next payroll cycle. Onboarding usually involves agreement signing, dashboard setup, bulk employee upload, allowance configuration, and the first fund load.

What should HR check before choosing a provider?

Confirm the licensing model, UPI and card acceptance, multi-wallet category controls, receipt and compliance handling, onboarding speed, and whether the product and support are built for the Indian market. Then align the benefit structure with a tax advisor before rollout