What is a Trial Balance?

A trial balance is a statement that summarises the closing balances of all ledger accounts of a business at a specific point in time. It is an internal accounting statement that lists the adjusted closing balances of every general ledger account.

These ledger accounts include capital accounts, revenue accounts, and expenditure accounts, all recorded in the books of accounts up to a particular date. Each account in the trial balance shows either a debit balance or a credit balance, depending on the nature of the account.

In a trial balance, all debit balances are recorded on the debit side, and all credit balances are recorded on the credit side. When the accounting entries are correctly recorded, the total of the debit side equals the total of the credit side, which helps verify the arithmetic accuracy of the ledger postings.

The balances shown in the trial balance are then used to prepare the Trading Account, Profit and Loss Account, and the Balance Sheet, making it an essential step in the accounting process.

Uses of the Trial Balance

| Purpose | Explanation |

|---|

| Check arithmetic accuracy | A trial balance verifies that the total of debit balances equals the total of credit balances. If both sides tally, it confirms numerical accuracy in ledger postings; differences indicate errors in posting, totaling, or balancing. |

| Detect and correct errors | It helps identify errors such as wrong-side entries, omitted transactions, or incorrect amounts before they affect the profit and loss account or balance sheet. |

| Simplify the preparation of final accounts | The trial balance acts as the base document for preparing the trading account, profit and loss account, and balance sheet by bringing all ledger balances into one place. |

| Maintain internal control | Regular preparation strengthens internal control by allowing management to review records, identify inconsistencies, and ensure the timely updating of all accounts. |

| Provide a snapshot of financial records | It offers a quick overview of all ledger accounts, showing debit and credit balances at a glance, which helps accountants and auditors assess the books efficiently. |

Features of Trial Balance

The trial balance may look simple, yet it holds several distinct features that make it a crucial part of the accounting process. Each feature helps maintain order, accuracy, and clarity while summarizing the results of all ledger accounts. Below are the main features explained in detail.

Prepared on a Specific Date

A trial balance is always prepared on a particular date, usually at the end of an accounting period. It shows the financial position of all ledger accounts as of that day. Businesses can create it monthly, quarterly, or yearly, depending on their reporting needs. The date ensures that the statement represents the exact stage of the accounts being reviewed.

Summarizes All Ledger Balances

The statement includes the closing balances of every ledger account maintained by the business. Each account is recorded either on the debit or the credit side according to its nature. This summary gives a clear idea of which accounts have increased or decreased over the accounting period and makes further reporting easier.

Prepared under the Double-Entry System

The trial balance works on the principle that every transaction has two sides—debit and credit. Because all entries are made following the double-entry system, the total of the debit side must equal the total of the credit side. This equality confirms that the posting of entries has been done correctly.

Contains Two Columns: Debit and Credit

The trial balance format follows a two-column structure. One column records all debit balances, such as assets and expenses. The other column lists credit balances, such as liabilities, income, and capital. When these columns are totaled, the sums should match if no posting error exists.

Used as an Internal Statement

The trial balance is prepared for internal use and not shared publicly. It serves as a tool for accountants, auditors, and management to check the accuracy of the books before preparing financial statements. Since it is a working document, it can be corrected and revised as needed before finalization.

Acts as the Basis for Final Accounts

Every profit and loss account and balance sheet starts with the figures taken from the trial balance. Once the totals are confirmed, these balances are used to prepare final reports. The statement ensures that all the accounts required for financial reporting are included and accurate.

Ensures Mathematical Accuracy but Not Complete Accuracy

When a trial balance tallies, it only confirms that the mathematical posting is correct. It cannot reveal every kind of mistake, such as entries placed in the wrong account or omitted transactions. Still, it serves as a reliable first checkpoint for verifying the records.

Rules of the Trial Balance

| Rule | Explanation |

|---|

| Debit and Credit Rule | Every transaction affects two accounts under the double-entry system. Assets and expenses are recorded on the debit side, while liabilities, capital, and income are recorded on the credit side. |

| Equality of Totals | The total of all debit balances must always equal the total of all credit balances. This confirms the mathematical accuracy of ledger postings. |

| Sequence of Accounts | Accounts are generally arranged in a standard order—personal, real, and nominal—to make verification and reference easier. |

| Balancing of Accounts | All ledger accounts must be properly balanced before preparing the trial balance. Unbalanced or incomplete accounts can lead to errors in the final statement. |

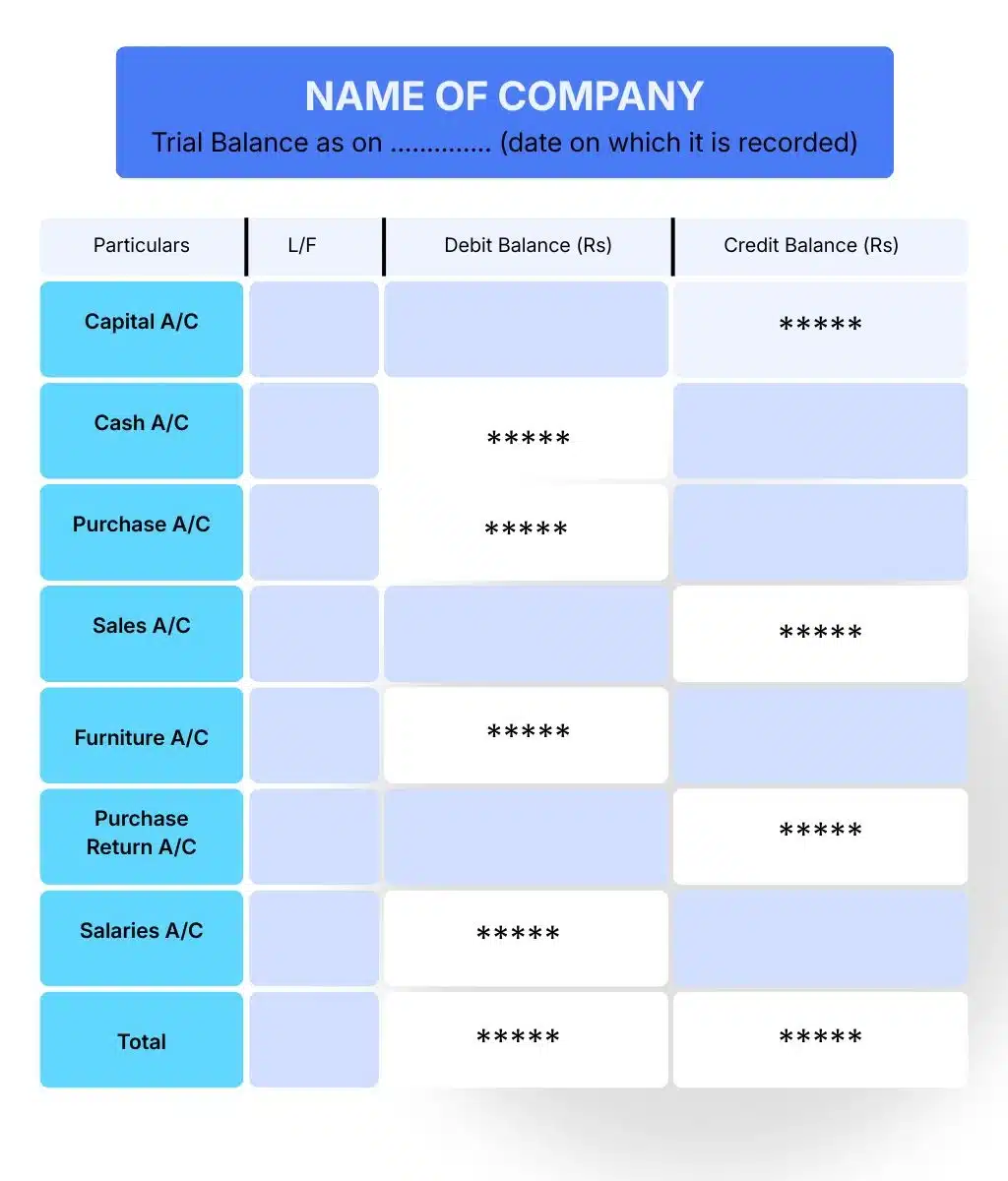

A trial balance follows a simple and uniform layout that helps present all ledger balances clearly. The format makes it easy to identify each account, check the totals, and verify if the books are balanced. Accountants prepare it at the end of an accounting period to ensure that all entries have been correctly recorded.

A trial balance format usually contains four main columns. The first column lists the name of each account, the second shows the ledger folio number, and the last two columns display the debit and credit balances. Each figure is taken directly from the ledger after balancing the accounts.

Heading and Presentation

Every trial balance must have a clear heading that includes the business name, the title “Trial Balance,” and the date it was prepared. For example:

“Trial Balance as on .........”

How to Read the Columns

The debit column includes assets and expenses, while the credit column includes liabilities, income, and capital. If an account has a debit balance, it is written under the debit side, and if it has a credit balance, it is placed under the credit side. The total of both sides must be equal when all entries are correct.

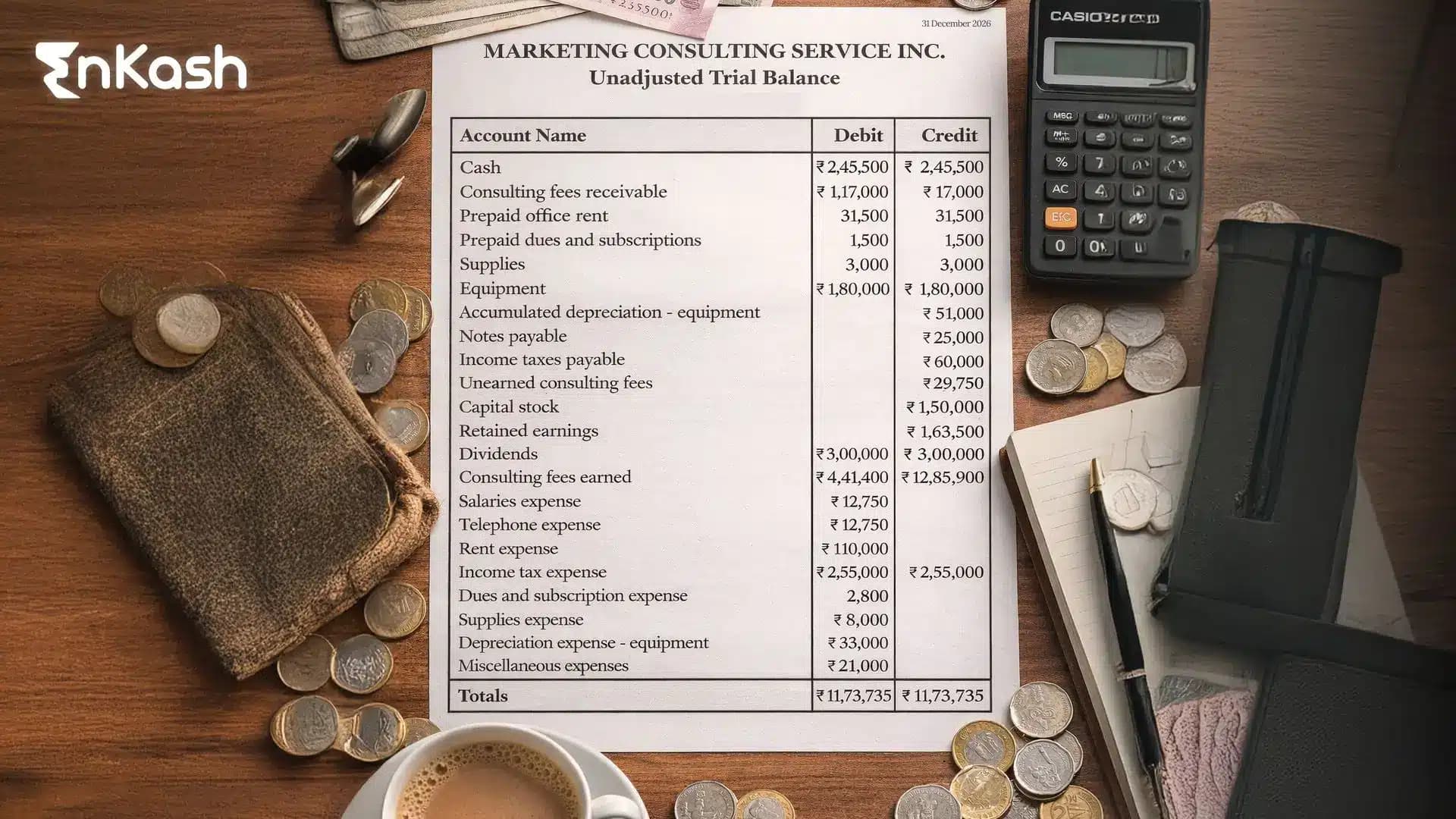

In a practical scenario, the trial balance image or a printed format generated by accounting software such as Tally or Zoho will look similar to the example table above. It may also include additional columns for notes or references, depending on the business setup.

The design of the trial balance helps in locating errors easily and provides a quick summary of all the ledgers. It also allows the accountant to prepare adjustments, create the profit and loss account, and move smoothly to the balance sheet.

How to Prepare a Trial Balance

Before preparing final accounts, accountants first prepare a trial balance to ensure that all ledger entries are accurate and properly classified. The process follows a clear sequence and should be done carefully to avoid errors.

Step 1: Close all ledger accountsBegin by closing all accounts in the general ledger. This involves totaling each ledger account and determining its closing balance as of the chosen date.

Step 2: Prepare the trial balance formatCreate a trial balance worksheet with separate columns for account names, debit balances, and credit balances. Ensure that the list includes all accounts maintained in the general ledger.

Step 3: Enter account balancesTransfer the closing balance of each ledger account to the trial balance. Expense and asset accounts should appear on the debit side, while liability, capital, and revenue accounts should appear on the credit side.

Step 4: Add the debit and credit columnsCarefully total both the debit and credit columns. Accuracy at this stage is essential, as even a small error can affect the final outcome.

Step 5: Verify the totalsIf the total of debit balances matches the total of credit balances, the trial balance is said to be balanced. If there is a difference, it indicates a mathematical error in posting, totaling, or balancing the ledger accounts, which must be identified and corrected before proceeding further.

Errors in Trial Balance

A trial balance may fail to tally when mistakes occur during recording, posting, or totaling entries. These errors can affect the balance in different ways and need to be identified before preparing the final accounts.

Errors that Affect the Trial Balance

These mistakes cause the debit and credit totals to become unequal.

- Posting an entry on the wrong side of the ledger.

- Entering a wrong amount in the ledger or trial balance.

- Omitting an account balance from the statement.

- Recording a transaction on one side only.

Errors that Do Not Affect the Trial Balance

These mistakes keep the totals equal but still make the accounts incorrect.

- Complete omission of a transaction from the books.

- Recording an entry in the wrong account, but on the correct side.

- Errors of principle, such as treating capital expenses as revenue.

- Compensating errors, where two mistakes cancel each other.

Use of Suspense Account

When the exact difference cannot be traced immediately, the accountant opens a suspense account. The difference is placed there temporarily until the mistake is located and corrected, after which the suspense account is closed.

Bills Receivable in Trial Balance

Bills receivable represent the amount a business has yet to receive from customers against accepted bills of exchange. These bills are treated as assets because they show money that will be received in the future.- Meaning of Bills ReceivableA bill receivable is a written promise from a debtor to pay a specific amount on a set date. Once accepted, it becomes a legal document confirming the payment obligation.

- Treatment in Trial BalanceBills receivable are recorded on the debit side of the trial balance, as they represent an asset. If any bill has been dishonored or not accepted, it is removed from this account and recorded as a receivable or bad debt, depending on the situation.

Types of Trial Balance

A trial balance is prepared in different forms depending on the stage of accounting and the reason for preparing it. Each type serves a unique purpose in checking and confirming the accuracy of the accounts. Understanding these types helps in knowing how the accounting process moves step by step before final statements are created.

Unadjusted Trial Balance

The unadjusted trial balance is the first version prepared after all transactions have been recorded and posted in the ledger. It lists every account with its closing balance exactly as it appears before any adjustments are made. This version helps the accountant confirm that the books are balanced and that the debit and credit totals are equal. If the two sides do not tally, the accountant reviews the ledger to find where the mistake occurred. The unadjusted version serves as the starting point for preparing the final statements.

Adjusted Trial Balance

The adjusted trial balance is prepared after all necessary adjustments are made at the end of the period. These adjustments may include entries for accrued income, outstanding expenses, prepaid expenses, or depreciation. Once these entries are added, the ledger balances are updated, and the statement is prepared again. This version shows the most accurate balances that will be used for the profit and loss account and the balance sheet.

Post-Closing Trial Balance

The post-closing trial balance is created after the income and expense accounts are closed for the year. It includes only the permanent accounts, such as assets, liabilities, and capital. All temporary accounts, including revenue and expenses, are closed and transferred to capital. The purpose of this version is to confirm that all closing entries have been recorded correctly and that the books are ready for the next accounting period.

Periodic or Interim Trial Balance Image or Example Table Balance

Some businesses prepare a trial balance during the accounting year to check the progress of their accounts. This is called a periodic or interim trial balance. It gives management a quick look at the financial position without waiting until the end of the year. Preparing it helps in making decisions, reviewing expenses, and planning for adjustments in advance.

What is the Difference Between a Trial Balance and a Balance Sheet?

A trial balance and a balance sheet are closely related but serve different purposes in accounting. Both summarize financial data, yet they differ in form, timing, and function.

| Basis of Difference | Trial Balance | Balance Sheet |

|---|

| Purpose | Prepared to check the arithmetical accuracy of accounting records | Shows the true financial position of the business on a specific date |

| Stage of Preparation | Prepared before final accounts are created | Prepared after the Profit & Loss Account, using adjusted and finalized figures |

| Content | Includes all ledger account balances (debit and credit) | Shows assets, liabilities, and capital to present net worth |

| Format | Two-column format: Debit and Credit | Divided into two main sections: Assets and Liabilities |

| Scope | Used as an accuracy-check tool | Used to understand the financial strength, stability, and position of the business |

Benefits of Trial Balance

A trial balance plays an important role in keeping financial records accurate and organized. It acts as a checkpoint between bookkeeping and the preparation of final accounts.

- Checks Mathematical Accuracy: By comparing debit and credit totals, the Trial Balance confirms that all transactions have been recorded correctly and that the books are in balance.

- Helps in Detecting Errors: If the two sides do not match, it signals mistakes such as missing entries, wrong postings, or incorrect totals. Detecting these early prevents larger issues later.

- Simplifies Preparation of Final Accounts: Since all ledger balances appear together, creating the profit and loss account and the balance sheet becomes easier and faster.

- Supports Internal Control: A trial balance helps management ensure that every account is complete, consistent, and recorded under the correct head.

- Assists in Audit and Review: Auditors rely on it to trace balances and verify that ledgers are maintained properly before detailed checking begins.

Limitations of the Trial Balance

A trial balance helps in verifying the mathematical accuracy of the books, but it does not guarantee that every entry is correct. It has a few limitations that must be understood before relying on it completely.

- Cannot Detect All Types of Errors: The trial balance cannot identify mistakes such as entries made in the wrong accounts, omitted transactions, or errors of principle. It only ensures that the debit and credit sides match.

- Does Not Show Financial Position: The statement does not reflect the profit, loss, or overall financial health of the business. It is a working document, not a financial report.

- Relies on Correct Ledger Posting: If the original entries in the ledgers are wrong, the trial balance will still tally. This can give a false sense of accuracy.

- Limited Use for Decision-Making: The trial balance cannot be used alone for analysis or business decisions since it only lists account balances without interpretation.

Conclusion

The trial balance accounting process is an essential part of every bookkeeping system. It ensures that all debit and credit entries recorded in the ledgers are accurate and balanced before final accounts are prepared. By listing every account with its closing balance, the trial balance confirms the mathematical accuracy of the books and highlights any mismatches that may exist.

The purpose of preparing a trial balance is to verify the correctness of entries, simplify the preparation of financial statements, and maintain internal control over accounts. It acts as a checkpoint that gives accountants and auditors confidence in the reliability of the records.

Following proper trial balance rules ensures that the data entered follows the double-entry principle, where every debit has an equal credit. When prepared carefully, a trial balance strengthens the foundation of financial reporting, supports error detection, and assures that the books of accounts reflect the true financial position of the business.

FAQs

Q1. What is a Trial Balance in accounting?A Trial Balance is a statement that lists all ledger account balances on a specific date to ensure total debits equal total credits. It acts as a checkpoint before preparing final financial statements.

Q2. Why is a Trial Balance important for businesses in India?A Trial Balance ensures the accuracy of accounting records as required under Indian accounting practices. It helps detect posting errors early and supports the preparation of financial statements in line with statutory norms.

Q3. How often should a Trial Balance be prepared?In India, most businesses prepare a Trial Balance monthly, quarterly, or annually—depending on reporting needs, audits, or compliance schedules.

Q4. What is the difference between a Trial Balance and a Balance Sheet?A Trial Balance checks arithmetic accuracy and lists all ledger balances, while a Balance Sheet shows the financial position of a business with assets and liabilities after adjustments.

Q5. Who prepares the Trial Balance in an organization?A Trial Balance is typically prepared by accountants or bookkeepers before final accounts are drawn up, ensuring all ledgers are balanced and updated.

Q6. Does the Trial Balance detect all types of errors?No. It detects arithmetic errors but cannot catch mistakes like omitted transactions, wrong account classification, or errors of principle.

Q7. What accounting software is commonly used for Trial Balance preparation in India?Popular software includes Tally, Zoho Books, and QuickBooks. These tools help automate ledger postings and generate Trial Balances quickly and accurately.