As one of the core accounting tools, a ledger records each financial transaction of a business. From every small startup to larger corporations, businesses require ledgers to keep track of income, expenses, assets, and liabilities. Record-making paves a clear and orderly path for the financial activities of a company, thereby assisting in the preparation of reports, in setting performance targets, and other activities aimed at ensuring a correct keeping of books.

Knowing what a ledger is or how to create a ledger in Tally is very important for managing financial entities well.

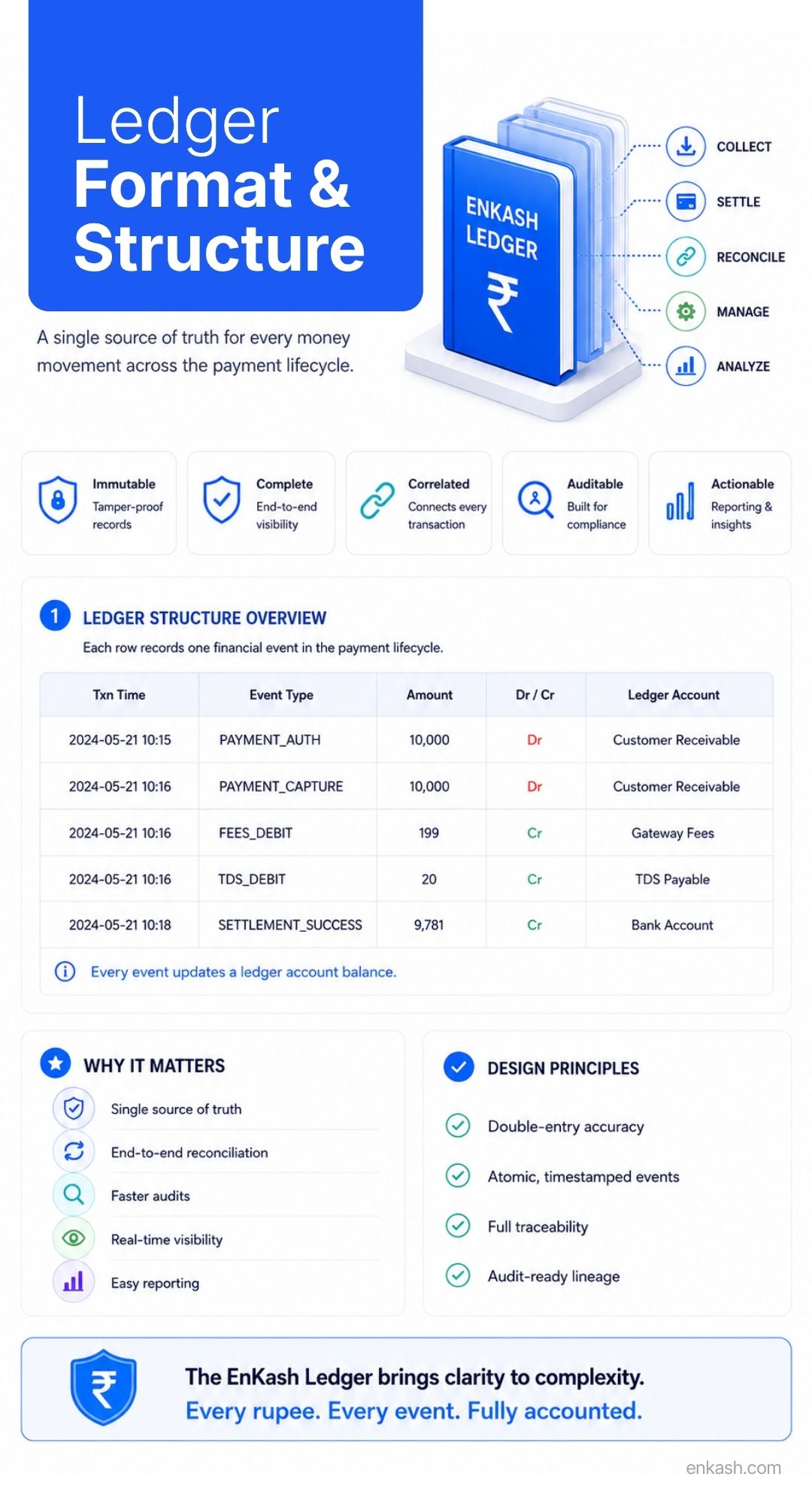

What is Ledger?

The ledger is the chief book of accounts wherein the various business transactions are entered systematically after being classified under different heads. There are separate accounts for sales, purchases, expenses, assets, liabilities, and revenues, making analysis and monitoring easier while maintaining a clear financial record. The general ledger is the complete record showing the financial position of a business at any moment in time.

Digital accounting software such as Tally has made ledger maintenance smoother since transactions get automatically recorded, arranged, and updated. This allows efficient accuracy, transparency, and a high level of ease in grabbing any financial information for making quick decisions or reporting.

What are the key components of a Ledger?

Transaction Details: A ledger has date, account name and description of the transaction.

Running Balance: The updated total of the account after the transaction is posted.

Double entry Accounting: A bookkeeping method where every financial transaction is recorded in at least two accounts as equal and opposite entries.

Chart of Accounts: An index of all financial accounts in a company's general ledger to categorise assets, liabilities, equity, revenue, and expenses.

Types of Ledger Accounts in Accounting

In accounting, ledger accounts provide an organized manner of recording financial transactions to track business performance. Depending upon the nature of transactions, ledger accounts are categorized into:

1. General Ledger

This ledger is truly a master record of all financial accounts in one place. Every transaction about assets, liabilities, equity, income, and expenses is maintained in this ledger. Accounting is founded on it as the source from which the financial statements, like Balance Sheet and Income Statements, are drawn up. In computerized accounting systems such as Tally, the General Ledger gets automatically updated, thereby saving time and eliminating errors.

2. Sales Ledger

Sales Ledger records all sales transactions of the business, whether they are made for cash or on credit. It has individual customer accounts showing how much these customers owe, how much they paid, and what balance is outstanding. By controlling the sales ledger, the company controls its credit sales and chases the pending payments.

3. Purchase Ledger

The Purchase Ledger keeps a detailed record of all the goods and services the business has purchased. Supplier names, amounts payable, and payment history are recorded in this ledger. These ledgers are employed in managing payables so that suppliers are paid on time, thereby avoiding unnecessary late fees or disputes.

4. Cash Ledger

The Cash Ledger records cash inflows and outflows. These are cash transactions like sales, purchases, withdrawals, and deposits. In regular cash ledger monitoring, keeping liquidity healthy will ensure that the business does not fall short on cash for operational requirements.

Two-Sided Structure for Clear Recording

The ledger normally has two sides: the left is the Debit (Dr) side and the right is the Credit (Cr) side. This is done to make every transaction entry precise so that both debit and credit amounts can be tracked properly.

Date for Reference: Proper Ledger Entries

This contains the date of the business transaction. Chronological tracking of business activities becomes simpler, making a matching of an entry with some receipt, invoice, or bank statement also possible when needed.

Description for Transaction Details

The description column in the ledger displays the particulars of the nature of the transaction. Payment could be to a supplier, income from sales, salary payments, or so on-the-greater the description, the more transparent the transaction, and thus simpler for auditing.

Reference Number for Easy Tracking

Each entry has to be furnished with a reference number that can be linked to a supporting document, like an invoice or payment voucher. This ensures that whenever any dispute arises, every transaction can be checked easily.

Proper Entry of Amounts

The most important aspect of a ledger is the amount entered into the Debit or Credit column. This must be accurate because an error of even one unit may cause a serious financial misstatement.

Design for Accuracy and Clarity

The structured design of the ledger aims at clarity and accuracy in transaction tracking. Maintaining the consistency of recording entries in a ledger avoids confusion; thus, businesses maintain reliable financial data for decision-making.

General Ledger and Its Functions

An account ledger is the primary set of accounting books containing all of the business's financial transactions, duly indexed by accounts. It is, therefore, the hub for storing summarized data extracted from sub-ledgers such as sales, purchase, and cash books. Thus, the general ledger keeps records of larger entries with their date, name or description, reference number, and credits and/or debits.

The general ledger becomes a fundamental document while preparing the financial statements, mainly the balance sheet and the income statement, which enhances financial accuracy and transparency. It tells everything about a company's financial position for any given period. The General Ledger is a vital part of financial management and has the following aspects:

1. Maintains a Complete Record of Financial Transactions

The general ledger maintains the record of all financial transactions done by the business; nothing is excluded. In effect, it acts as a single point of reference for all financial operations carried on within the enterprise.

2. Helps to Detect Errors in Recording

Occasionally, the general ledger may be checked for discrepancies, errors in posting, or omission of any transaction. Discovering any such error early will prevent it from turning into larger errors in the accounts later on.

3. Facilitates Audit and Tax Filing

If the ledger is maintained properly, an auditor is blessed with a very easy task since they can view all transactions. It also provides ease with tax filing, since the records for income, expenses, and so on are kept correct and up-to-date.

Ledger Posting Process

Ledger posting is the systematic procedure of transferring data from journals to the ledger. It is very important for accounting, given the fact that it enables the classification of all transactions, thus easing the preparation of trial balances and final accounts. Let us have a look at the details of how the posting procedure is carried out.

Understanding the Purpose of Ledger Posting

Ledger posting is the procedure of transferring information from the journal to the ledger in an organized fashion. Ledger entries present transactions into categories like Cash, Sales, Purchases, or Expenses, so that ledger analysis can evaluate the aggregate effect of transactions.

Identifying Debit and Credit Accounts

Before the actual posting, it is important to ascertain from the journal entry which accounts are to be debited and which are to be credited. Every debit must equal a credit by the double-entry system of accounting. This shall ensure that the accounting equation stays balanced and becomes accurate.

Posting to the Ledger

On deciding on the accounts, the amounts on the debit are posted to the Dr. side of the ledger account concerned and the credit on the Cr. side. Hence,a brief narration should be added to each entry if the entry itself is not completely explanatory.

The ledger account may be presented in the "T" format or tabular form, with separate columns for debit, credit, and balance. Any one uniform format is to be followed; uniformity is necessary for easy interpretation of data and avoiding confusion, ensuring professional standards in bookkeeping.

Updating Balances After Every Entry

The balance of an account is to be updated immediately after each posting. This running balance assists in knowing the current standing of the account without having to recalculate it from the beginning each time.

Cross-Referencing with Journal Entries

Another thing that should always be used is a cross-reference, such as a journal page number or voucher particulars, so an auditor can trace back the ledger posting via the journal entry. Such cross-references help an auditor to check the entries in a hurry and to eliminate any discrepancies.

Avoiding Posting Errors

Errors of various types result in the distortion of financial records. These errors may include incorrect amounts, erroneous accounts, or the omission of transactions. These can be avoided by conscientious effort, systematic checking, and strict adherence to the original journal data.

Periodic Ledger Review

At the end of each account period, every ledger account should be reviewed to confirm that all postings are by the journal entry made. This is necessary so that an accurate trial balance may be cast and, eventually, reliable financial statements prepared.

Ledger Journal Entries

A journal entry is the first recording of a financial transaction before its transfer to the ledger. It records the necessary details of the transaction in some manner so that there is always documentary evidence of all financial transactions.

Purpose of Journal Entries

A ledger journal entry is the very first recording of any financial transaction before it is posted into the ledger. The primary objective of journal entries is to maintain a chronological record of each transaction to facilitate full traceability; these entries are the basis for ledger posting, enabling accountants to keep track of the movement of money and maintain precise financial records.

Key Parts of a Journal Entry

Each journal entry must carry enough details to describe the nature of the transaction in question,

Date: The date the transaction happened is a part of the journal entry.

Account Involved: The account names from the chart of accounts.

Debit and Credit Amounts: The values for each account.

Description: A short explanation as to why the transaction occurred.

Reference Number: A unique ID to track and audit the transaction

Types of Journal Entries

Accounting entries are of several types.

Simple Entry: A simple journal entry would have one debit and one credit.

Compound Entry: A compound journal entry has several debit or credit accounts in a single transaction.

Opening Entry: Opening journal entries are made at the start of a financial year to record opening balances.

Procedure for Entering a Journal

Journal entry preparation is, by sequence of operations, an enumerated one: The first step is identifying the transaction from source documents—the invoices or receipts. Next is to determine what accounts are affected, one of which must be debited and the other credited; then one marks the date, the names of the accounts, the amount, and an explanatory narration in the journal.

Double-Entry Accounting System

Every transaction recorded in the journal is a two-sided transaction. An equal debit and credit amount must be entered throughout the journal entry. This fundamental principle balances the equation and ensures that the recorded transactions give a true reflection of the financial position of the company.

A Simple Example of a Journal Entry

For example, if a company buys goods worth ₹5,000 in cash, the Purchases Account will be debited by ₹5,000, and the Cash Account will be credited by ₹5,000. This depicts the movement of cash and goods.

Importance of Making the Right Journal Entries

Journal entries should be made right, for if a wrong entry is made here, it will be carried down into the ledgers and financial statements, where it could manifest into incorrect reporting. It is thus a good habit to verify an entry before it gets posted.

Relationship Between Journal and Ledger

The journal records each transaction in chronological order, whereas the ledger places transactions under specific accounts. Without accurate and timely journal entries, ledger posting would never be successfully done; hence, it forms a crucial link in accounting.

What is Ledger Balance?

The ledger balance generally is the closing amount after all transactions for a given period have been recorded in the ledger. Simply put, it is the real figure available in the account after recording all the deposits, withdrawals, and adjustments. From the viewpoint of banking, the ledger balance in a bank account is the balance at the end of the previous business day after all cleared transactions. It differs from the available balance, which reflects pending deposits or withdrawals yet to be cleared. Thus, managing cash flow becomes the foremost function of the ledger balance.

Importance of Ledger Balance

Avoid unnecessary fees: A ledger balance helps you track cleared funds so you do not get overdraft charges or bounced checks.

Defining business budgets: The balance acts as a starting point for daily or monthly personal and business budgets.

Payment tracking: It confirms which payments are cleared and which are pending.

Facilitates statements: The ledger balance forms the foundation for creating trial balances, profit &

loss statements, and balance sheets.

Keeps records: It keeps a secure record of revenue, assets, and expenses for tax and legal compliance.

Trading details: It showcases exact cash components available for investments.

Creating a Ledger in Tally

Setting up a ledger in Tally is simple but requires precision in order to have proper recording of financial details. Here's a stepwise approach for creating one:

Open Tally and Navigate to Ledger Creation

Start the Tally software. Enter Gateway of Tally → Accounts Info → Ledgers → Create from the main menu. This option opens the ledger creation screen on which you enter the required details.

Enter the Ledger Name

Enter a desired name in the field for Ledger “Name.” It is preferable to keep the name clear and self-explanatory to identify the ledger at a later point. Instances are “Sales Account,” “Purchase Account,” or “Cash in Hand.”

Select the Appropriate Group

Each ledger in Tally must be put into a particular group. Choose the group that best represents the nature of the ledger, such as “Sundry Debtors” for customer accounts or “Sundry Creditors” for supplier accounts. This classification directly affects the reports in your income statement and balance sheet. So choose wisely.

Fill in the Necessary Details

Enter the opening balance, mailing name, address, and contact details (if any). You can also specify tax details, currency, and cost-center allocations, wherever necessary, following your accounting rules.

Saving the Ledger

Once all fields have been filled in, press Enter to save the ledger. The ledgers will now be displayed by Tally, allowing transactions to be recorded immediately.

Practices for Accurate Ledger Posting

Double Check Every Entry Before Posting in Ledger

Before entering a transaction into the ledger, it is important to go through the data very carefully. The amount, date, and description should all be checked. Even simple errors like wrong figures or an erroneous account can cause huge discrepancies in the financial reporting.

Follow Proper Ledger Format for Clarity

Using a standard and consistent ledger format increases the ease of reading, reviewing, and auditing the respective records. Ensure the debit and credit columns are clearly labeled, and there are appropriate headings for each ledger account. This eliminates confusion and allows quicker interpretation of data.

Update Ledger Accounts Regularly to Prevent Discrepancies

Never wait till the end of the month to update your ledger. Posting of transactions should always be regular, daily, or weekly, so the records are current. With the records current, better decision-making is guaranteed. Errors, if any, can be detected and corrected promptly.

Keep Backup Copies of Your General Digital Ledger

Never forget to keep backup copies of your ledger, whether manual or digital. If digital, then keep on backing it up on hard devices or on the cloud. This will keep your financial data from being lost due to accidental deletion, a technical failure, or even a cyber attack.

Conclusion

A ledger is one of the most important books in accounting because it helps organize and classify all financial transactions into separate accounts. It is difficult to prepare financial reports and manage business finances without a ledger. The ledger groups the transactions account-wise, making it easier to track balances, prepare financial statements, and understand the overall financial position of a business.

FAQs

1. What is a ledger in accounting?

A ledger is book of accounts that contains all business transactions classified under different accounts such as cash, sales, purchases, assets, liabilities, income, and expenses.

2. What is the purpose of a ledger?

The main purpose of a ledger is to organize journal entries account-wise, determine account balances, and provide the information required to prepare financial statements.

3. What is the difference between a journal and a ledger?

A journal records transactions in chronological order, while a ledger records them account-wise. Transactions are first entered in the journal and then posted to the ledger.

4. What are the main types of ledgers?

The three primary types of ledgers are:

5. Why is the ledger important in accounting?

A ledger helps businesses:

Track financial transactions accurately

Determine account balances

Prepare trial balances and financial statements

Detect errors and discrepancies

Support auditing and compliance requirements

6. What does a ledger contain?

A ledger typically includes:

7. Can a business maintain a ledger digitally?

Yes. Most modern businesses use accounting software to maintain digital ledgers, which automate posting, improve accuracy, and provide real-time financial insights.

8. What is a General Ledger (GL)?

A master record of all financial accounts of a business is called a General Ledger. It has information related to assets, liabilities, equity, revenue, and expenses.

9. Is a ledger needed for small businesses?

Yes. Business irrespective of their size need to maintain a ledger for tracking finances, filing taxes, managing cash flow, and making informed business decisions.

10. What happens if ledger records are inaccurate?

In case of inaccurate ledger entries, incorrect financial statements will be created, tax filing will have errors, cash flow issues will be visible, and difficulties arise during audits.