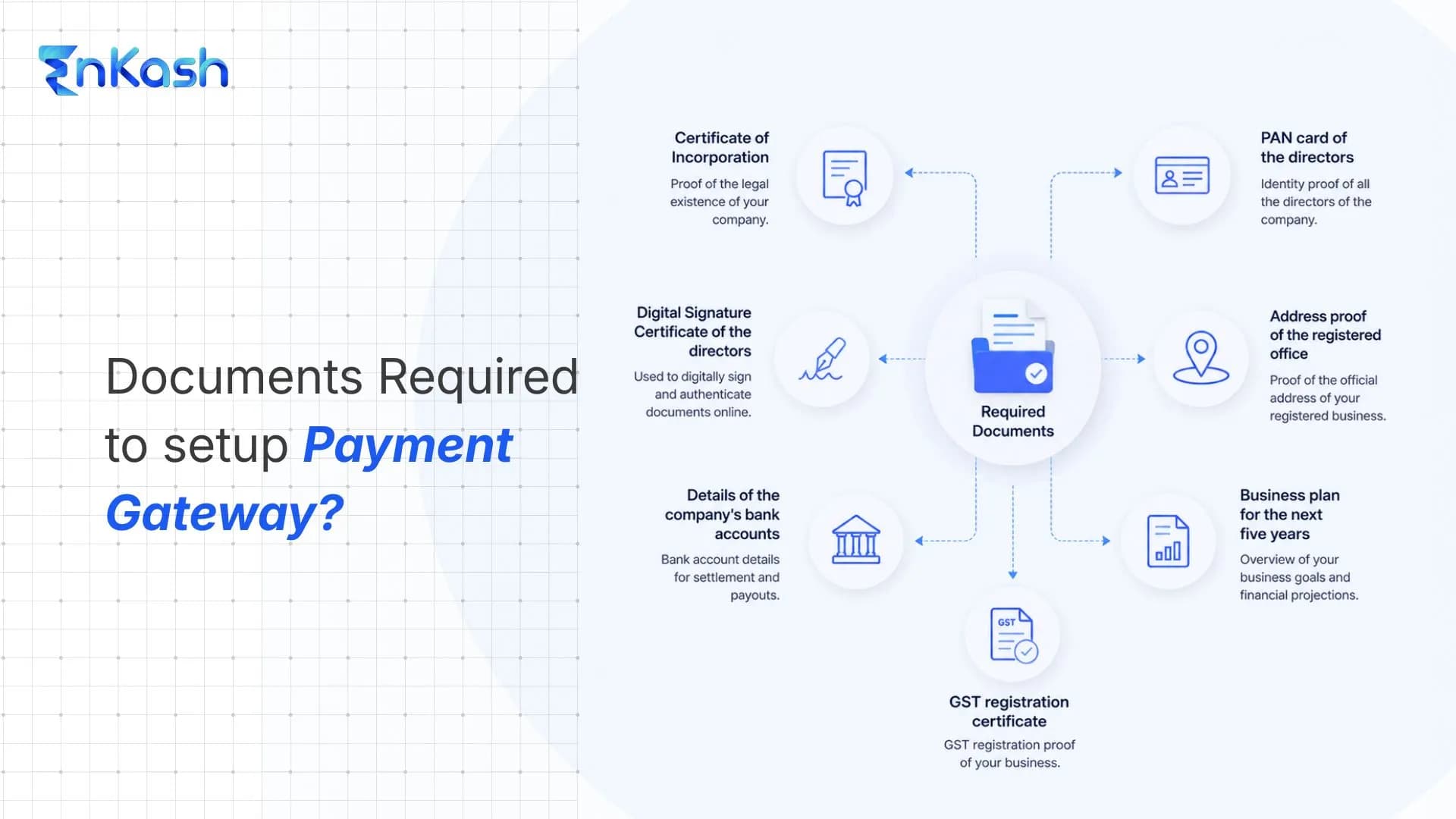

Setting up online payments is more than a technical step. A payment aggregator, acquiring bank, or payment provider must first verify that the applicant is a genuine merchant, that the business can legally collect payments, and that settlements will be credited to the correct account. Documents for payment gateway approval help confirm identity, ownership, business activity, signer authority, and bank linkage before live transactions begin. This protects the merchant, the customer, and the payment provider from avoidable disputes or misuse. As part of payment gateway KYC, providers also review the sales channel, since the website, app, or donation page must reflect a real business purpose. This blog explains the core document requirements by business type, then covers extra records, incomplete paperwork risks, and common onboarding questions. Merchants can use it to understand the paperwork behind approval without sorting through scattered provider checklists.

To set up a payment gateway in India, most businesses need PAN, business registration proof, authorized signatory KYC, settlement bank proof, GST certificate where applicable, website or app details, and customer-facing policies such as refund, cancellation, privacy, and terms pages. The exact document list depends on the business type, provider, risk category, and payment flow.

Documents Required for Payment Gateway in India

Payment gateway documents for onboarding vary depending on the merchant’s legal structure. A company has a different verification process from that of a proprietorship, and an LLP cannot be checked using the same file as a regular partnership firm. Providers review the business identity, signatory authority, settlement account, and live sales channel before approval. Legal name, trade name, PAN,

GST record, bank account, and website footer details should line up clearly. Clean files reduce avoidable back-and-forth during merchant review. Blurred uploads, old records, missing signatures, and mismatched names can slow activation even when the business itself is eligible.

| Entity type | Commonly required documents |

|---|

| Company | - Certificate of Incorporation

- company PAN

- MOA

- AOA

- Board Resolution

- authorized signatory KYC

- bank proof

- GST certificate (where applicable)

|

| Sole proprietorship | - Proprietor PAN

- address proof

- business proof

- bank proof

- GST certificate (where applicable)

- website or app details

|

| LLP | - LLP incorporation certificate

- LLP PAN

- LLP Agreement

- designated partner KYC authorization record

- bank proof

- GST certificate (where applicable)

|

| NGO | - Trust deed

- society registration or Section 8 records

- NGO PAN

- authorized signatory KYC

- bank proof

- 12A or 12AB

- 80G

- FCRA (where applicable)

|

| Partnership | - Partnership deed

- firm PAN

- partner KYC

- authorization letter

- firm bank proof

- GST certificate (where applicable)

|

For Company

A company needs a cleaner paper trail because it operates as a separate legal entity. The payment gateway provider checks whether the company exists, whether its activity is permitted, and whether the person signing the agreement has proper authority.

Documents needed:

- Certificate of Incorporation issued for the registered company.

- Company PAN is linked to the same legal name.

- Memorandum of Association showing permitted business activity

- Articles of Association covering internal company rules

- Board Resolution approving payment gateway onboarding

- An authorization letter naming the approved signatory

- Director or authorized signatory PAN card

- Address proof of the director or authorized signatory

- Registered office address proof of the company

- Company bank account proof for settlement credits

- GST certificate where GST registration applies

- Website or app details connected to sales activity

The Board Resolution needs close attention. It should clearly name the person allowed to sign the payment gateway agreement and manage onboarding communication. If the company has multiple directors, the uploaded authority record should remove any confusion about signer approval.

For Sole Proprietorship

A sole proprietorship needs a different file because the business and owner are closely linked. The provider checks whether the individual applying is connected to the trade name, sales channel, and settlement account.

Documents needed:

- Proprietor PAN card with readable details

- Proprietor's address proof accepted for KYC

- The proprietor’s photograph, when requested by the provider

- Bank proof in the proprietor's or business name

- Udyam Registration Certificate, where available

- Shop and Establishment license, where available

- GST certificate where GST registration applies

- Income tax return as business activity proof

- Import Export Code, where import or export activity is involved

- Professional license for regulated service activity

- Utility bill issued in the business name

- Website or app details connected to the business

This section carries a common risk. A proprietor may use a trade name on the website, another name in the bank account, and the owner’s personal name in PAN records. The file should make that connection easy to verify. Payment gateway KYC becomes smoother when the owner, trade name, and business proof point to the same operating activity.

For LLP

Payment gateway documents required for LLP onboarding include incorporation records and proof of partner or signatory authority. An LLP has a registered legal identity, designated partners, and an agreement that defines how the entity is managed.

Documents needed:

- LLP Certificate of Incorporation issued by MCA

- LLP PAN linked to the registered entity

- LLP Agreement signed by the partners

- Designated partner PAN card for KYC

- Designated partner address proof for verification

- Partner resolution or authorization record approving payment gateway onboarding

- Authorization letter naming the onboarding signatory

- Registered office proof of the LLP

- Principal business place proof, where different

- LLP bank account proof for settlements

- GST certificate where GST registration applies

- Website or app details linked to business activity

The LLP Agreement is important because it helps verify partner roles, management rights, and authority. Providers may request clarity on who controls the merchant account and who can receive communication. Any change in designated partners should be updated before submission.

For NGO

An NGO's file depends on its legal form and donation flow. A trust, society, and Section 8 company usually need different registration proofs. The provider checks the organization, collection purpose, signer authority, and donation page transparency.

Documents needed:

- Trust deed for a registered trust

- Society registration certificate for a society

- Certificate of Incorporation and Section 8 licence for a Section 8 company

- NGO PAN is linked to the registered organization

- 12A or 12AB registration, where applicable

- 80G certificate where donor benefit applies

- List of trustees, members, directors, or office bearers

- Governing body resolution approving onboarding

- Authorized signatory PAN card for KYC

- Authorized signatory address proof for verification

- Bank account proof in the NGO name

- Donation page details explaining the cause, collection purpose, and donor receipt process

- Refund or cancellation policy for donations

- Privacy policy covering donor data handling

- FCRA certificate where foreign contributions apply

- Designated FCRA bank details where applicable

Donation collection needs tighter clarity because the contributor must understand the purpose, receipt flow, refund terms, and data handling. A domestic donation setup should not be mixed with foreign contribution acceptance. Foreign contributions must be handled through the permitted FCRA account route.

For Partnership

A partnership file mainly depends on the deed and partner authority documents. The provider checks whether the firm exists, which partners are tied to it, and who has approval to complete payment gateway activation.

Documents needed:

- Partnership deed signed by all partners

- Partnership firm PAN is linked to the firm name

- Registration certificate where the firm is registered

- PAN cards of all required partners

- Address proofs of all required partners

- Partner-signed authorization letter for onboarding

- Firm address proof for business verification

- Bank proof in the partnership firm name

- GST certificate where GST registration applies

- Website or app details tied to sales activity

The deed should match the current partner details. Older deeds can create review issues when bank, tax, or application records carry updated names. Unregistered firms may need stronger supporting proof, such as tax records, business licenses, invoices, or address evidence. When one partner handles the application, the authorization letter should state that role clearly.

Additional Documents That Payment Gateways May Ask For

Standard entity papers open the review, but some applications need a second layer of checks. These requests depend on business category, settlement setup, website readiness, risk level, and technical integration. Payment gateway onboarding may also move more slowly when the provider needs evidence beyond incorporation or identity records.

Bank Account and Settlement Proof

Settlement proof confirms the account where collected money will be credited after successful transactions. Providers may ask for a cancelled cheque, a recent bank statement, a passbook copy, or a bank verification letter. The account name should match the merchant record or a supported trade name. Any gap between the application name and bank proof can lead to payout review before activation.

GST Certificate or Non-GST Declaration

GST documents help validate the tax record, registered address, trade name, and business category where registration applies. A merchant without

GST registration may need a non-GST declaration, depending on the provider’s onboarding policy. The declaration should match the nature of sales shown on the website, invoice format, and expected transaction flow.

Website, App, and Customer-Facing Policy Pages

A payment page needs enough information for the customer to review before money is collected. Providers may check the About Us page, Contact Us page, pricing details, terms and conditions, privacy policy, refund and cancellation policy, and delivery or service policy. These pages help confirm transparency, customer support access, refund handling, and business continuity. Empty or incomplete pages can trigger manual review

Category Licenses for Regulated Businesses

Some businesses need category-specific proof before approval. A food merchant may need an FSSAI license. A pharmacy-linked seller may need a drug license. Import-export activity may need an IEC. Education, training, financial services, gaming, health, charity, and professional services may need additional proof depending on the exact model. The provider checks whether the merchant can legally sell the product or service being listed.

Security and Integration Declarations

Technical review becomes important when the merchant uses custom checkout, marketplace routing, saved customer data, or a deeper integration. For custom checkout, marketplace routing, saved customer data, or deeper integrations, providers may request declarations linked to PCI-DSS, card data handling, privacy controls, incident response, or secure redirect use. The merchant should avoid storing sensitive card credentials unless the setup is allowed under applicable standards. Payment gateway documents for onboarding can, therefore, include both business records and technical confirmations.

What Happens if Documents Are Insufficient

Incomplete paperwork does not always mean final rejection, but it can interrupt approval, settlement, and live collection. The issue may come from missing records, unreadable uploads, expired documents, wrong entity selection, or details that do not match across forms.

Onboarding Gets Delayed

An application with missing signatures, blurred scans, expired proofs, or incomplete bank details may be moved to manual review. The provider may ask the merchant to upload a clearer copy or submit a fresh authorization record. This delay can hold live activation even after technical integration is ready.

The KYC Submission Can Be Rejected or Sent Back

Rejection can happen when the document does not support the selected business type. For example, a proprietorship application submitted with company papers, an LLP file without the agreement, or an NGO file without registration proof may be returned. Correction may still be possible when the business category is eligible.

Payouts Can Be Put on Hold

Settlements may be paused when bank ownership, signer authority, or business control is unclear. This can affect refunds, supplier payments, inventory movement, and service delivery. Small merchants should treat settlement proof with care because payout interruptions can create working capital pressure.

Payment Features May Stay Limited

Some providers may restrict payment modes, transaction limits, settlement speed, or live collection access until verification is complete. The exact treatment depends on provider policy and merchant risk category. A low-risk merchant with incomplete records may still face temporary controls during review.

Unsupported Categories May Be Declined

Documents cannot solve a business model issue. A merchant dealing in prohibited products, unclear donation purposes, counterfeit goods, misleading claims, or restricted services may be declined even with clean papers. Providers review the business category because customer protection and transaction monitoring continue after approval.

Conclusion

A complete document file helps the payment provider verify the merchant, approve the right payment setup, map settlements correctly, and reduce avoidable review loops. For most businesses, payment gateway onboarding requires identity proof, business registration proof, authorized signatory KYC, bank proof, GST details where applicable, and sales-channel information.

The exact checklist depends on the entity type, provider policy, risk category, and business model. A company, sole proprietorship, LLP, NGO, and partnership firm will not follow the same document path. Businesses should keep records current, readable, and consistent across PAN, GST, bank account, website, and application details.

Clean documentation does not guarantee approval for every business model, but it improves the chance of faster onboarding, fewer corrections, and smoother settlement activation.

FAQs

What are the documents required for a payment gateway in India?Most businesses need PAN, business proof, authorized signatory KYC, bank proof, GST details where applicable, and website or app information. Additional documents may be required based on entity type, risk category, and business model.

What is Payment Gateway KYC?Payment gateway KYC is merchant verification done before live payment collection. It checks identity, business existence, ownership, signer authority, bank account details, sales channel, and risk category before approval.

What documents are needed for payment gateway registration for a company?A company needs its incorporation certificate, company PAN, MOA, AOA, Board Resolution, director or authorized signer KYC, bank proof, GST certificate, where applicable, and website or app details.

What is the payment gateway document required for LLP onboarding?Payment gateway documents required for LLP onboarding include LLP incorporation certificate, LLP PAN, LLP Agreement, designated partner KYC, authorization record, office proof, bank proof, GST details, and website information.

Can a sole proprietor get a payment gateway in India?A sole proprietor can apply with the proprietor's PAN, address proof, bank proof, business activity proof, GST details where applicable, and website or app information linked to the trade activity.

What documents are required for a payment gateway for NGO donations?A Payment gateway for NGO may need trust, society, or Section 8 proof, NGO PAN, authorized signer KYC, bank proof, 80G, 12A or 12AB, and FCRA records, where applicable.

Why do payment gateways ask for refund and privacy policy pages?Payment gateways review these pages to check customer transparency, refund clarity, grievance access, business authenticity, and data handling before allowing payment collection through the merchant website or app.

What happens if payment gateway documents are incomplete?Incomplete documents can delay onboarding, trigger KYC resubmission, pause payouts, restrict payment features, or lead to rejection when the business category is unsupported or the records remain inconsistent.

Is GST mandatory for payment gateway approval in India?GST is required when the merchant is GST-registered. Non-GST merchants may need a declaration that matches the business type, sales channel, invoice practice, and expected payment flow.

Why do payment gateways ask for bank proof?Bank proof confirms the settlement account linked to the merchant application. Providers use cancelled cheques, bank statements, passbook copies, or bank letters to reduce payout and routing errors.