The best travel card in India is the one that matches a company’s travel frequency, destination, spending limits, currency needs, and payment cycle. No single card works equally well for every business.

A corporate travel card or travel payment account helps businesses pay for approved flights, hotels, meals, transport, and other work-related travel costs without relying only on employee reimbursements. Depending on the product, it may work as a prepaid card, corporate credit card, forex card, or centrally billed travel account. A central travel account is usually used for centrally booked travel and may not cover all on-trip employee expenses. These options differ in funding, KYC, liability, foreign exchange charges, and settlement rules.

For a planned trip with a fixed budget, a company may choose a prepaid travel card that limits spending to the loaded amount. A corporate credit card may suit frequent executive travel, where schedule changes, longer hotel stays, or client expenses can increase the final cost.

This guide covers:

- How a travel card works

- Types of business travel cards available in India

- Corporate travel card options from EnKash, HDFC, American Express, ICICI, Axis Bank, and Happay

- Benefits and selection criteria for businesses

- The difference between a travel prepaid card and a credit card

- Costs, controls, liability, and foreign exchange factors

What is a Travel Card?

A travel card is a prepaid payment card designed for domestic or international travel expenses. It allows users to load funds in advance and use the card for purchases, hotel bookings, dining, transportation, and ATM withdrawals during their trip. Travel cards help travellers manage spending, reduce the need to carry cash, and provide a secure payment option while travelling.

A corporate travel card usually works in the following sequence:

- The business creates a travel budget for an employee, team, or trip

- Finance assigns the card and sets permitted spending conditions

- The employee pays for approved travel-related purchases

- The transaction record is sent to the company’s expense or accounting system for review and reconciliation

For example, a consulting firm sending an employee to Bengaluru can allow hotel, meal, and cab payments while disabling payments to unrelated merchant categories. Finance receives a clear record of each payment without waiting for a manual reimbursement claim.

The card processes the payment, but it does not replace an expense policy. The policy defines permitted spending, while the issuer and card platform enforce the available controls.

The legal and operational structure depends on whether the issuer provides the card as a credit facility, prepaid payment instrument, or foreign exchange product. Businesses should verify the program terms before issuing them to employees.

Types of Travel Cards in India

Businesses in India generally choose between prepaid, credit-based, and forex travel cards. Each type uses a different funding method and supports a different travel need.

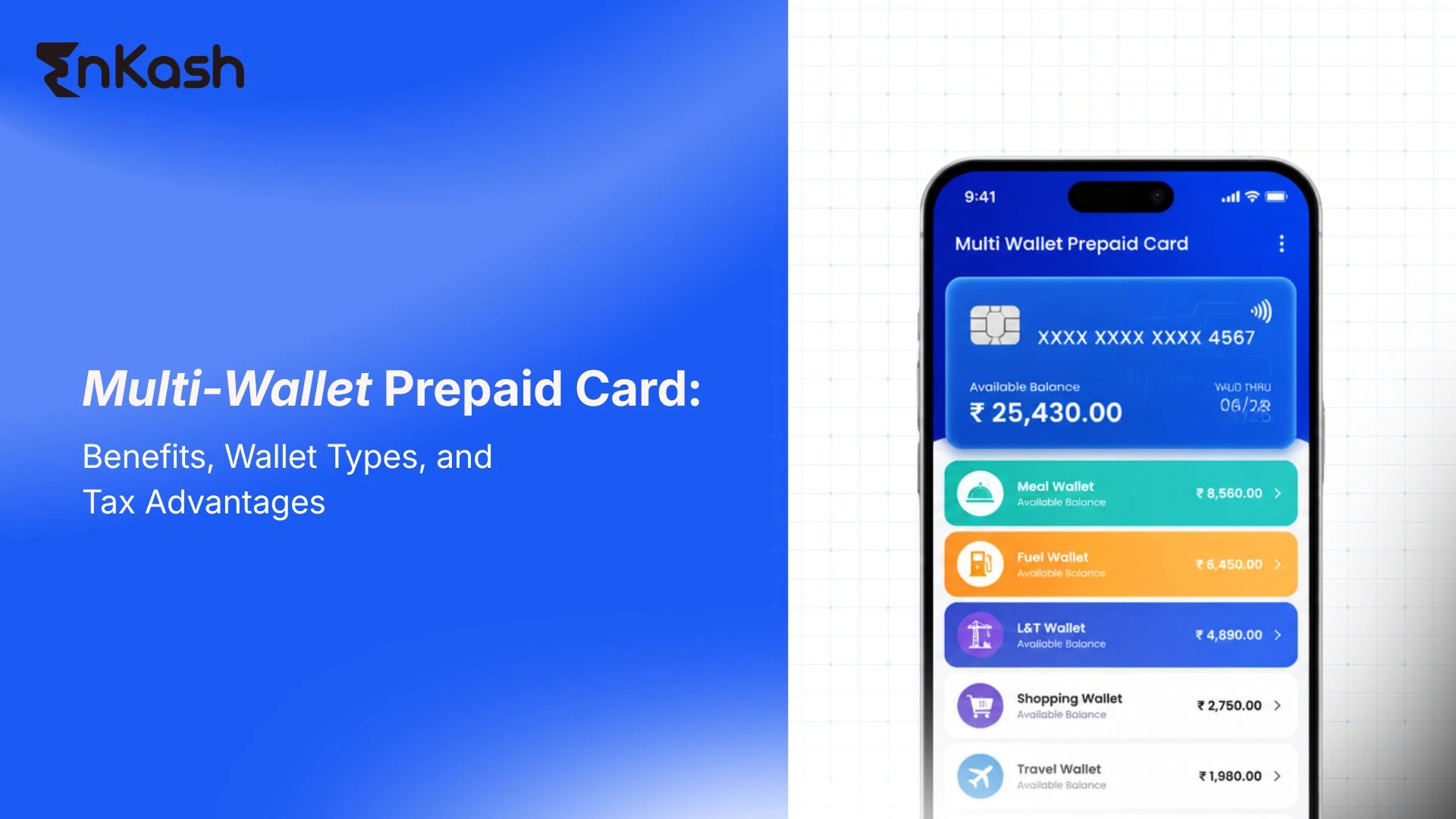

Prepaid Travel Card

A prepaid travel card uses money that the company loads before an employee begins spending. The available balance creates a clear limit, so the employee cannot exceed the approved amount unless finance adds more funds.

This card works well for:

- Trips with a fixed daily allowance

- Employees who travel only a few times a year

- Project teams working away from their usual office

- Businesses that want firm control over trip expenses

For example, a construction company may send five engineers to Hyderabad for a site inspection. Finance can load separate amounts for meals, local transport, and accommodation instead of giving cash advances.

A prepaid card gives the company strong budget control, but it also requires reliable reloading. An employee may face a payment problem if the balance runs low and finance cannot add funds quickly. Businesses must also check whether the card supports international use, since many domestic prepaid cards work only in India.

Travel Credit Card

A travel credit card allows an authorized employee to spend against a credit limit assigned to the company. The business pays the bill after the statement reaches its due date.

This structure suits regular travelers who may face changing costs. A service manager visiting several client locations, for instance, may need to extend a hotel stay or book a new flight at short notice.

Before choosing a travel credit card, the business should verify:

- Who is responsible for the outstanding amount

- How long does the payment window last

- Which spending categories does the card permit

- What fees apply to cash withdrawals and overseas payments

- How the issuer handles disputed or unauthorized transactions

A credit limit offers flexibility, but it does not remove financial risk. Late payment, interest, and weak spending controls can raise the total cost.

Forex Travel Card

A forex travel card may hold one or more foreign currencies, while some international business travel cards may be INR-funded and convert at the time of use. The company converts rupees and loads the selected currency before the employee travels. The card then deducts payments from the balance in the relevant currency.

Suppose an employee travels to Singapore and Japan for supplier meetings. The company can load Singapore dollars and Japanese yen into separate wallets, provided the card supports both currencies. This makes the funded amount easier to plan in rupee terms.

Before selecting a prepaid card for international travel, compare:

- Available currency wallets

- Loading and reloading fees

- ATM withdrawal charges

- Cross-currency conversion costs

- Rules for refunding unused funds

The card may charge a cross-currency fee when the employee pays in a currency that is not loaded. The company must also complete the applicable KYC and foreign exchange documentation before funding the card.

Best Travel Card in India

A useful comparison of the best travel card in India must go beyond product names and advertised benefits. Businesses need a clear view of how each option works, which use case it supports, and which terms require further verification.

| Travel Card | Best Suited For | What Makes It Useful | What the Business Should Verify |

|---|

| EnKash Travel Card | Companies that want to manage cards and travel expenses through one system | Businesses can set limits by amount, category, and currency, monitor transactions, manage approvals, and connect spending data with accounting or enterprise systems | Confirm the card issuer, funding model, international usage, forex charges, insurance, and fees under the selected programme |

| HDFC Travel Card | Established companies that need either corporate credit or a separate forex solution | HDFC offers a corporate credit card with liability options and merchant controls. Its multicurrency ForexPlus Card supports several foreign-currency wallets | Check which HDFC product matches the requirement. The corporate credit card and forex card follow different terms, costs, and eligibility rules |

| Amex Travel Card | Frequent business travellers and senior employees who need travel assistance | American Express offers different corporate card tiers, central programme management, emergency support, and travel-related benefits | Review merchant acceptance, card fees, liability structure, spending conditions, and benefits included with the chosen tier |

| ICICI Corporate Forex Prepaid Card | Companies funding planned overseas travel in several currencies | The card supports multiple currency wallets and allows businesses to load and manage travel funds digitally | Compare loading rates, reload fees, ATM charges, supported currencies, and unused-balance refund rules |

| Axis Bank Central Travel Account | Businesses that book flights through a travel desk or travel agency | The company receives central billing, detailed booking data, and one settlement process for eligible travel purchases | This account mainly supports central bookings. Employees may still need separate cards for meals, hotels, or local transport |

The final choice should follow a written cost comparison. The company must include annual fees, foreign exchange markup, loading charges, cash withdrawal costs, late-payment fees, and card replacement expenses. Promotional rewards should not outweigh poor acceptance, weak controls, or difficult reconciliation.

Benefits of Travel Cards for Businesses

A corporate travel card helps a business control travel costs, protect employees from large personal payments, and create reliable records for finance and audit teams.

Reduces employee out-of-pocket spending: Employees can use approved company funds for flights, hotels, cabs and overseas expenses instead of paying personally and waiting for reimbursement.

Controls expenses before they happen: Finance teams can set limits by amount, merchant category, location or payment type to prevent unapproved travel spending.

Creates clear transaction records: Every card payment captures the date, amount, merchant, and cardholder, making travel expense tracking and audits easier.

Simplifies reconciliation: Travel card data can be matched with receipts, trip IDs, departments, or cost centers, reducing manual entry during month-end closing.

Improves supplier negotiations: Consolidated travel spend data helps procurement teams negotiate better rates with airlines, hotels, and travel partners.

Enables faster misuse response: Admins can block lost cards, reduce limits, or disable selected transactions quickly when suspicious activity is reported.

Improves travel cash-flow control: Prepaid travel cards help companies allocate funds before a trip, while credit-based cards allow payment after the billing cycle.

How Businesses Can Choose the Right Corporate Travel Card

A business should choose a corporate travel card by matching the card program with its travel pattern, approval process, costs, and risk controls.

Review Travel Requirements

Study recent travel data before comparing providers.

- Count domestic and international trips

- Identify frequent and occasional travelers

- Note the average spend on flights, hotels, meals, and transport

- Check how often bookings change

This shows whether the company needs prepaid limits, flexible credit, foreign-currency access, or central billing.

Check Card Controls

The provider should support the controls required by the travel policy.

- Per-transaction and monthly limits

- Merchant-category restrictions

- Online, ATM, and international-use settings

- Instant card blocking

- Separate rules for each employee

Ask for a live demonstration. Marketing pages may list controls without showing how they work.

Compare the Full Cost

Do not judge a card by its annual fee alone.

- Joining and renewal fees

- Foreign exchange markup

- Loading and reloading charges

- ATM and cross-currency fees

- Interest, late payment, and replacement costs

Use expected travel volume to estimate the annual cost.

Review Liability and Compliance

Confirm the legal issuer, KYC process, billing responsibility, and dispute rules.

- Who pays the outstanding amount?

- How quickly must fraud be reported?

- What happens when an employee leaves?

- Does the card support the required countries and currencies?

A fintech platform may manage the card, while a bank or authorized entity issues it.

Test Reporting and Support

Run a pilot before rollout.

- Check transaction data and receipt matching

- Test accounting or ERP integration

- Measure support response time

- Review declined payments, refunds, and reversals

Choose the card only if it reduces manual work and gives timely financial records.

Difference Between a Prepaid Travel Card and a Travel Credit Card

Businesses often compare these two options when deciding how employees should access travel funds. The table below examines the practical differences in funding, spending flexibility, repayment, eligibility, foreign exchange use, and cost.

| Comparison Point | Prepaid Travel Card | Travel Credit Card |

|---|

| Funding | The company adds money before use | The issuer provides a credit limit |

| Spending capacity | The employee can use only the available balance | The employee can spend up to the assigned limit |

| Payment timing | The business pays before the trip | The business settles the bill after the statement |

| Budget control | The loaded amount creates a firm ceiling | Limits allow more room for changing expenses |

| Emergency use | Finance may need to add more money | Available credit can cover approved extra costs |

| Interest | The company does not borrow funds | Interest or late fees may apply if the bill remains unpaid |

| Overseas payments | A forex-enabled card may hold selected currencies | The issuer converts foreign transactions under its exchange-rate terms |

| Eligibility | Usually depends on KYC and programme rules | Often requires a credit assessment and issuer approval |

| Best fit | Planned trips with fixed budgets | Frequent travel with uncertain or changing costs |

Why Businesses Need Corporate Travel Cards

Businesses need corporate travel cards when employee travel can no longer be managed safely through cash advances, personal cards, and delayed reimbursements.

A formal card program becomes necessary when:

- Travel happens across several teams, cities, or countries

- Different departments charge costs to separate budgets

- Managers need faster approval during trip changes

- Finance must identify who spent the money and for which business purpose

- The company needs one payment process across all offices.

With the EnKash travel card, finance teams can manage spending limits, approvals, live transaction visibility, card blocking, and system integrations from a central platform. Because EnKash card programs may follow different issuing and funding arrangements, companies should review the exact program before rollout. This review should cover the issuer, card structure, applicable charges, overseas transaction conditions, and liability terms.

Closing Thoughts

A well-chosen corporate travel card brings structure to every stage of business travel. It should align with the company’s approval process, match how employees actually spend, and keep every transaction easy to trace. When the card program works with internal policies and accounting systems, finance teams gain better visibility without placing extra administrative pressure on travelers.

FAQs

1. Can a small business apply for a corporate travel card?

Yes, but approval depends on the issuer’s eligibility rules. The provider may review the company’s registration, operating history, turnover, financial records, and KYC documents before approving the program.

2. What documents are required for a corporate travel card?

Businesses may need registration proof, PAN details, address proof, financial records, and authorized signatory documents. A forex card application may also require the traveler’s passport, Form A2, and supporting travel documents.

3. Does an employee need a personal bank account?

A personal bank account is not always required. Under a company liability program, the business may settle the card centrally. An individual-liability arrangement may require the employee to provide a personal account for repayment.

4. How long does travel card issuance take?

Issuance time varies by provider and card format. Virtual cards may become available after approval, while physical cards can take several working days. Incomplete KYC or company documents may delay the process.

5. Can the same travel card be used for future trips?

The same cardholder can usually reuse a valid tTravel cCard if the program permits further loading or continued credit access. The company should check card validity, renewal terms, and inactivity charges.

6. Can a travel card be reloaded while the employee is abroad?

Many reloadable prepaid and forex programs allow authorized fund loading during the trip. The business must follow the provider’s process and comply with the applicable foreign exchange limits and documentation requirements.

7. What happens to the unused balance after the trip?

The available amount may remain on the card for another journey or return to an eligible bank account. Refund rates, encashment charges, card validity, and closure rules differ across providers.

8. Can a travel card be used for hotel security deposits?

A card may be accepted for hotel pre-authorization, but the hotel can temporarily block part of the available balance. This hold may reduce the money available for other expenses until the hotel or issuer releases it.

9. Can virtual travel cards pay for online bookings?

A virtual corporate travel card can pay for flights, hotels, and other online bookings when the provider enables online transactions and the merchant accepts the card network. Usage controls may still restrict certain payments.

10. Can several employees share one corporate travel card?

A card issued in an employee’s name should remain with that cardholder. Sharing it can weaken expense ownership and may breach program terms. Separate physical or virtual cards create a clearer record for each traveler.

11. Which corporate travel card is best for a business in India?

There is no single best corporate travel card for every business. A prepaid card may work for fixed-budget trips, a corporate credit card may suit frequent travellers, a forex card may suit overseas travel, and a central travel account may work for centrally booked air travel.