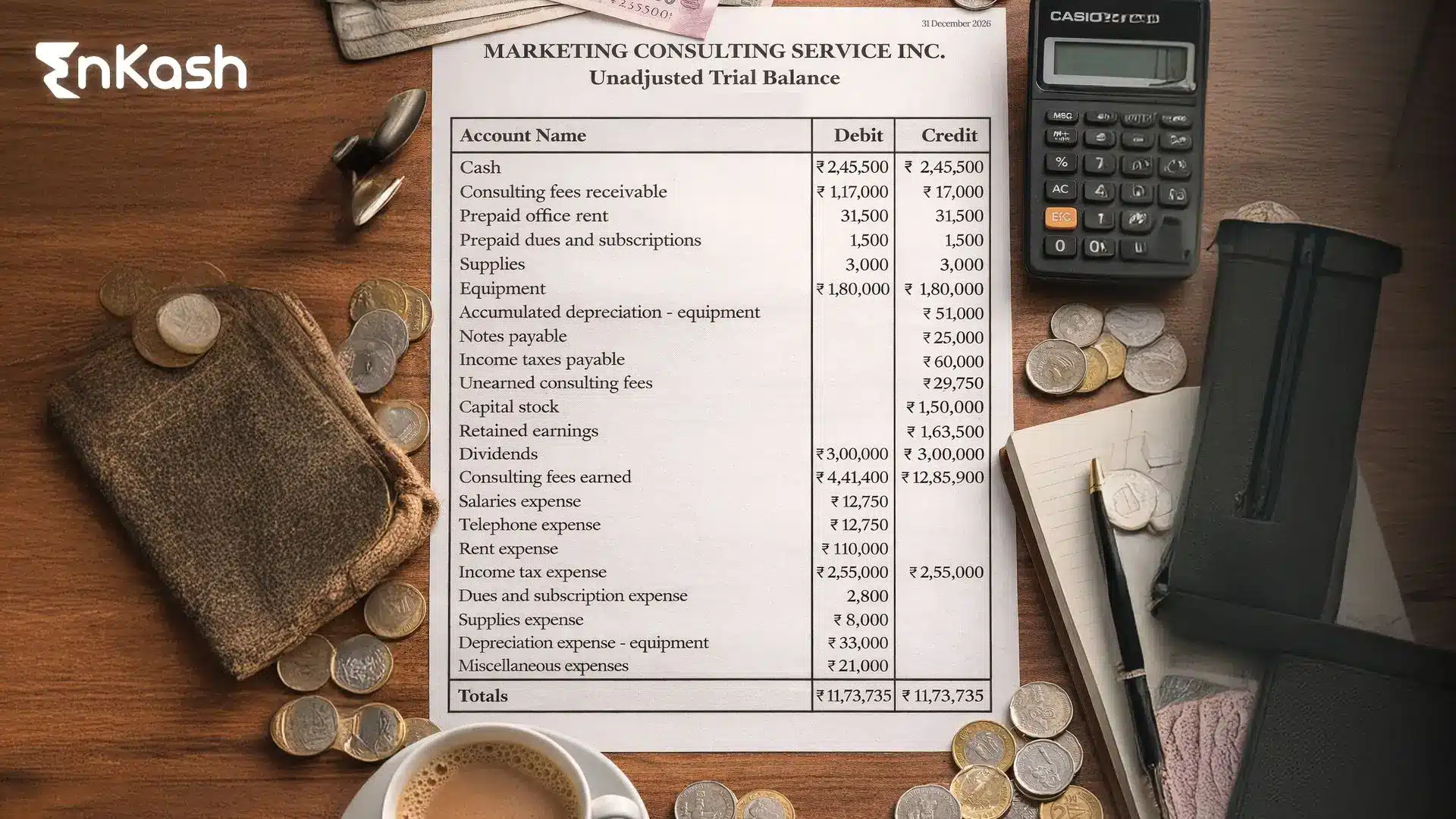

GAAP, or generally accepted accounting principles, forms the base of how financial information is recorded, presented, and reviewed in a structured way. In simple terms, it gives businesses a common method for preparing accounts so that numbers are not reported randomly or interpreted differently every time. When financial reporting follows a recognised framework, it becomes easier for management, investors, lenders, auditors, and regulators to understand what the numbers actually show.

In India, the relevance of GAAP accounting goes far beyond bookkeeping. It supports consistency in financial statements, improves disclosure quality, and helps businesses report their financial position with greater clarity. It also matters for compliance, since companies are expected to follow prescribed accounting policies and presentation requirements while preparing their statements.

For anyone trying to understand the full form, the role of GAAP standards, or the broader meaning of GAAP in the Indian context, the real value lies in one thing: reliable reporting. A strong accounting framework helps businesses present information that can be compared, reviewed, and trusted with greater confidence.

GAAP in India: Legal and Reporting Framework

How GAAP is Understood in India

In India, GAAP is understood as the accounting and reporting framework companies use to prepare financial statements. It is not treated as a separate code with one fixed document. Instead, it works through accounting standards, company law requirements, and prescribed disclosure formats. This is why the meaning of GAAP accounting in India is closely linked to the legal structure that governs how companies recognise, measure, classify, and present financial information.

Role of the Companies Act in Financial Reporting

The Indian reporting framework draws heavily on the Companies Act, 2013. This law sets the foundation for how companies prepare and present their financial statements. It requires financial statements to give a true and fair view of the company’s affairs. It also connects financial reporting with the accounting standards that are formally notified for use. In practical terms, this means companies cannot prepare accounts casually or choose reporting methods without reference to the required framework.

Significance of Notified Accounting Standards

A major part of Indian GAAP standards comes from accounting standards notified under the legal framework. These standards provide structure for key areas such as inventory valuation, revenue recognition, employee benefits, fixed assets, provisions, and disclosures. Their purpose is to reduce inconsistency and support uniform treatment of similar transactions across businesses. Without such standards, financial reporting would depend too heavily on internal preferences, thereby weakening comparability.

How Presentation Requirements Improve Reporting Clarity

Financial reporting in India is also shaped by prescribed presentation rules, including the format in which balance sheets, profit and loss accounts, and related disclosures are shown. This matters because reporting is not only about getting the numbers right. It is also about presenting them in a way that users can review properly. A structured format improves clarity and allows financial statements to be read with greater consistency.

Institutions that Govern the Reporting Framework

The Indian reporting environment involves multiple institutions. The Institute of Chartered Accountants of India plays a key role in developing and recommending accounting standards. The Ministry of Corporate Affairs notifies those standards for legal use. Oversight and enforcement functions are also supported by regulators such as NFRA, while listed entities may also be subject to additional reporting requirements set by SEBI. Together, these institutions help maintain discipline in financial reporting.

Practical Distinction Between Indian GAAP and IND AS

The term Indian GAAP is still used widely in business discussions, but it must be understood carefully. In practice, Indian entities may follow traditional Accounting Standards or IND AS, depending on their category and legal applicability. That is why GAAP in India is best understood as a structured reporting environment rather than a single uniform standard book for every entity.

Read more: Comparative Balance Sheet: Formula, Format, and Business Insights

Core Accounting Principles That Support GAAP

Transactions are Recorded When the Business Event Actually Happens

Under GAAP, a transaction is recognised when the related business activity takes place, rather than when cash is received or paid. This approach gives a clearer view of income earned, expenses incurred, and obligations created during a reporting period. If a company completes a service in March and receives payment in April, the income belongs to March because the service was delivered then. This method improves the reliability of financial reporting and helps users understand real business performance.

The Same Accounting Methods Should be Used Across Reporting Periods

A business is expected to apply the same accounting methods from one reporting period to the next unless a valid and disclosed reason requires a change. This makes financial statements easier to compare over time. If inventory, depreciation, or expense recognition is handled each year differently without a proper basis, the reported numbers become harder to interpret. Consistent application supports clarity and gives analysts, lenders, and management a stronger basis for reviewing trends.

Caution is Necessary When There Is Uncertainty

Financial reporting should avoid inflating income, asset values, or financial strength when the outcome is uncertain. At the same time, expected expenses, losses, or liabilities should not be ignored when reliable evidence points to a possible obligation. This principle encourages balanced reporting in the face of uncertainty. It reduces the risk of accounts presenting an overly positive position and helps financial statements remain grounded in reasonable judgment.

Financial Statements are Usually Prepared on the Basis of Continuing Operations

Accounts are generally prepared on the assumption that the business will continue operating in the foreseeable future. This assumption affects how assets are valued, how liabilities are classified, and how the overall statements are prepared. A company that is expected to continue business uses normal reporting treatment. A company facing closure or a serious operational breakdown may need a different basis of preparation. This principle supports proper valuation and presentation in regular reporting.

Financial statements should give clear attention to information that can influence users' decisions. Some items are significant because they affect how performance, financial position, or risk is understood. Other items may be too minor to change the overall picture. This principle helps decide what deserves separate disclosure, what requires explanation, and what may be grouped without weakening understanding. Relevance is important because users depend on financial statements to make informed judgments.

Accounting Should Reflect the Real Business Effect of a Transaction

A transaction should be reported according to its actual economic effect rather than only its legal wording or outer structure. Documents may describe an arrangement in a certain way, yet the business impact may point to a different accounting treatment. GAAP accounting is strengthened when reporting reflects commercial reality accurately. This helps prevent misleading presentations and improves the usefulness of financial statements for analysis and review.

Financial Statements Should Include Enough Detail for Proper Interpretation

The main financial statements do not, by themselves, convey the full meaning of the reported numbers. Notes, accounting policies, estimates, assumptions, and related explanations are also important for interpretation. Without this supporting context, even correct figures may be misunderstood. Proper disclosure helps users understand how the numbers were prepared, what judgments were applied, and where uncertainty may exist. This improves transparency and strengthens trust in the reporting process.

Compliance With GAAP

Identifying the Reporting Framework that Applies

Compliance with GAAP begins with a basic but important step. A business must first identify the accounting framework that legally applies to its financial reporting. In India, companies do not all follow a single reporting track in the same way. Depending on their category and applicability requirements, they may prepare accounts under Accounting Standards or IND AS. This decision affects recognition, measurement, disclosure, and presentation across the full set of financial statements.

Applying Notified Standards in a Consistent Manner

Once the correct framework is identified, the company must apply the relevant accounting standards consistently while preparing its accounts. Under the Companies Act, financial statements are required to comply with the accounting standards notified under Section 133. That requirement provides GAAP accounting with a formal compliance framework in India, rather than leaving reporting treatment to internal preference. Consistent application also improves comparability across periods and reduces the risk of distorted reporting caused by frequent method changes.

Compliance is not limited to recording transactions correctly. The final financial statements must also be prepared in the form prescribed for the relevant class of company. Section 129 states that financial statements must give a true and fair view, comply with notified accounting standards, and follow the forms provided in Schedule III. This means presentation, classification, and supporting notes are part of compliance, not an optional formatting exercise done at the end.

Supporting Reported Numbers With Disclosures and Records

Strong GAAP compliance also depends on documentation. Reported numbers should be supported by accounting policies, working papers, assumptions, estimates, reconciliations, and explanatory notes where required. A financial statement without proper backup may appear complete on the surface, yet still fail under audit or regulatory review. Clear records help explain how transactions were treated, why judgments were made, and whether the disclosures accurately reflect the underlying facts. This is important because financial reporting is tested through evidence, not presentation alone.

Reviewing Updates and Correcting Non-Compliance Where Needed

Compliance is an ongoing exercise rather than a one-time filing task. Businesses need to monitor amendments, updated rules, and reporting changes issued by the relevant authorities. Indian company law also provides a route for revising financial statements in certain cases where earlier statements do not comply with Section 129 or Section 134, subject to the prescribed process. That makes periodic review important for finance teams, boards, and auditors responsible for maintaining accurate and compliant reporting.

Difference Between GAAP and IFRS

Shared Purpose in Financial Reporting

Both GAAP and IFRS are accounting frameworks used to prepare financial statements in a structured and comparable manner. Their common purpose is to improve the quality of financial reporting and help users understand a company’s financial position, performance, and cash flows with greater clarity. IFRS is developed by the International Accounting Standards Board under the IFRS Foundation and is used across many jurisdictions worldwide.

Variation in Reporting Philosophy and Application

A common distinction is that GAAP frameworks are generally described as more rule-oriented, while IFRS is viewed as more principle-driven in application. That difference affects how transactions may be interpreted in areas where judgment plays a larger role. Under a rule-oriented environment, reporting treatment may rely more heavily on detailed guidance. Under a principle-led environment, professional judgment may carry greater weight when applying the broader reporting requirement to a specific transaction. This difference matters because similar business events may be analysed through slightly different reporting logic.

Differences in Measurement, Presentation, and Disclosure

Differences between GAAP and IFRS can also appear in measurement methods, presentation choices, and disclosure depth. Certain frameworks may place different emphasis on historical cost, fair value, classification rules, or the level of disclosure expected in the notes to accounts. These differences do not mean one framework is casual and the other is strict. The real point is that financial reporting outcomes can vary because the standards and their application methods differ across frameworks.

IND AS Brings the Comparison Closer to the Indian Context

For Indian businesses, the comparison becomes more practical when viewed through IND AS. ICAI guidance explains that India chose convergence rather than the direct adoption of IFRS, meaning IND AS is broadly aligned with IFRS but includes carve-outs and carve-ins suited to the Indian environment. ICAI material also states that IND AS is named and numbered in line with the corresponding IFRS standards. This is why Indian reporting discussions frequently move from GAAP vs IFRS to Indian GAAP vs IND AS in real-world use.

Applicability Matters More Than Broad Comparison

A broad comparison between GAAP and IFRS can help explain differences in accounting philosophy and reporting treatment. However, Indian companies must assess the framework that actually applies to them under Indian law and regulatory requirements. That is the point where the discussion becomes operational. A business preparing financial statements in India must first determine whether it falls under Accounting Standards or IND AS, because compliance depends on applicability rather than on a general international comparison alone.

GAAP Standards in India and Their Applicability

GAAP Standards Give Structure to Accounting Treatment

GAAP standards are formal accounting requirements that guide how financial information is recognised, measured, classified, and disclosed. Principles explain the broader logic of reporting, while standards deal with the treatment of specific transactions such as inventory, depreciation, revenue, employee benefits, provisions, and foreign exchange items.

India Follows Recognised Accounting Frameworks Under Law

In India, accounting standards operate within the legal framework of the Companies Act, 2013. Section 133 provides for accounting standards to be prescribed, which means reporting treatment must follow the applicable standards notified for use.

The AS and IND AS Frameworks Apply in Different Cases

India uses two broad accounting frameworks. The traditional AS framework covers standards such as AS 1, AS 2, AS 3, AS 10, AS 15, and AS 29. The IND AS framework applies to specified classes of companies and includes standards such as IND AS 1, IND AS 2, IND AS 7, IND AS 16, IND AS 109, and IND AS 115. Applicability depends on the entity’s category, size, and legal reporting requirements.

What are Non-GAAP Measures?

Non-GAAP measures are financial metrics that fall outside the formal GAAP framework. Companies create them to present performance in a way that management believes gives added business insight. Common examples include adjusted profit, adjusted EBITDA, or earnings before certain one-time or non-operating items. These figures can help users examine operating trends without the effect of unusual transactions, accounting adjustments, or non-recurring charges.

At the same time, non-GAAP measures need careful reading. Because they are not defined under standard accounting rules, companies may calculate them differently. That reduces comparability across businesses and reporting periods. For this reason, non-GAAP measures should be read alongside GAAP-based financial statements, not in place of them. Their value lies in added interpretation, while the primary reporting base must still come from recognised accounting standards and required disclosures.

Read more: What is an Income Statement? Preparation Guide and Types of Income Statement

Limitations of GAAP

Reporting Still Depends on Judgment and Estimates

GAAP provides structure, yet many accounting outcomes still depend on estimates and judgment. Areas such as impairment, provisions, valuation inputs, and useful life assessment can produce different results even within an accepted framework.

Recorded Values may not Match Present Economic Reality

In many cases, reported figures are based on earlier transaction values rather than current market realities. This can reduce how closely financial statements reflect present economic conditions, replacement value, or updated business risk.

Applying Standards can be Resource Intensive

Applying accounting standards correctly requires documentation, technical understanding, and regular review of changes. For smaller businesses, this can increase the compliance burden and make reporting more difficult to manage.

GAAP improves consistency across reporting, but it does not guarantee identical outcomes. Different judgments, accounting choices, and business models can still lead to variation in reported figures.

Conclusion

GAAP remains fundamental to financial reporting because it turns accounting into a disciplined system rather than a set of internal choices. Within the Indian framework, that discipline matters at every level, from recognition and measurement to disclosure, presentation, and compliance. It helps businesses report financial performance with consistency, explain their position with greater precision, and build confidence among auditors, lenders, investors, and regulators. This is what gives the framework lasting relevance.

A strong understanding of generally accepted accounting principles helps businesses move beyond routine bookkeeping and approach reporting with greater accuracy and accountability. It also becomes easier to interpret standards, disclosures, and reporting obligations in the right context. For any organisation preparing financial statements, a working knowledge of the GAAP Standards List is directly linked to reporting quality, compliance strength, and the credibility of every number presented.

FAQs

1. Why do lenders pay close attention to accounting frameworks before approving credit?Lenders rely on structured financial statements to assess repayment capacity, leverage, cash flow stability, and working capital discipline. A recognised accounting framework improves confidence that revenue, expenses, assets, and liabilities have been recorded using accepted methods, which makes financial ratios and credit evaluation more dependable.

2. How do accounting frameworks improve audit quality?Audits become stronger when financial statements are prepared using recognised standards and supported by documented policies, estimates, and disclosures. A structured framework gives auditors clear benchmarks for testing recognition, measurement, classification, and presentation, which improves review quality and reduces ambiguity during verification.

3. Why can two profitable businesses still report very different financial results?Reported profit can differ because businesses may operate under different accounting frameworks, apply different judgments, or face different disclosure requirements. Estimates linked to depreciation, provisions, deferred tax, impairment, or revenue timing can materially affect outcomes even when commercial performance appears similar on the surface.

4. What makes accounting estimates important in financial reporting?Accounting estimates affect figures that cannot be measured with exact certainty at the reporting date. Items such as doubtful debts, asset useful life, warranty obligations, and impairment require professional assessment. These estimates influence profit, asset values, liabilities, and disclosures, which makes them important for accurate interpretation.

5. Why are notes to accounts important for understanding financial statements?The main statements present the headline numbers, but notes explain the accounting policies, assumptions, contingencies, commitments, related party items, and estimation basis behind those figures. Without that supporting detail, users may read the numbers incorrectly or miss risks that materially affect financial interpretation and decision-making.

6. How do accounting frameworks help investors compare companies across periods?A structured framework reduces inconsistency in how transactions are recorded and presented from year to year. That improves trend analysis, ratio comparison, and performance review. Investors can examine changes in revenue, margins, liabilities, and cash flows with greater confidence when reporting treatment follows recognised standards consistently.

7. Why does revenue timing matter in financial reporting?Revenue timing affects profit, tax impact, margin analysis, and period-wise performance assessment. If income is recognised too early or too late, the financial statements may present a misleading picture of actual operations. Standardised accounting treatment helps link revenue recognition to the underlying business event more accurately.

8. How can weak accounting compliance affect a business beyond reporting?Weak compliance can affect audits, funding discussions, valuation analysis, internal controls, regulatory review, and board oversight. Financial statements that lack proper support or alignment with the applicable framework can create credibility issues, delay transactions, and increase the risk of correction, qualification, or scrutiny from stakeholders.

9. Why is financial statement presentation important even when the numbers are correct?Correct numbers still need proper classification, grouping, and disclosure to be useful. Financial reporting works through both content and presentation. A poorly presented statement can hide risk, weaken interpretation, and create confusion about liquidity, performance, or obligations, even when the underlying accounting entries are technically accurate.

10. How do boards and management benefit from stronger accounting discipline?Stronger accounting discipline improves visibility into business performance, obligations, reporting gaps, and control weaknesses. It helps management make better operational and financial decisions, while boards gain a more reliable basis for oversight. Accurate reporting also improves communication with auditors, lenders, investors, and regulatory authorities.