In business finance, a large share of friction does not come solely from major invoices. It also covers the supporting costs associated with travel, supply, dispatch, documentation, and employee claims. These smaller outflows are frequently recorded late, poorly grouped, or reviewed without sufficient context.

A business cannot evaluate these costs only by the amount. The same rupee value may be a travel support charge in one case, a supplier-billed add-on in another, and a non-claimable personal outlay in a third. The commercial link decides treatment. This is why businesses asking what incidental expenses are need a practical answer tied to accounting, tax, reimbursement, and internal control.

In India, the issue has direct compliance relevance. Section 15 of the CGST Act includes certain incidental charges, including commission and packing, in the value of supply when charged by the supplier. Direct tax treatment also depends on business purpose, documentation, and the exact character of the outflow. A finance team that treats these items casually risks poor coding, weak deductions, and invoice-level tax errors.

What are Incidental Expenses

Incidental expenses are secondary costs that arise from a larger business activity already in progress. They do not represent the main object of spending, yet they help complete the task, movement, or transaction connected to that activity. In practical finance terms, the principal expense carries the main commercial purpose. The incidental expense supports execution around it.

A flight ticket booked for an employee’s official visit is a principal cost. A baggage handling fee paid during that same trip is a supporting cost. A vendor invoice for goods is a principal transaction. Packing charged by the supplier around that supply is a supporting cost. The relationship with the core event is what defines the expense.

What Makes an Expense Incidental

An expense is incidental when three conditions are met. It arises because a larger business event already exists. It supports completion of that event rather than replacing it. It remains subordinate in commercial character, even if it is necessary for proper execution.

Businesses sometimes classify any small cost as incidental. That approach is inaccurate. Size alone does not define character. A small recurring software subscription is not incidental merely because it is low in value. A small packing fee linked to dispatch may be incidental, as it occurs around the supply event itself.

Difference Between Main Expenses and Supporting Expenses

The distinction between principal and supporting expenditure affects bookkeeping, tax reviews, and reimbursements. Principal expenses usually define the transaction itself. These may include inventory cost, hotel tariff, airfare, core logistics contracts, or service fees. Supporting expenditure is allocated to those items and helps them move toward completion.

That is where the incidental expense meaning moves from concept to actual use. If the finance team understands the supporting role of the cost, it can correctly classify the item, properly review supporting documents, and avoid pushing unrelated charges into vague expense heads.

Business Context in India

In India, businesses encounter these outflows across procurement, official travel, service delivery, dispatch coordination, and employee claims. The same label cannot be applied mechanically across all of them. A supplier-billed charge raises one set of questions. An employee reimbursement raises another. To understand what incidental expenses are, it is important to look at the actual context first.

Examples of Incidental Expenses

A strong understanding of incidental travel expenses begins with distinguishing the trip itself from the support costs arising around it. The airfare, train fare, or hotel booking forms the principal travel expense. The smaller costs incurred because the trip is in progress form the supporting layer.

Examples include baggage handling, modest local transport between work locations, communication charges incurred for official coordination during the trip, and laundry during extended travel where company policy permits it. Each example must still pass a business-purpose test. A personal meal upgrade or a leisure detour is not claimable because it occurred during a work trip.

A sales employee attending a client meeting in another city offers a clear case. The flight and accommodation are core travel costs. Small taxi movements between the hotel and the meeting venue, porterage charges, and work-related communication costs may be treated as incidental travel expenses, provided they are policy-compliant and properly supported.

Trade and Supply Examples

Incidental trade expenses arise in connection with the sale, supply, movement, or delivery of goods and services. These are operationally important because they frequently appear on supplier invoices and can affect GST valuation. Packing charges are a direct example. The commission charged in relation to supply is another. Handling, dispatch support, and documentation-related costs may also fall into this layer when they are billed around the transaction.

Take a supplier invoice that contains the value of goods, packing charges, and commission. The goods value is the principal element. The other billed items are attached to that supply and are reviewed as supporting charges. Under Section 15 of the CGST Act, such supplier-charged incidental items can form part of the taxable value.

Administrative Examples

A third category appears in routine execution. This is where the list of incidental expenses usually expands inside office operations. Urgent printing for official submissions, courier add-ons for required dispatch, parking paid for a business meeting, and minor documentation support costs are common illustrations. None of these amounts defines the business transaction on its own. They support completion of the work already underway.

Scenario-Led Reading

Finance teams should review incidental expense examples using transaction logic rather than relying on labels alone. A procurement team coordinating dispatch may incur packing, handling, and urgent paperwork charges. An employee travelling for client work may incur porter charges, local movement, and communication costs. A vendor billing a service may add supporting charges performed at or before delivery. These examples become meaningful because they are tied to an identifiable business event.

Types of Incidental Expenses

This category covers supporting costs arising during official journeys, temporary assignments, site visits, or transfers. It includes amounts incurred while business travel is already underway. The category should not be stretched to absorb unrelated personal expenditure. A clean policy definition is essential because travel claims tend to generate the highest volume of small-value submissions.

Incidental trade expenses arise around the commercial execution of the supply. They may relate to packing, handling, commission, dispatch preparation, or similar support around movement and delivery. This category matters for procurement and tax teams because invoice structure and supplier billing patterns directly affect review.

Administrative Incidental Expenses

Administrative incidental costs support internal execution rather than the movement of people or goods. These may include minor processing charges, printing, documentation support, courier add-ons, or other office-linked outflows arising during task completion. They should be identified carefully because repeated small charges in this category can indicate process inefficiency or poor vendor discipline.

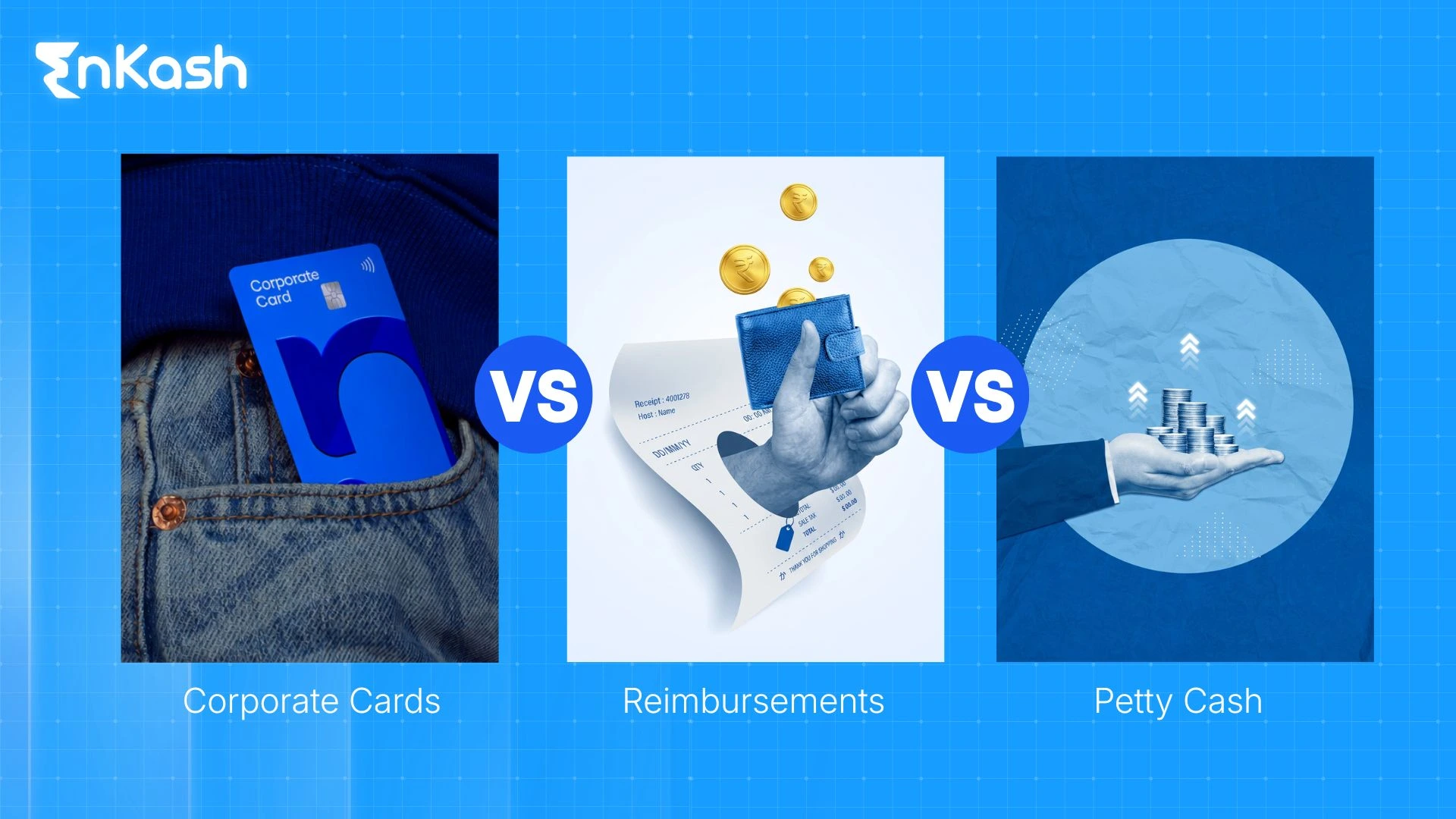

Employee Reimbursement-Based Costs

An employee may first pay a cost personally and later claim reimbursement from the employer. That produces a separate control problem from direct vendor billing. The expense has to be tied to official work, supported by documents, and reviewed against company policy. This type of classification helps teams manage incidental expenses with fewer disputes between employees, managers, and finance reviewers.

Supplier-Billed Charges

A final category covers incidental charges raised directly by the supplier. These charges require careful invoice scrutiny because the tax effect may differ from the costs incurred internally. If the supplier charges an amount around the supply event, the business must review it through valuation rules, commercial documentation, and purchase-side accounting treatment. This category should never be buried under a generic miscellaneous booking.

Read more: Different Types of Expenses in Business: Know It All

Taxes and Deductions of Incidental Expenses

Tax Treatment Depends on the Nature of the Expense

There is no single tax rule that governs all incidental expenses. Treatment depends on the cause of the outflow. A supplier-billed charge linked to a supply may raise a GST valuation issue. An employee claim may raise a reimbursement or payroll issue. A general business outlay recorded in the books may be tested under the direct tax rules governing business expenditure.

For this reason, labels alone cannot decide tax treatment. The same description can produce different outcomes when facts differ. Finance teams must review who incurred the expense, why it was incurred, how it was documented, and how it was recorded in the books.

GST Treatment of Supplier-Billed Charges

Section 15 of the CGST Act states that the value of supply includes incidental expenses, including commission and packing, charged by the supplier to the recipient. It also includes amounts charged for anything done by the supplier in respect of the supply, at or before delivery of goods, or the supply of services. This is the statutory anchor for reviewing supplier-billed incidental charges.

The operational impact is direct. If a vendor invoices separately for packing, commission, or similar support costs, those amounts do not fall outside tax valuation merely because they appear on separate lines. The invoice has to be read as a whole, with attention to the statutory inclusion rule. Businesses dealing with high dispatch volumes, distribution-linked supplies, or contract execution billing need strong review discipline in this area.

Income Tax Deductibility for Businesses

For direct tax purposes, the general business expenditure principle under Section 37 remains important. Official Income-tax Department material states that expenditure laid out wholly and exclusively for business or profession is allowable, subject to statutory restrictions. This is the relevant framework for many business-side incidental outflows.

This does not automatically make every claim deductible. The expense must have a clear business nexus. It must be supported properly. It must not be personal in character. It must not fall into a prohibited category. Documentation becomes decisive at this point. Bills, approval trails, trip details, invoice references, and internal policy alignment strengthen the deductibility position.

Allowance Versus Reimbursement

An incidental expense allowance is not the same as reimbursement. Allowance refers to a fixed or prescribed amount granted for a specified purpose. Reimbursement refers to payment against actual expenditure incurred and later claimed. The tax treatment of the two may differ because the legal and documentary basis differs.

Income-tax Department guidance under Section 10(14), read with Rule 2BB, refers to allowances granted to meet the cost of travel on tour or on transfer. It also refers to sums paid in connection with the transfer, packing, transportation of personal effects, and daily allowance for journeys connected with official duties or transfer. This matters in the travel context, though the treatment depends on the specific facts and compliance with the legal conditions.

Frequent Tax Errors

Errors usually arise from poor classification rather than from complex law alone. Businesses may claim unsupported incidental costs without enough evidence. Teams may mix personal spending with official claims. Purchase reviewers may overlook GST valuation treatment on supplier-billed support costs. Employees may use vague descriptions that obscure the character of the outflow. Each of these errors weakens the support for deduction and creates avoidable review risk.

Benefits of Incidental Expense Management

Better Cost Visibility

Businesses that manage incidental expenses well gain a clearer picture of recurring low-value outflows. This matters because leakage rarely appears first in the major heads. It tends to spread through repeated, small support charges that are individually small but collectively material.

Stronger Financial Discipline

A disciplined review framework helps prevent loose claims, repetitive add-ons, and coding errors. It also improves management's understanding of how travel, procurement, and administrative processes are performing. If a team keeps incurring the same support charge repeatedly, that pattern can signal an operational weakness rather than an unavoidable expense trend.

Faster Claim Resolution

When categories are clear and documentation standards are defined, finance teams can process claims faster. Managers know what must be checked. Employees know what is claimable. Reimbursement disputes decline because the control framework is visible in advance rather than applied inconsistently later.

Better Audit Readiness

Accurate mapping of incidental expense examples to policy-backed categories strengthens the audit trail. Bills, approvals, purpose notes, and consistent ledger coding reduce friction during internal review and statutory examination. That is a concrete financial control gain, not a procedural formality.

More Reliable Reporting

A business cannot produce reliable departmental reporting if support costs are buried in random heads. Structured treatment of these items improves travel analysis, purchase analysis, and team-wise cost visibility. That improves budgeting and operating decisions across functions.

How to Control Incidental Expenses

Set a Clear Policy Boundary

The first control step is definitional clarity. The policy should state what qualifies as incidental expenses, what does not qualify, which functions can incur them, and what evidence is required. Ambiguous policy language creates downstream confusion because every approving manager starts interpreting the category differently.

Build Fixed Classification Buckets

A business should create fixed buckets for travel, trade, administrative, reimbursable, and non-reimbursable items. This structure helps manage incidental expenses without pushing everything into a broad miscellaneous ledger. Strong classification also improves trend analysis by allowing comparable items to be recorded together.

Apply Approval Rules and Claim Standards

Approval thresholds should reflect risk and recurrence. A simple, small-value charge may need basic approval, but repeated similar claims may justify higher review. Claim standards should require business-purpose notes, bills wherever available, and timely submission after the expense is incurred. Delayed claims reduce accuracy and weaken documentation quality.

Standardise Reimbursement Workflows

A standard claim path reduces inconsistency. Employees should know where to file the expense, how to describe it, and which documents to attach. Managers should verify business purposes. Finance should review category, policy fit, tax relevance, and booking treatment. This is particularly important for incidental expense allowance structures and reimbursement-led travel claims, where weak workflows can blur the distinction between entitlement and actual spend.

Use Digital Review and Evidence Storage

Digital systems improve control by consolidating bill capture, timestamps, approval records, and category selection in one place. Even a disciplined spreadsheet-based process is better than unstructured email claims, provided it records enough evidence. The central requirement is traceability. A finance team should be able to reconstruct the origin, purpose, approval, and accounting treatment of each material support charge.

Review Patterns and Correct Root Causes

Periodic review helps identify recurring issues hidden behind small-value charges. Repeated packing fees may indicate weak vendor negotiation. Frequent local travel claims may indicate poor trip planning. Constant urgent printing may point to workflow inefficiency. The best control system does not stop at rejection. It identifies the operating cause and corrects it.

Train Employees on Claimable and Non-Claimable Spend

A large share of avoidable friction comes from misunderstanding. Employees need to know what counts as an official support expense, what remains personal, when prior approval is needed, and how to document the claim. Clear training creates more accurate submissions and fewer disputes. That is one of the most effective ways to manage incidental expenses without increasing review burden.

Conclusion

A precise understanding of the meaning of incidental expenses helps businesses treat these costs as a defined financial category rather than a vague side issue. The real test lies in context. Travel support costs, supplier-billed additions, employee reimbursements, and office execution charges cannot be reviewed through one generic lens. Each item must be linked to its business event, supported with records, and classified correctly.

In India, the issue carries direct tax and accounting relevance. Supplier-billed incidental charges may be included in the GST valuation under Section 15. Direct tax deductibility depends on business purpose, documentary support, and the legal character of the outflow. A business that handles these items with precision builds cleaner books, stronger controls, and fewer review disputes. That is the practical value of disciplined treatment of incidental expenses.

FAQs

1. How can a business identify whether a charge is incidental or part of the main expense?A business should test the commercial purpose of the charge. If the amount supports completion, handling, movement, or administration of a larger transaction, trip, or service, it may be incidental. If it represents the primary object of spending itself, it should be treated as the main expense instead.

2. What is the practical difference between travel-related incidental costs and trade-related incidental costs?Travel-related incidental costs arise during official journeys, transfers, or temporary duty and support employee movement. Trade-related incidental costs arise around the supply, handling, delivery, packing, commission, or dispatch of goods and services. The distinction matters because reimbursement treatment and GST valuation issues usually arise in different ways.

3. Why should businesses avoid recording these costs under a generic miscellaneous expense head?A generic miscellaneous head weakens clarity. It becomes harder to test business purpose, detect recurring leakage, support tax treatment, or review vendor billing patterns. Clear classification improves accounting accuracy and strengthens internal controls because the nature of each cost remains visible during reporting, reimbursement review, and assessment.

4. How should supplier-billed support charges be reviewed under GST?Supplier-billed support charges should be reviewed with the invoice as a whole, not as isolated line items. Under Section 15 of the CGST Act, incidental expenses, including commission and packing charged by the supplier, can form part of the value of supply, along with amounts charged before or at delivery.

5. What factors decide whether a business can claim a deduction for a supporting outflow?The deduction position depends on business nexus, documentation quality, accounting treatment, and the legal character of the expense. A business must show that the spending was incurred wholly and exclusively for business purposes. Weak records, mixed personal use, or vague descriptions can materially weaken the claim.

6. How is an allowance different from a reimbursement in this context?An allowance is a fixed or prescribed amount granted for a specified purpose, while reimbursement is payment against actual expenditure incurred and later claimed. This distinction matters because tax treatment, payroll handling, and evidence requirements differ. The label alone does not determine treatment. The underlying facts remain decisive.

7. What documents should support a claim for a small business-related outflow?A defensible claim should include the bill or receipt where available, the date, the amount, the business purpose, the approving authority, and the link to the trip, task, or transaction. Consistent ledger coding and policy alignment further strengthen the record during tax reviews, audits, and internal finance checks.

8. How should finance teams treat recurring low-value support costs that appear every month?Recurring low-value costs should not be ignored merely because each item is small. Finance teams should review whether the pattern reflects vendor pricing, poor travel planning, weak process design, or policy gaps. Repetition can make a minor cost financially significant and may justify separate coding or stronger approval rules.

9. What mistakes commonly lead to the wrong treatment of these costs in accounts and tax review?Common mistakes include using vague expense descriptions, mixing personal and business spending, failing to account for supplier-billed valuation implications, missing supporting records, and booking unlike items under a single broad head. These errors make it harder to defend deductions, verify policy compliance, and maintain reliable financial statements.

10. How can a company build a stronger policy for these expenses?A stronger policy should define qualifying categories, excluded items, approval thresholds, documentation standards, submission timelines, and reimbursement rules. It should also clarify treatment for supplier-billed additions and travel-linked claims. Good policy design reduces ambiguity and improves consistency across employees, managers, procurement teams, and finance reviewers.