Government spending on infrastructure, healthcare, defence, education, and welfare depends largely on tax revenue. Within India’s fiscal structure, direct tax represents a primary revenue source because it is collected from income earners and profit-making entities rather than consumption.

Recent Ministry of Finance releases show sustained growth in direct tax collections. Provisional figures indicate collections crossing ₹19 lakh crore in recent financial years, with personal income tax contributing a rising share and corporate tax continuing to remain a major component. The increase reflects expansion in the taxpayer base, improved reporting systems, and stronger digital compliance.

The introduction of direct tax as a structured revenue mechanism reflects a policy shift toward income-linked contribution. When taxation is aligned with earnings and profits, governments can generate predictable revenue while maintaining fairness across different income groups. This makes direct taxation central to fiscal planning and long-term economic management.

India administers direct taxation through statutory provisions led by the Income Tax Act, supported by annual Finance Act updates that refine rates, deductions, and procedural rules. Oversight by the Central Board of Direct Taxes ensures uniform implementation, dispute resolution frameworks, and standardised taxpayer services.

Technology has significantly strengthened the direct tax ecosystem. Electronic filing, pre-filled returns, data matching, and automated verification have improved accuracy and reduced processing timelines. As a result, direct taxation now acts as a measurable indicator of formal economic activity and financial transparency.

What is Direct Tax

Direct tax refers to a form of taxation imposed on income, profits, or gains where the payment responsibility remains with the person or entity that earns the income. The defining feature of direct tax is that the burden cannot be transferred to another party, making the taxpayer the final bearer of liability.

Under India’s regulatory framework, direct taxation applies after taxable income is calculated using statutory rules that classify income sources, allow deductions, and determine applicable rates. The resulting liability is then paid directly to the government through prescribed compliance mechanisms.

The scope of direct tax extends across several taxpayer categories. Individuals may pay tax on salary, professional income, or investments. Companies are taxed on net profits. Partnership firms, Hindu Undivided Families, trusts, and certain non-resident entities may also fall within the direct taxation framework when income is generated within India.

Several characteristics clarify what is direct tax in practice. The system is income-linked, progressive in rate design, and dependent on formal disclosure through return filing and documentation. Regulatory provisions define how liability is calculated, reported, and assessed, ensuring consistency across taxpayers.

Understanding direct taxation is essential because tax liability directly affects disposable income, business profitability, and financial decision-making. By linking taxation to earnings rather than spending, direct tax operates as a structured mechanism through which economic output is recorded, evaluated, and taxed within India’s legal framework.

Types of Direct Tax

The classification of types of direct tax in India is based on the nature of income, the entity earning that income, and the financial transaction that triggers tax liability. Each category exists to address a specific source of earnings or wealth creation, ensuring that direct taxation captures different forms of economic activity within a defined legal framework.

Income Tax

Income tax represents the most widely recognised form among the types of direct taxes in India. It applies to earnings received by individuals and other eligible entities across salary, business income, professional fees, rental income, and investment returns. Liability is determined after computing total income, applying deductions where allowed, and calculating tax using applicable slab rates. This category forms the foundation of India’s direct tax system due to its broad taxpayer coverage.

Corporate Tax

Corporate tax applies to profits generated by companies operating within India’s jurisdiction. Domestic and foreign companies are taxed under separate provisions that define applicable rates, allowable expenses, and reporting requirements. Within the broader structure of direct taxation, corporate tax plays a significant role in revenue generation because it captures business profitability and reflects economic performance across sectors.

Capital Gains Tax

Capital gains tax arises when a capital asset is transferred at a value higher than its acquisition cost. Assets may include property, securities, mutual funds, or other investments recognised under tax law. Classification into short-term and long-term gains determines the applicable rate. This category ensures that wealth created through asset appreciation is captured within the types of direct tax framework.

Securities Transaction Tax (STT)

Securities transaction tax applies to specified transactions executed on recognised stock exchanges. It is levied at the time of buying or selling eligible securities, making it a transaction-linked component within direct taxation. The objective is to simplify reporting of market activity while creating a traceable record of taxable financial transactions.

Dividend Distribution Tax (DDT)

Dividend distribution tax historically applied to companies distributing profits to shareholders. Although the taxation approach has shifted and dividends are now taxed in the hands of recipients, the concept remains relevant when understanding the evolution of types of direct taxes in India. It illustrates how policy design adapts to improve transparency and align taxation with income recipients.

Wealth Tax

Wealth tax previously applied to specified high-value assets exceeding defined thresholds. While this tax has been abolished, it remains an important reference point in discussions of direct tax policy because it demonstrates earlier approaches to taxing accumulated wealth rather than income flows.

Other Direct Tax Examples

Certain additional provisions complement the main types of direct tax categories. Gift taxation rules address income received without consideration beyond the prescribed limits. Property tax, administered at the municipal level, reflects ownership-based taxation. Concepts such as the minimum alternate tax also illustrate mechanisms used to ensure that entities with reported profits contribute within the direct taxation structure.

Read more: What Is Payment Success Rate and Why Is It Important

Examples of Direct Tax in Real Life

Salary Income Taxation

A common example of a direct tax arises from salary income. Employers deduct tax at source based on estimated annual income, declared deductions, and applicable slab rates. The individual remains responsible for verifying the final liability while filing returns. This illustrates how direct taxation applies directly to earned income rather than spending.

Property Sale and Capital Gains

When an individual sells property at a price higher than the purchase cost, the profit is taxed under capital gains provisions. The applicable rate depends on asset type, holding period, and indexation rules. This scenario shows how direct tax captures wealth created through asset appreciation.

Investment Transactions

Selling shares, mutual funds, or other securities may generate taxable gains. These gains become part of taxable income once realised, and investors must report them while calculating their liability. This reflects the role of direct taxation in tracking income from financial markets.

Business Profit Taxation

Businesses compute taxable profit after deducting allowable expenses from revenue. Companies then pay corporate tax on net profits according to statutory rates. This example highlights how direct tax applies to organised economic activity and profitability.

Taxation on Specified Gifts

Financial gifts received above prescribed thresholds may become taxable in the recipient’s hands. Such receipts are treated as income under direct taxation, demonstrating that direct tax also applies to certain non-earned financial inflows.

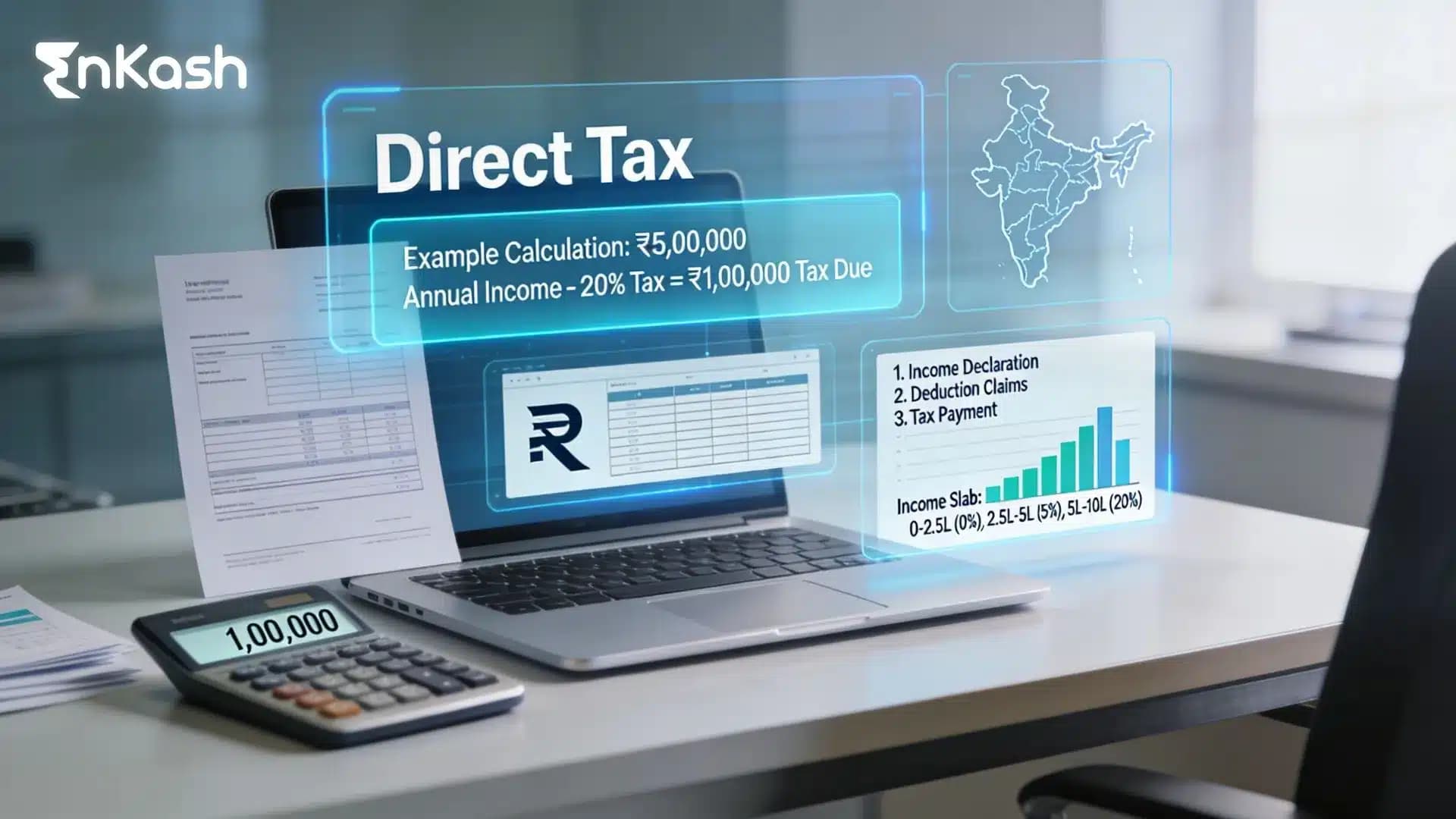

How to Calculate Direct Tax

Identify Total Taxable Income

The calculation of direct tax begins with determining the total income earned during the financial year. This includes salary, business or professional income, capital gains, rental earnings, and income from other sources. Each category is computed separately under statutory rules before arriving at gross total income within the direct taxation framework.

Apply Eligible Deductions and Exemptions

After computing gross income, taxpayers reduce allowable deductions permitted under law. These may include specified investments, insurance contributions, retirement savings, and certain expenditure categories recognised under the Income Tax Act. This step ensures that direct tax is calculated on taxable income rather than total earnings.

Determine Applicable Tax Rates

Once taxable income is finalised, the next step involves applying relevant tax slabs or prescribed rates depending on the taxpayer category. Individuals follow slab-based rates, while companies apply defined corporate tax rates. This stage establishes the base direct tax liability before additional adjustments.

Add Surcharge and Cess

Where income crosses defined thresholds, a surcharge may apply. Health and education cess is then calculated as a percentage of the tax amount. These additions form part of the final direct taxation liability and must be included before determining payable tax.

Adjust Tax Credits and Advance Payments

The final step involves adjusting tax already paid through tax deducted at source, advance tax, or other available credits. After these adjustments, the remaining balance represents the net direct tax payable or the refund due under the direct taxation system.

Features of Direct Tax

Non-Transferable Tax Burden

A defining feature of direct tax is that the responsibility to pay remains with the person or entity that earns the income. The liability cannot be shifted to another party through pricing or transaction structures. This distinguishes direct taxation from consumption-based taxes, where the burden moves along the supply chain.

Income-linked Structure

Direct tax is calculated based on earnings, profits, or realised gains rather than spending behaviour. The amount payable varies according to the level and nature of income, ensuring that taxation reflects economic capacity. This income linkage makes direct taxation sensitive to changes in employment, business performance, and investment outcomes.

Progressive Rate Design

Many components of direct taxation follow a progressive framework where tax rates increase as income rises. This structure supports fiscal equity by aligning contributions with financial ability. Progressive design also allows policymakers to adjust thresholds and rates to address economic conditions.

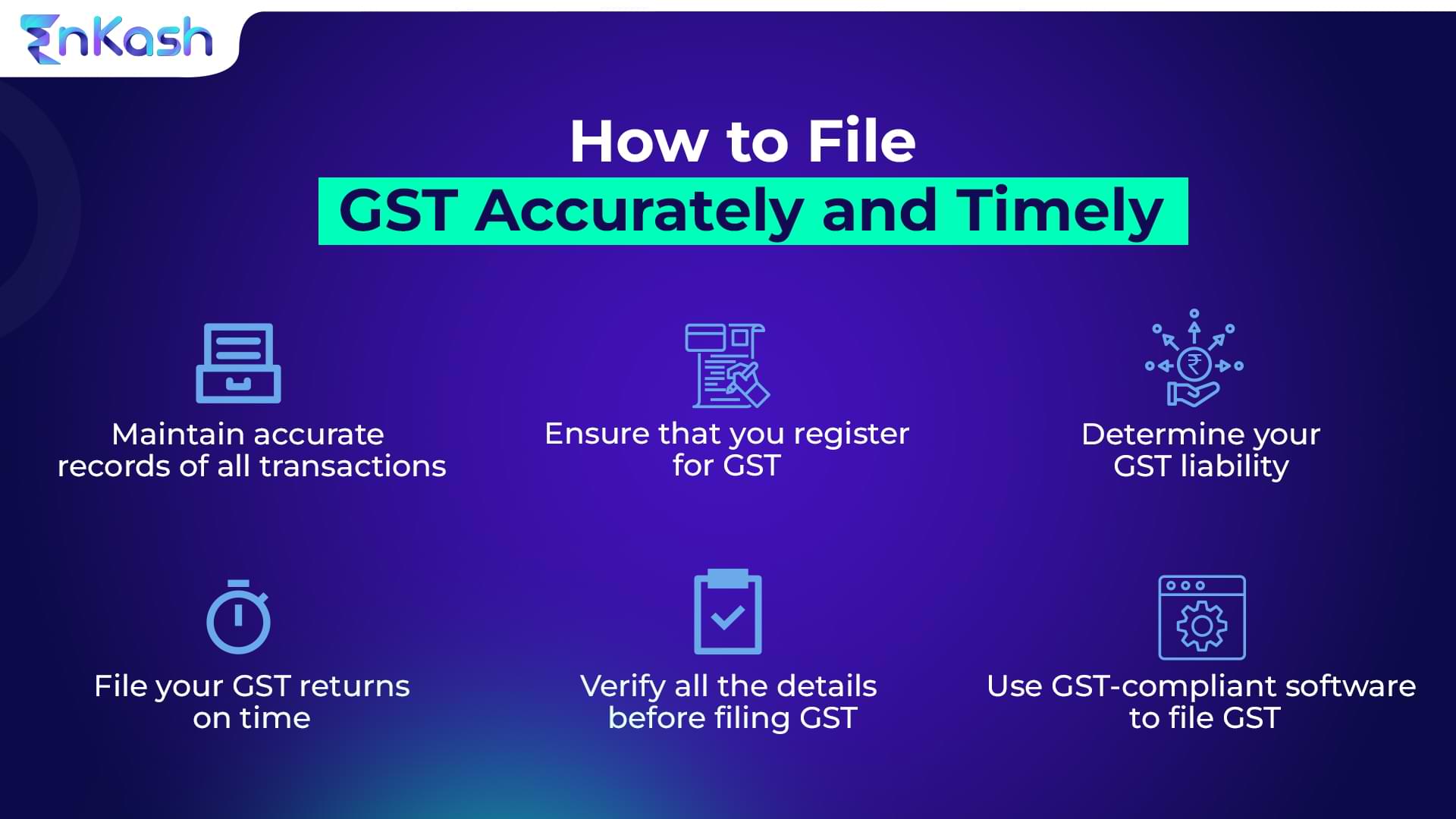

Compliance and Reporting Framework

The administration of direct tax relies on structured disclosure, documentation, and periodic return filing. Taxpayers must report income sources, claim deductions, and maintain records that support calculations. This reporting framework improves transparency and enables regulatory oversight within the direct taxation system.

Annual Assessment Cycle

Direct taxation operates through defined assessment periods where income for a financial year is evaluated and final liability is determined. This cyclical approach allows authorities to reconcile reported income with available financial data, supporting consistent enforcement and predictable compliance timelines.

Advantages of Direct Tax

Equity Based Contribution

A major advantage of direct tax lies in its alignment with the ability-to-pay principle. Since liability depends on income or profit levels, individuals and businesses contribute in proportion to their financial capacity. This structure supports fairness within the income-based tax system and reduces the burden on lower-income groups.

Stable Government Revenue

Direct tax provides a relatively predictable revenue stream because it is tied to recurring income and corporate profitability. Governments can forecast collections with greater accuracy, which helps in planning expenditure, budgeting public programmes, and managing fiscal targets.

Supports Income Redistribution

Progressive rate structures within direct tax enable redistribution by collecting a higher share from higher-income segments. The revenue can then fund social programmes, infrastructure, and welfare initiatives. This makes income-linked taxation an important policy instrument for addressing income inequality.

Encourages Financial Transparency

Because direct tax requires income reporting, documentation, and return filing, it promotes transparency across the financial system. Digital reporting, employer disclosures, and data integration improve traceability of earnings, strengthening the formal economy within the regulated tax framework.

Policy Flexibility for Economic Management

Governments can adjust rates, deductions, and incentives within the income-based tax structure to influence behaviour such as investment, savings, or sectoral growth. This flexibility allows direct tax policy to function not only as a revenue tool but also as a mechanism for economic signalling and reform implementation.

Limitations of Direct Tax

Compliance Complexity

A key limitation of direct tax relates to the procedural requirements involved in calculating liability, maintaining documentation, and filing returns. Taxpayers must track multiple income sources, apply deductions correctly, and interpret regulatory updates. This complexity can create challenges for individuals and small businesses without professional support.

Risk of Tax Evasion

Because direct tax depends on income disclosure, gaps in reporting may lead to underreporting or evasion. Informal earnings, cash transactions, and fragmented financial records can reduce visibility for authorities. Addressing this limitation requires stronger data integration, enforcement mechanisms, and improved taxpayer awareness.

Administrative Burden

The implementation of direct tax involves assessment processes, verification systems, dispute resolution, and ongoing regulatory updates. These administrative requirements can increase operational costs for both tax authorities and taxpayers, particularly when policy changes introduce new compliance steps.

Impact on Disposable Income

Since direct tax is deducted from earnings or profits, it directly influences the amount of income available for consumption, savings, or investment. Higher liability levels may affect household spending decisions and business reinvestment capacity, especially during periods of economic slowdown.

Policy Interpretation Challenges

Frequent amendments, evolving judicial interpretations, and technical provisions can create uncertainty around direct tax treatment in specific situations. Taxpayers may require professional guidance to ensure accurate reporting, highlighting how regulatory complexity remains a structural limitation of income-based taxation.

Conclusion

Direct tax defines the method through which earnings, business results, and investment gains are evaluated in India’s tax environment. From individual earnings and investment returns to corporate profitability, direct tax establishes a structured link between economic activity and government revenue. The introduction of direct tax as an income-based mechanism reflects a policy approach that prioritises fairness, accountability, and predictable resource mobilisation for national development.

The framework also highlights how taxation extends beyond collection. It shapes financial behaviour, influences investment decisions, and strengthens transparency across the formal economy. At the same time, recognising the demerits of direct tax, such as compliance complexity, reporting requirements, and interpretation challenges, is important for a balanced understanding. These limitations continue to inform policy reforms aimed at simplification and improved taxpayer experience.

Overall, direct tax remains a foundational element of India’s public finance architecture. By aligning liability with earning capacity while evolving through digital administration and regulatory updates, it functions as both a revenue instrument and a governance tool that supports long-term economic stability.

FAQs

1. How does tax deducted at source affect final liability?Tax deducted at source acts as an advance payment collected during the year on salary, interest, or contractual income. When returns are filed, this deducted amount is adjusted against the total liability calculated after deductions and exemptions. If the deducted amount exceeds the final liability, a refund is issued, while any shortfall must be paid by the taxpayer.

2. Why are tax slabs revised periodically?Tax slabs are revised to reflect inflation, income growth, and policy priorities. Governments adjust thresholds to maintain fairness across income groups and stimulate consumption or savings when needed. Changes may also simplify compliance and expand the taxpayer base, ensuring that the system remains aligned with economic conditions and fiscal objectives.

3. How do deductions influence taxable income?Deductions reduce the portion of income subject to tax by recognising eligible investments, insurance contributions, retirement savings, and specified expenses. By lowering taxable income rather than total earnings, deductions encourage long-term financial planning while also shaping investment behaviour. Their availability directly affects the final liability calculated during return filing.

4. What role does advance payment play in tax compliance?Advance payment requires individuals and businesses with significant non-salary income to pay liability in instalments during the financial year instead of waiting until return filing. This mechanism improves revenue flow for the government and prevents large year-end payments for taxpayers. It also reduces interest charges that may arise from delayed payment.

5. How are non-resident taxpayers treated under Indian tax rules?Non-resident taxpayers are taxed based on income that accrues, arises, or is received within India. Their liability depends on residential status, applicable tax treaties, and the nature of income such as salary, capital gains, or business profits. Double taxation agreements may allow credits or exemptions to prevent the same income from being taxed twice.

6. Why is record keeping important for taxpayers?Maintaining financial records supports accurate reporting of income, deductions, and credits. Documents such as salary statements, investment proofs, expense invoices, and transaction reports help verify calculations during return filing or assessment. Proper record keeping reduces disputes, ensures compliance, and allows taxpayers to respond effectively if clarification is requested by authorities.

7. How do tax refunds occur after return filing?Refunds arise when the total amount paid through withholding, advance payments, or self-assessment exceeds the final liability calculated in the return. After verification, authorities process the excess amount and transfer it to the taxpayer’s registered bank account. Timely filing and accurate reporting help prevent delays in refund processing.

8. What happens if income is reported incorrectly?Incorrect reporting can lead to notices, reassessment, penalties, or interest depending on the nature of the error. Minor mistakes may be corrected through revised returns within the allowed timeline, while significant discrepancies may trigger verification or audit procedures. Accurate disclosure and documentation reduce the risk of compliance issues.

9. How do tax rules influence investment decisions?Tax provisions affect where individuals allocate funds by offering incentives for specific instruments such as retirement savings, insurance, or long-term investments. Rate differences across asset classes can also influence holding periods and portfolio strategy. As a result, taxation plays a role in shaping financial planning alongside risk and return considerations.

10. Why does digital filing matter for taxpayers?Digital filing improves accuracy, reduces manual errors, and speeds up processing through automated validation and data integration. Pre-filled information simplifies reporting, while online verification shortens timelines for assessment and refunds. The digital environment also strengthens transparency by creating consistent records across financial institutions and regulatory systems.