In India, people search this topic when they want a clear answer before sending money through a banking or UPI app. A P2P transaction is a person-to-person payment in which one individual sends money directly to another through an authorised digital payment system. In India, this commonly happens through UPI apps, banking apps, or other bank-linked transfer channels.

For Indian users, P2P payments are now part of regular financial activity. People use them to split bills, send money to family, repay a friend, or transfer small amounts without using cash. The process feels quick, but the payment still depends on proper recipient selection, verified account linkage, and user authentication.

Clarity around P2P meaning in banking helps users recognise the difference between a direct personal transfer and other digital payment formats. This helps users make better decisions during the transaction and reduces the risk of using the wrong payment route or sending money without proper verification.

This guide is based on RBI retail-payments guidance, NPCI’s UPI framework, and NPCI’s UPI safety advice for users.

What are P2P Payments

A P2P payment is a person-to-person transfer in which one individual sends money directly to another through an authorised digital payment channel. In India, this commonly happens through UPI, IMPS, and bank-linked transfer routes.

P2P full form in banking is person-to-person. In payment classification, this term is used when both ends of the transaction are individual users. The category is defined by the payer-payee relationship, not by the app's screen design or the payment platform's brand.

In practical Indian payments use, a transaction is treated as P2P when funds are directed to an individual recipient through an authorised digital channel such as UPI, IMPS, or a bank-transfer route. This classification helps separate direct individual transfers from merchant collections, billed payments, and other commercial payment flows. The distinction is operational because the recipient type affects how the transaction is interpreted within the wider payments framework.

P2P payments are therefore identified less by the interface and more by the payment context. A transfer can begin in a bank app, UPI app, or another digital payment system, yet the transaction is still considered P2P if the recipient is an individual and the payment is personal. This is why the same digital ecosystem can support different payment categories without treating them as identical.

Examples of P2P Payments

Sending money to familyA person may transfer funds to a parent, sibling, or child for regular household needs, urgent expenses, or day-to-day support. The payment goes directly to an individual recipient.

Splitting a shared expenseFriends or flatmates may use a personal transfer to settle a shared bill after a meal, ride, utility payment, or grocery purchase. This is a common use of person-to-person payments.

Repaying borrowed moneyA user may send money back to someone who paid first on their behalf. In this case, the transfer is a direct repayment between two individuals.

Paying a personal share of rent or household costsIn shared living arrangements, one person may collect the total amount, and others may transfer their share separately. This still falls within a person-to-person payment context.

Reimbursing a personal purchaseA family member or friend may buy medicine, travel tickets, or household items for someone else first. The other person may then reimburse that amount through a direct digital transfer.

How Do P2P Payments Work in India

A person begins a P2P transfer money journey by opening a bank app or UPI app and choosing the intended recipient. The recipient can be selected through a UPI ID, a supported mobile-number-based flow, bank account details, or a QR code. After this step, the sender enters the amount and checks the payee's name displayed on the screen before proceeding. The transfer is completed only after the sender authorises it with the required payment credentials. In most cases, the instruction is processed within seconds through the connected banking network.

The Basic Process Behind a P2P Transfer

Recipient identificationThe first step is choosing the intended payee. The system needs a valid recipient reference before it can prepare the transfer instruction.

Amount entry and reviewThe sender enters the amount and checks the payment details shown on the screen. This review stage helps confirm that the transfer is being sent to the right person.

User authorisationThe payment moves ahead only after the sender completes the required approval step. This stage confirms that the transfer has been actively authorised.

Processing and status updateAfter approval, the payment instruction is sent for processing. The app then displays whether the transaction has been completed, is pending, or has failed.

Common Ways Users Send Money

UPI IDA UPI ID acts as a payment address linked to the recipient. It allows the sender to direct funds without entering full bank account details.

Mobile numberIn supported flows, a registered mobile number helps identify the recipient for payment. This route is useful when the sender does not have the other person’s account details.

Bank account detailsSome transfers are made by entering the recipient’s account number and IFSC. This route still supports direct movement of funds between individuals.

QR-based transferA QR code allows the sender to scan it and display the recipient's details on the screen. The sender can then verify the payee information before approving the transfer.

Why UPI is Central in India

Shared payment infrastructureUPI connects multiple banks and payment apps through a common interoperable framework. This makes person-to-person digital transfers easier to process across institutions.

Faster day-to-day usageFor many users, UPI has reduced reliance on branch-led or cash-led transfer habits in routine personal payments. The process is built for direct and frequent use.

Multiple payment identifiersUPI supports multiple ways to identify the recipient, such as a payment address, mobile number, or a QR code. This gives users multiple ways to initiate a personal transfer.

Interoperable experienceThe app interface may vary, but the transfer still runs through an authorised payment setup that supports fund movement across participating banks.

P2P vs P2M Payments in India

A P2P payment is a transfer between two individuals, while a P2M payment is a transfer from an individual to a merchant. In India, the same digital payment ecosystem can support both. NPCI’s UPI framework explicitly supports both person-to-person (P2P) and person-to-merchant (P2M) transactions, which is why the payment flow may look similar on screen even when the transaction type is different.

The key difference lies in the recipient type and payment purpose. In a P2P transaction, money is usually sent to a friend, family member, flatmate, or another individual for a personal reason such as splitting expenses, repayment, or support. In a P2M transaction, the payment is made to a business, shop, service provider, platform, or merchant for goods or services. This difference matters because it affects how the payment should be interpreted, recorded, and reviewed.

This distinction is important in India because some payment screens may appear similar even when the underlying context is not. A QR code linked to an individual typically supports a personal transfer, while a merchant-facing QR is designed for commercial collection. NPCI’s UPI safety guidance also makes an important user-protection point: scanning a QR code is for making a payment, not for receiving money.

For users, the practical takeaway is simple. If the payment is being made to another individual for a personal purpose, it is a P2P payment. If it is being made for a purchase, service, subscription, bill, or other commercial reason, it should be understood as P2M. Reading the payment context correctly helps users verify the receiver properly, classify the transfer correctly, and reduce avoidable mistakes before approval.

How Safe and Secure are P2P Payments

Digital P2P payments are built on controlled user approval, linked bank access, and identity checks visible during the payment flow. A transfer does not move on its own. It moves only when the sender reviews the payment details and completes the final authorisation step. This structure gives users a clear role in protecting the transaction before money leaves the account.

What Makes P2P Payments Secure

User-controlled authorisationEvery transfer requires the sender's active approval. This reduces the chance of an unintended payment moving through without direct user action.

Linked banking frameworkThe payment runs through an authorised banking or payment setup connected to the user’s account. This creates a formal transaction trail that can be tracked and reviewed later.

Recipient name visibilityThe app usually displays the recipient's name before final confirmation. This gives the sender a chance to stop the transfer if the payee details do not match expectations.

Recorded transaction historyEach completed payment leaves a digital record inside the app or banking system. This helps users verify what was sent, when it was sent, and to whom it was directed.

Common Fraud Risks Linked to P2P Payments

Fake collect requestsSome fraud attempts begin with a payment request that looks genuine on the screen. A user who approves it without reading the details may end up authorising an unwanted debit.

Misleading QR scansA QR code can look harmless, but the sender still needs to verify the recipient's identity after scanning. The code itself should never replace on-screen verification.

Social engineering attemptsFraudsters may pressure users through calls, messages, or urgent instructions. These attempts usually rely on confusion, speed, or fear rather than any failure in the payment system.

Weak payee verificationA transfer can also go wrong when the sender reads the name carelessly or skips the review step. In that case, the issue begins with poor checking rather than a technical flaw.

Safety Checks Before Confirming a Payment

Verify the recipient's name carefullyThe displayed name should match the intended receiver before approval. A small mismatch deserves attention before moving ahead.

Review the amount and payment purposeUsers should read the amount once again and confirm why the transfer is being made. This reduces avoidable errors during routine payments.

Never share sensitive approval detailsA UPI PIN or OTP should remain private at all times. NPCI also advises users to enter the UPI PIN only on the app’s UPI PIN page and never share it with anyone. Anyone asking for these details is asking for control over the transaction.

Pause when something feels unusualUnexpected urgency, vague payment instructions, or unfamiliar requests deserve a second look. A short pause can prevent a costly mistake.

This is how users should assess P2P QR code payments and other direct transfer routes from a risk perspective. The payment framework supports control, but the final layer of protection comes from careful on-screen review.

Benefits of P2P Payments

The rise of P2P payments is closely linked to user convenience, transfer speed, and payment visibility. These benefits explain why this payment type now plays a routine role:

Faster Movement of Personal Funds

A person can send money within minutes when the recipient's details are already available in the app. This is useful in situations where the payment cannot wait, such as bill splitting, urgent family support, or small reimbursements. The speed improves convenience, but it also supports better financial response in everyday situations.

Simpler Execution for Routine Transfers

Direct transfers are easier to complete because the user does not have to rely on paper instruments or branch-led instructions for small personal payments. A digital payment route reduces effort on the user end and makes the transfer process easier to follow on-screen. This is valuable for people who want a clean and readable payment flow.

Better Visibility of Transaction Records

Each completed P2P transfer leaves a digital trail that can be reviewed later. Users can check the recipient name, amount, date, and status in the app or in the linked banking channel. This improves payment visibility and helps users confirm whether money was sent, received, or is still under review.

Useful for Low-value and Frequent Payments

Direct person-to-person transfers work well for small, frequent payments between individuals. These may include household sharing, short-term support, expense settlements, or repayment of minor dues. The system helps users complete these payments without creating an unnecessarily heavy process for each transaction.

Wider Usability Across Digital Channels

Users can initiate personal transfers through different digital interfaces while still operating within the larger banking and payments system. This provides flexibility in how the transaction begins while keeping the movement of money within an authorised framework. For users, this improves access without reducing payment control.

Companies Offering P2P Payments in India

Digital P2P payments in India are supported by a mix of banks, UPI apps, and payment service providers. Each of them plays a different role in the transfer journey. Some provide the user-facing app, some manage the bank account connection, and some support payment initiation within the regulated digital payments framework. For the user, the experience may appear app-led. In practice, the transaction depends on coordination between the interface, the linked bank, and the payment network.

Banks as Payment Access Providers

Banks remain central to person-to-person digital transfers because the money ultimately moves through bank-linked accounts. A banking app may allow users to send funds directly, review transaction history, and manage recipient details within the same environment. This gives users a familiar channel with direct account visibility.

UPI Apps as Transfer Interfaces

UPI apps have made it easier to initiate personal digital transfers by offering a more flexible front-end experience. Users can search for recipients, scan QR codes, check payment status, and approve transfers from a single-screen flow. The app improves usability, but it still relies on the underlying banking system.

Payment Service Providers in the Transaction Chain

Some companies support the payment experience without holding the user’s money directly. Their role may include enabling the interface, supporting payment routing, assisting with transaction records, or helping users navigate failed-payment support. This is where P2P business infrastructure becomes visible in the background, even when the user only sees a simple payment screen.

How Businesses Sometimes Use P2P Transfer Routes

A P2P business context can create confusion because a payment that looks personal on screen may still be linked to a commercial purpose. This is where users need to read the payment setup carefully. A direct transfer between two individuals is different from a payment collected as part of business activity. The interface may look similar, but the payment context changes how the transaction should be understood.

Why Some Businesses Appear to Use Personal Payment Routes

Small sellers, freelancers, tutors, delivery agents, and home-based service providers may sometimes collect money through an individual payment identity. In such cases, the payer may feel like they are making a personal transfer, even though the payment relates to a service, sale, or business arrangement. This usually happens in informal or early-stage business setups.

Why Personal and Business Collections are Not the Same

A personal transfer is a transaction in which one individual pays another for a personal purpose. Business collections work differently because payments require clearer commercial identification, better record handling, and cleaner reconciliation. When a business receives money through a personal route, the payment can become harder to classify and review later.

Where Payment Clarity Becomes Important

The recipient type affects how the payer reads the transaction before approval. A user sending money to a friend usually looks for a personal identity match. A user paying for goods or services should also understand whether the payment is being directed to a business-facing setup or an individual account. This difference supports cleaner payment decisions and fewer interpretation errors.

Personal QR and Business-facing Acceptance are Different

A P2P QR code usually points to an individual recipient, while a business-facing QR is meant for commercial collection. Users should also remember that scanning a QR code is for making a payment, not for receiving money. Both may open within the same app flow, but the purpose behind the payment is not identical. For users, the safest approach is to check who is receiving the money and why the payment is being made before confirming the transfer.

Limitations of P2P Payments

Transfer Limits can Affect Larger Payments

P2P transfers work well for routine amounts, but they may not suit every payment size. App-level and bank-level limits can restrict how much a user can send in a single transaction or within a day.

Failed Transactions can Interrupt the Experience

A transfer may fail due to bank-side issues, app load issues, network problems, or incorrect recipient details. This can create confusion when the payment attempt does not complete as expected.

In some cases, money may be debited before the final status is resolved. When that happens, the user may need to wait for the reversal process to complete under the banking system’s prescribed turnaround timelines..

Internet and App Access Remain Important

P2P payments depend on a working device, app access, and stable connectivity. If any of these fail at the wrong moment, the transfer journey can break down midway.

Payment Context is not Always Clear

Some transfers look personal on screen even when the underlying purpose is commercial. This can affect how users interpret the payment before approval.

Conclusion

P2P transactions have changed how money moves between individuals in India. What once required cash, account details, or a branch visit can now be completed in a direct digital payment flow within moments. That convenience has made person-to-person transfers part of regular financial behaviour, from family support and shared expenses to small-value daily settlements.

The real value of P2P payments, however, does not come from speed alone. It comes from understanding what the transaction is, how it is classified, where it fits in the payment ecosystem, and the checks that must be completed before approval. A user who can correctly identify a personal transfer, verify the recipient carefully, and read the payment context with precision is far less likely to make an avoidable mistake.

The real strength of P2P payments in modern banking lies in this balance. They make money movement easier, but the quality of the transaction still depends on user judgment at the final step.

FAQs

1. What does pending mean in a P2P transaction?In a P2P transaction, pending means the transfer instruction has been created, but the final status is still being processed. The sender may see the amount debited before closure. Users should wait for the final update, check transaction history, and avoid initiating another payment until the status becomes clear.

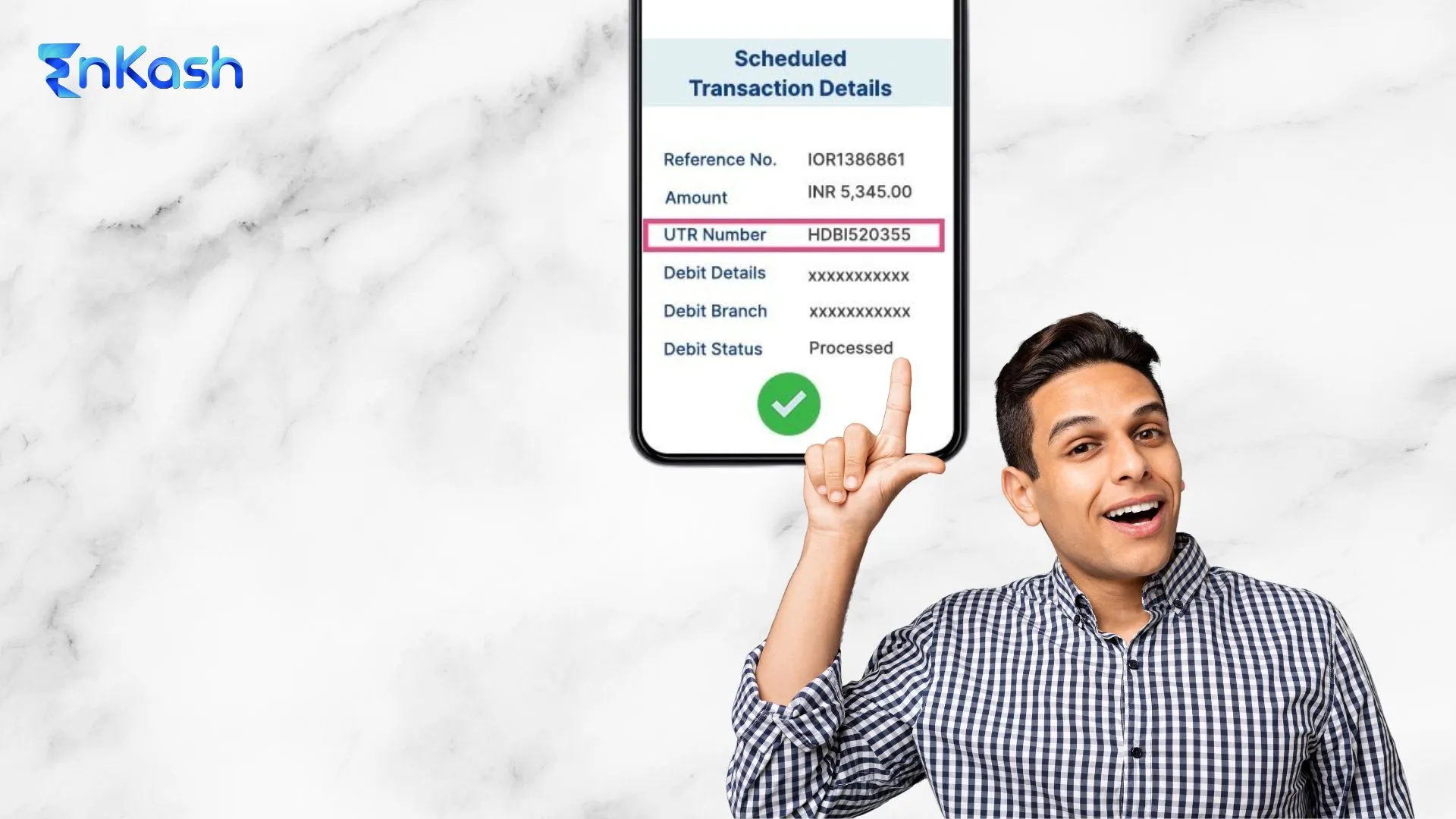

2. How can I confirm a P2P payment was successful?A successful P2P payment usually shows a completed status, a transaction reference number, and a matching debit entry in the app or bank history. Users should also verify the recipient name and amount together. A screenshot alone does not confirm completion if the transfer status still shows pending.

3. What happens if a P2P transfer goes to the wrong person?If a P2P transfer reaches the wrong person, the sender should immediately record the reference number, date, amount, and recipient details, then contact the app or bank support channel. Recovery is not automatic in every case and may depend on the receiving bank, the beneficiary, and the complaint review process. Fast reporting improves the chances of timely action.

4. What is a collect request in a P2P payment?In a P2P payment, a collect request is a payment request sent to the payer for approval. Money moves only after the payer authorises it. Users should read the requester's name, amount, and purpose carefully. Approving an unfamiliar collect request can result in an unintended debit from the account.

5. What should I verify before approving a P2P transfer?Before approving a P2P transfer, users should verify the recipient name, amount, transfer route, and payment purpose shown on the screen. These checks help confirm that the money is being sent to the intended person. Careful review before approval is one of the strongest safeguards against avoidable transfer mistakes.

6. Why do P2P payment limits vary across apps?P2P payment limits can vary because banks, payment apps, and user account settings may not apply the same thresholds. A sender may, therefore, see different caps across platforms. These differences usually come from operational controls, account-level settings, or bank-side rules, even when the broader transfer framework appears similar.

7. Can a P2P QR code send money to the wrong receiver?A P2P QR code can still lead to the wrong receiver if the sender scans the wrong code or ignores the name displayed before approval. The QR helps identify the payment destination, but it does not remove the need for verification. The recipient's name remains the final, most important checkpoint.

8. Why is transaction history important in P2P payments?Transaction history helps users check whether a P2P payment was completed, failed, reversed, or remains under review. It also records the amount, date, recipient details, and reference number. This information becomes important when users need to verify a transfer, settle confusion, or raise a payment-related complaint through support.

9. Can repeated P2P transfers still result in mistakes?Repeated P2P transfers can still lead to mistakes when users rely on memory and skip verification. A familiar contact or payment route should not replace checking the recipient name, amount, and transfer intent on the screen. Errors in repeat payments usually happen because attention drops during routine transactions, not because the system changes.

10. What should I keep ready before reporting a P2P payment issue?Before reporting a P2P payment issue, users should keep the transaction reference number, amount, date, recipient details, and payment status ready. A screenshot of the transaction page can also help. Clear records support faster complaint review, while missing details can delay investigation and make the issue harder to resolve.

Official Sources:

RBI retail payments and customer-protection guidance

NPCI UPI product page

NPCI UPI safety guidance

RBI harmonised TAT and compensation rules for failed or delayed transactions