What is a UPI Wallet and How Does It Work?

Digital payments in India have become seamless with UPI and wallet-based apps. While UPI usually needs a bank account, prepaid UPI wallets bridge the gap for users without one. A UPI Wallet is part of this change. Some apps offer wallet services alongside UPI. While UPI itself requires a linked bank account, prepaid wallets allow you to transact digitally without one.

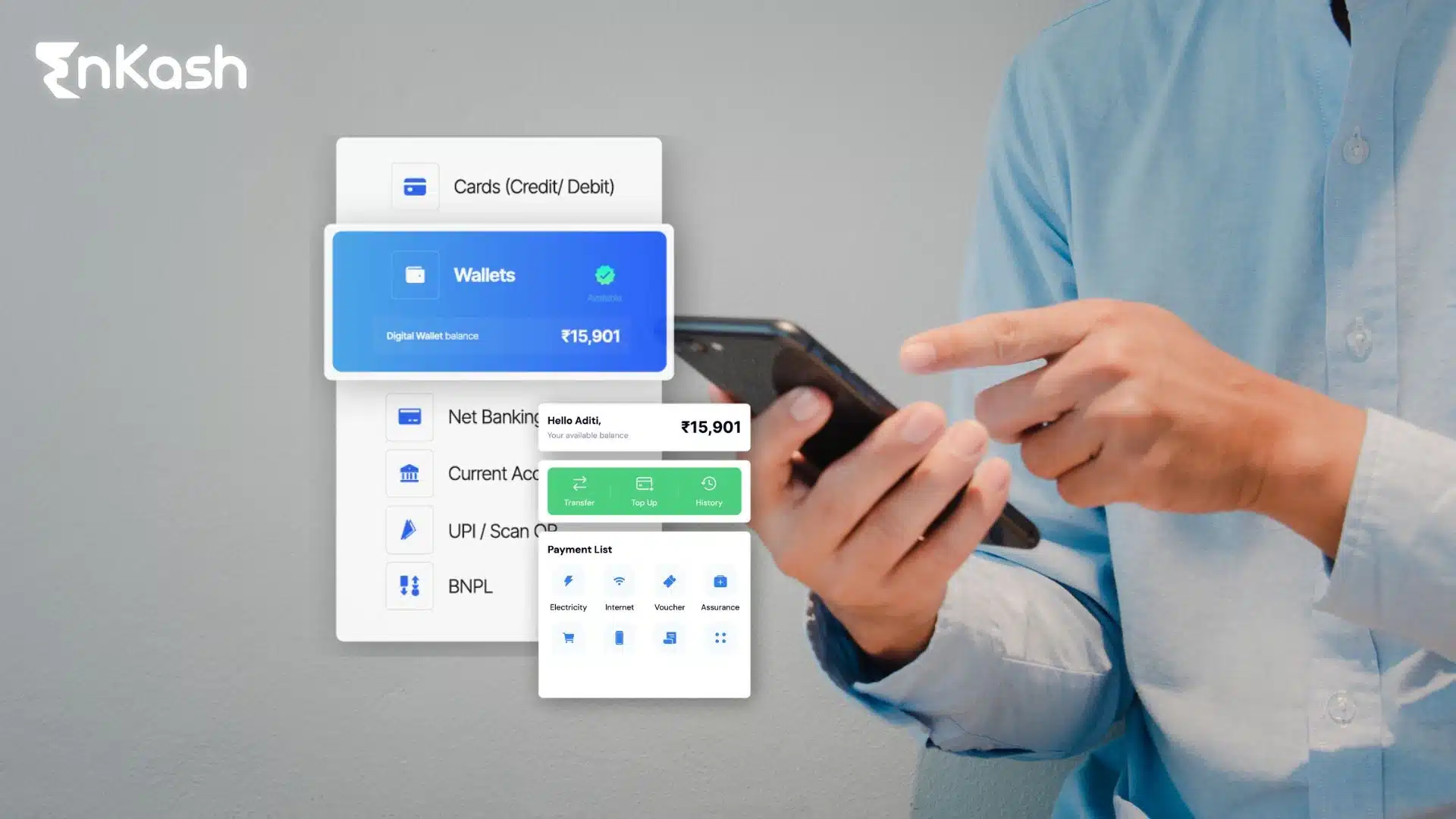

In simple terms, a UPI Wallet works like a small digital purse that holds money electronically. You can load funds into it using cash deposits, a card, or another payment method. Once the wallet is loaded, it can be used to pay for goods, transfer money to someone, or even

make utility payments. It removes the need to visit a bank or carry cash.

A wallet app may offer

UPI features for banked users and prepaid wallet features for unbanked users. This makes it useful for those who want to handle online payments without bank account access. It also helps small vendors, students, and independent workers who may prefer a digital option over traditional banking.

UPI wallet apps have grown rapidly because they’re easy to use and quick to set up. The setup is quick, transactions happen in real time, and payments are confirmed instantly. Each wallet works through a secure network that verifies the identity of the user and ensures safe money transfers.

As more people look for ways to manage digital wallets without bank account options, these platforms provide a reliable bridge between cash and

digital payments. They make financial access simple, fast, and safe for everyday use.

Understanding the Wallet Concept in a UPI-Enabled Environment

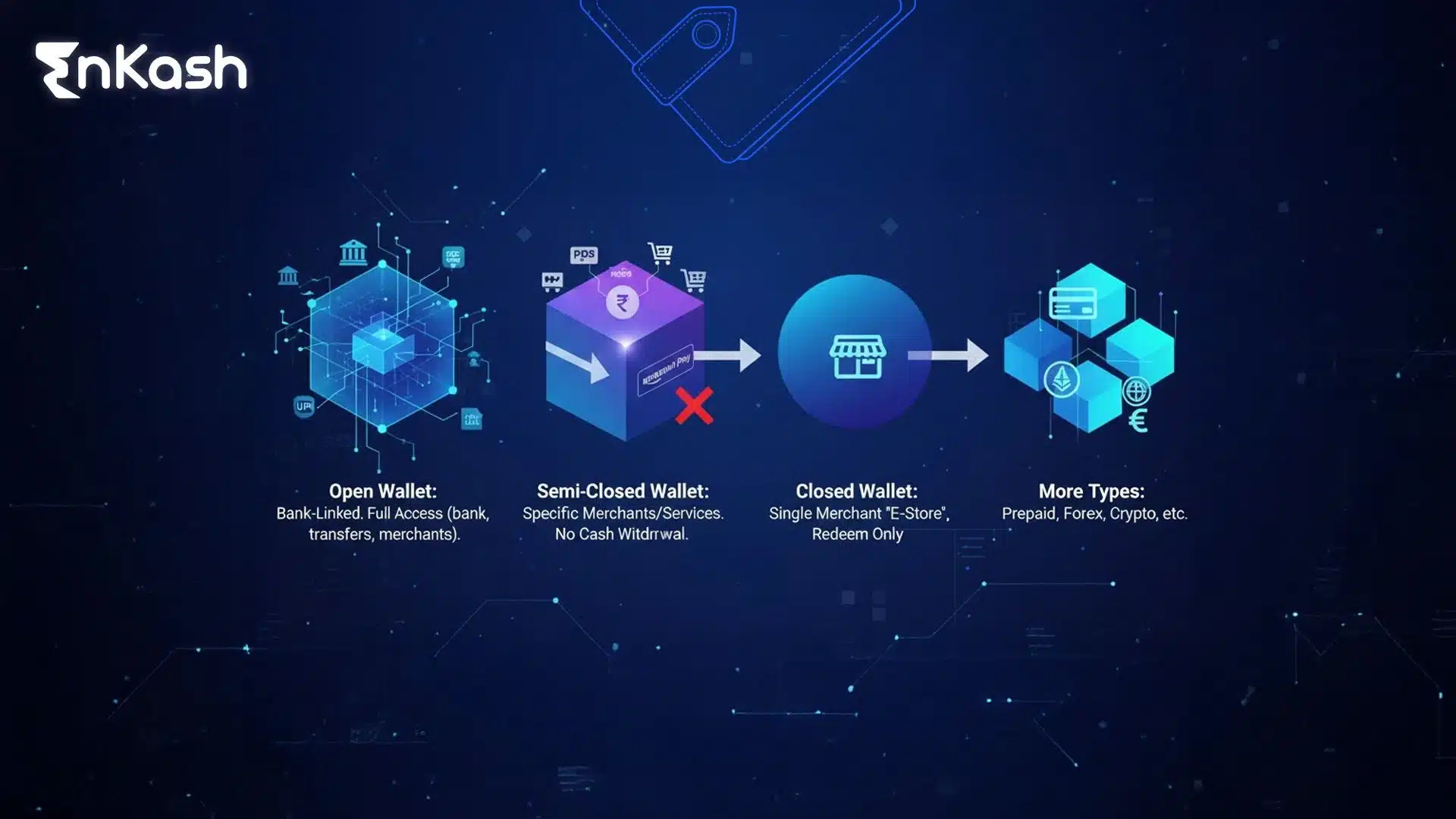

Difference Between a Digital Wallet and a UPI Wallet

A wallet stores money digitally, allowing users to pay and transfer funds without cash. A digital wallet keeps a prepaid balance that you load before spending. A UPI Wallet works differently. It is built on a real-time payment system that allows instant transfers between users and merchants. This structure brings speed and transparency to digital transactions.

How a UPI Wallet Without Bank Account Helps Users

Many people prefer managing digital money instead of visiting a bank branch. An e-wallet without a bank account option makes this possible. It allows users to store funds securely and make quick payments online. This approach supports small traders, gig workers, and people in remote regions who want to use digital payments safely.

Security and Verification in Mobile Wallets in India

Every licensed wallet provider must complete Know-Your-Customer (KYC) verification as per RBI guidelines. This process confirms user identity and prevents misuse. Once verified, users can send and receive money freely. These checks make the system transparent and trusted for daily transactions.

A digital wallet without a bank account feature connects cash users to the growing digital economy. With just a smartphone, anyone can manage payments and track spending. This shift promotes financial inclusion and reduces the need for physical cash.

Mechanics of a UPI Wallet: How Funds Move Without a Full Bank Account

Set Up and User Verification

To start using a UPI Wallet, users first install a payments app and create an account. They verify their identity and set a security code for protection. The process is simple, guided, and safe for new users.

Adding and Managing Funds

Once the wallet is ready, money can be added using a debit card, prepaid card, or transfer from another user. Some wallets also allow small cash deposits through partner outlets. These steps make online payment without bank account access practical and easy.

How UPI Wallet Apps Handle Transactions

A UPI Wallet app connects the user, the payment provider, and the merchant in one secure network. When someone makes a payment, the wallet deducts the amount from the stored balance and sends it to the receiver. Every transaction is logged for complete transparency.

Why a Payments App Without a Bank Account Is Useful

A payments app without a bank account follows a prepaid format. You can only spend what you have loaded. This structure prevents overspending and helps people manage money responsibly. It suits users who prefer predictable spending habits.

Secure Transfers and Settlement Process

Wallet operators use encrypted systems to ensure safe transfers. Each transaction goes through multiple security checks before completion. This is how a UPI Wallet Without Bank Account provides a fast and trustworthy payment experience without the need for traditional banking.

By linking cash to digital payments, a digital wallet without a bank account gives users control over how they move money. Payments happen instantly, securely, and without complication, making digital spending a part of everyday life.

Key Features and Benefits of Using a UPI Wallet Without a Bank Account

Simple Access and Quick Setup

A UPI Wallet is built for ease of use. Anyone with a smartphone can download a wallet app, verify identity, and begin making payments within minutes. This simplicity allows users to manage digital money without needing to visit a bank or handle paperwork.

Inclusive Payments for All Users

A digital wallet without a bank account feature supports people who do not have access to traditional banking. It allows students, small vendors, and independent workers to receive payments instantly and pay for services with convenience. This digital access brings more people into the financial system and reduces dependence on cash.

Instant Transfers and Real-Time Confirmation

Each transaction through a UPI Wallet happens instantly. The payment is processed and confirmed within seconds. Users can send, receive, and track money in real time. This creates confidence and helps merchants and individuals handle daily payments smoothly.

Control Over Spending and Budgeting

A payments app without a bank account follows a prepaid structure. You can load a specific amount and spend only what you have added. This system promotes better money discipline, avoids overspending, and helps users keep track of their budget through transaction records.

Safe and Verified Transactions

Security is a key part of every UPI Wallet. Each payment requires user verification through a secure code or biometric check. Wallets use

encryption to protect financial data and prevent misuse. These measures make every transaction safe and reliable for users.

Flexibility Across Daily Uses

A digital wallet can be used for shopping, utility bills, travel bookings, or local store payments. It supports QR scanning and virtual payment addresses for quick transfers. The convenience of handling all these payments from one app makes the experience seamless.

Growing Network of Acceptance

Many merchants and service providers now support wallet-based payments. This growth has made a UPI Wallet Without a Bank Account practical in every setting—from small stores to online platforms. The system works efficiently and adapts to different payment needs.

Contribution to a Cash-Light Economy

By offering a UPI wallet without a bank account, these platforms encourage people to move toward digital transactions. They simplify how money is exchanged and reduce the use of cash. This shift builds a smoother and more transparent payment culture.

Limitations, Risks, and Compliance Considerations

Transaction Limits and Usage Restrictions

A UPI Wallet operates under certain usage limits set by regulators. Prepaid wallets are subject to RBI limits — ₹10,000 per month for minimum-KYC and ₹2 lakh for full-KYC wallets (as of 2024). These limits control how much money can be added, held, or transferred within a given period. For a digital wallet without a bank account, this ensures security but also means users cannot store or send very large amounts. Understanding these limits helps in planning everyday spending.

KYC Rules and Compliance Checks

Before full access is allowed, users must complete identity verification. This process, called KYC, is mandatory for all UPI wallet apps. It ensures that the wallet is used for legal and safe purposes. Completing KYC helps prevent misuse, fraud, and money laundering while protecting both users and service providers.

Data Security and Privacy Concerns

Digital payments rely on user data and transaction details. A payments app without a bank account must use secure encryption to keep that information private. Even with strong protection, users need to stay cautious by keeping their access codes safe and using trusted apps only.

Risk of Fraud and Unauthorised Access

Any digital system can face attempts of misuse. Some people may try to trick users through fake messages or links. A genuine UPI Wallet always sends alerts and transaction updates directly in the app. Users should verify all payment requests and never share confidential codes to stay safe.

Dependence on Network and System Reliability

Every digital wallet depends on a stable internet connection. In areas with poor connectivity, transactions may take longer or fail to process. Although modern systems are improving, users should ensure that their connection is steady before making important payments.

Legal and Regulatory Oversight

A UPI wallet without a bank account must follow financial regulations and security standards issued by the central authority. These rules define limits, transaction types, and consumer rights. Regular checks make sure wallet companies remain transparent and accountable to users.

Limited Access to Traditional Banking Services

A wallet gives access to payments but does not offer full banking features like savings accounts or interest benefits. For many users, a digital wallet without a bank account is ideal for day-to-day transactions, but it cannot replace a full-service bank for long-term financial goals.

Importance of Awareness and Safe Practices

Users play a key role in keeping digital transactions secure. Reading terms, updating apps, and avoiding public networks for payments are small steps that make a big difference. With responsible use, a UPI Wallet remains one of the safest and most efficient payment tools available.

How to Choose a UPI Wallet App Without Bank Account – Checklist for Users

Check for Regulation and License

The first thing to verify before using any UPI Wallet is whether the company holds a valid license. A trusted provider operates under strict financial supervision and follows compliance guidelines. Always choose a wallet that is transparent about its regulatory status and clearly displays its authorization details on the platform.

Review Credibility and User Reputation

User experience reveals how reliable a wallet truly is. Before installing, check reviews, download history, and overall reputation. Well-known UPI wallet apps with a stable record of secure operations are safer choices. Avoid applications with poor feedback or unclear ownership details.

Understand KYC and Security Measures

Every digital wallet requires identity verification. A clear and simple KYC process is a good sign that the provider follows safety protocols. Look for features like PIN protection, biometric login, and transaction alerts. These add layers of protection and make your payments app without a bank account more secure.

Compare Fees and Transaction Costs

Some wallets charge small fees for loading money, transferring funds, or withdrawing balances. Read the fine print carefully. The best UPI Wallet will have transparent pricing and minimal hidden costs. Choose one that fits your usage frequency and transaction size.

Examine Loading and Withdrawal Options

A flexible e-wallet without a bank account gives several ways to load funds. These can include cash deposits, card transfers, or other wallet-to-wallet transfers. Some even allow linking a minimal account for easier fund management. Flexibility in fund movement makes the wallet more convenient for daily use.

Look for Interoperability and Merchant Reach

A good UPI Wallet Without Bank Account connects with major merchants, service providers, and utilities. The wider the network, the more practical it becomes. Interoperability also means you can send money or make purchases even when the receiver uses a different wallet provider.

Evaluate Customer Support and Dispute Resolution

Strong customer service reflects reliability. In case of failed transactions or technical issues, timely assistance matters. Before choosing any digital wallet without a bank account, check how users can raise complaints and the average resolution time offered by the provider.

Read the Terms and Conditions Carefully

Every wallet provider outlines specific rules for usage, refunds, and account closure. Take a few minutes to go through these details. It helps you understand limits, security rights, and what happens if your account remains inactive. A transparent policy signals a trustworthy digital wallet provider.

Focus on Ease of Use and Interface

An effective UPI wallet without a bank account app should be easy to navigate. Clear instructions, simple menus, and

quick responses make everyday payments smoother. A clean design helps users of all backgrounds manage money without confusion.

Confirm Data Privacy and Storage Standards

Before adding funds, ensure the wallet stores your information securely and does not share it with third parties without consent. Providers that follow proper encryption and privacy policies are safer choices for long-term use.

Use Cases and Real-World Examples of UPI Wallet Usage Without Bank Accounts

Everyday Peer-to-Peer Transfers

A UPI Wallet allows users to send money instantly to friends, family, or coworkers. Instead of exchanging cash, one can transfer small or large amounts within seconds. This feature makes it easier for people who do not have bank accounts to handle daily payments digitally. It is safe, quick, and transparent.

Small Business and Vendor Payments

Street vendors, delivery agents, and local shopkeepers benefit greatly from a digital wallet without a bank account. Customers can scan a QR code and pay for goods directly. This reduces the need for physical cash handling and gives sellers a simple digital record of their earnings. For many small businesses, it has replaced the need for cash transactions entirely.

Utility Bills and Service Payments

Many UPI wallet apps let users pay electricity bills, mobile recharges, or online subscriptions directly from the wallet balance. This feature saves time and effort, especially for those who do not have online banking. The process is fast and provides instant confirmation for every payment.

Public Transport and Ticket Bookings

In cities where cash payments were once standard, commuters now use UPI Wallets for tickets and passes. Wallet-based payments make travel smoother by reducing queues and improving transaction speed. For people without bank accounts, it provides a simple and traceable way to pay for daily commutes.

Freelancers and Gig Workers

Freelancers and small contractors use UPI wallets without a bank account setup to receive payments from clients. This is helpful for those who work independently or on short projects. It allows them to receive funds quickly without waiting for a bank to process transfers.

Online Shopping and Digital Marketplaces

A digital wallet can be used on e-commerce platforms, food delivery apps, or entertainment sites. Users can make purchases or pay service providers directly from the wallet balance. Each transaction is protected through verification codes and secure gateways.

Micro and Subscription Payments

Wallets support small recurring transactions like app renewals or donations. With a payments app without a bank account, users can set reminders or make automatic deductions from their stored balance. It makes regular payments manageable and transparent.

Local Economy and Cashless Drives

As more merchants and customers use UPI Wallets, digital acceptance grows in small markets and rural areas. This shift supports a connected economy where payments are simple and traceable. The use of wallets has made it possible for unbanked users to take part in modern commerce with ease.

Final Thoughts

A UPI Wallet has changed how people handle money by making digital payments simple, fast, and safe. It allows anyone to send, receive, and store funds without needing a traditional bank account. The system supports individuals, small businesses, and daily users who prefer convenience over complex banking. With growing trust and wide merchant acceptance, UPI wallet apps are building a stronger digital economy. As technology improves and security becomes smarter, these wallets will continue to make online payments without a bank account easier and more reliable for everyone.

FAQs

1. How does a UPI Wallet work without a linked bank account?

A UPI Wallet allows users to store digital money in a prepaid form. Instead of linking to a full bank account, funds are added through cards, transfers, or cash deposits. The wallet balance can then be used to send or receive payments instantly. It functions like a secure virtual purse for digital transactions.

2. Can I receive money directly into my UPI Wallet?

Yes. Once your UPI Wallet is active and verified, anyone can transfer money to your wallet using your unique ID or QR code. The amount reflects in your wallet balance immediately, and you can use it for shopping, bill payments, or transfers to other wallet users.

3. Is it possible to withdraw cash from a UPI Wallet?

Some wallet providers allow withdrawals through partner stores or ATMs, while others restrict funds to digital use only. This is available only for open-loop wallets with full KYC, not for closed or semi-closed types. Users should check their wallet’s policy. If supported, you can convert part of your digital wallet balance into cash by following the provider’s withdrawal process safely.

4. What are the limits for sending or storing money in a UPI Wallet?

Limits vary by provider and type of wallet. A basic UPI wallet without a bank account might allow smaller monthly transfers, while a full KYC wallet can handle larger values. These caps are designed to prevent misuse and keep digital transactions secure.

5. Are transactions through a UPI Wallet safe?

Yes. UPI Wallets use encryption, PINs, and secure servers to protect every payment. Each transaction requires authentication, and users receive instant alerts for any activity. Choosing a licensed wallet provider and keeping login credentials private adds extra safety to digital payments.

6. What happens if I lose my phone with a UPI Wallet installed?

Losing your phone does not mean losing your wallet balance. You can block access by contacting the wallet provider’s support team. They verify your identity and disable the old account. Once secured, you can log in again on another device and continue using your digital wallet safely.

7. Can I use my UPI Wallet to pay international merchants?

Most UPI wallet app transactions are limited to domestic payments. However,

NPCI is piloting cross-border UPI with countries like Singapore and the UAE. These services allow users to make small international purchases, but they depend on regulatory permissions and wallet type. Always check availability before attempting global payments.

8. Do UPI Wallets charge any hidden fees or commissions?

Basic transactions are usually free, but some wallets may apply small charges for loading funds, withdrawals, or transfers beyond certain limits. It is best to review the provider’s fee policy. Reputable UPI Wallet platforms are transparent about charges and display them before you confirm any payment.

9. What is the difference between a prepaid wallet and a UPI-linked account?

A prepaid wallet stores a fixed amount that users manually load, while a UPI-linked account connects directly to a bank balance. The wallet has limits on usage, but it is easier to set up. A UPI-linked account offers broader access to funds but requires a full banking relationship.

10. Can a UPI Wallet be upgraded later to link a bank account?

Yes. Most providers allow users to convert their e-wallet into a bank-linked UPI account. This process involves completing full KYC and linking existing bank details. After the upgrade, users can enjoy higher limits, direct transfers, and access to additional payment features under the same platform.