Accounting errors can begin with a small lapse and end with a much larger reporting problem. A missed vendor bill, a wrong entry in an expense head, or an invoice posted to the wrong ledger can distort profit, liabilities, tax working, and internal reporting in ways that take time to unwind. For finance teams handling reimbursements, vendor payouts, GST records, and month-end closing together, accuracy depends on disciplined recording at every step. Books must support reliable review, statutory compliance, and clean decision-making across the business.

This is why understanding accounting errors early is essential. The sections ahead explain what they mean, where they arise, how the main error categories differ, and how stronger process control reduces the risk of a costly wrong entry entering the books.

What is an Accounting Error

An accounting error is an unintentional mistake made during the handling of a financial transaction inside the books of account. The issue may appear when data is first captured, when amounts are entered into the journal, when balances are posted into the ledger, or when figures are carried forward for reporting. In each case, the transaction is real, but the recorded result is inaccurate.

This kind of mistake is different from fraud because there is no deliberate attempt to mislead. The error comes from oversight, an incorrect understanding, a posting failure, or weak recording discipline. A number may be entered incorrectly. A transaction may be classified under the wrong account head. An amount may be posted on the wrong side. A supporting document may be received, yet the related accounting step may remain incomplete.

The result is not limited to untidy books. Financial statements can reflect the wrong expense, revenue, asset, or liability position. Internal reports can lose reliability, and reconciliation work can become harder than it should be. Once that happens, finance teams spend time tracing entries that should have been correct at the first stage. Clear accounting treatment, accurate posting, and disciplined review are what keep the records dependable.

Why Accounting Errors Matter

Accounting errors affect more than bookkeeping accuracy. Incorrect records can influence management reporting, statutory filings, tax calculations, audits, lender reviews, investor reporting, and regulatory compliance.

For example:

- An understated expense can overstate profit

- A missed liability can understate obligations

- Incorrect GST treatment can lead to tax mismatches

- Wrong asset classification can affect depreciation calculations

This is why accounting standards, audit procedures, and internal financial controls place significant emphasis on accurate transaction recording and review.

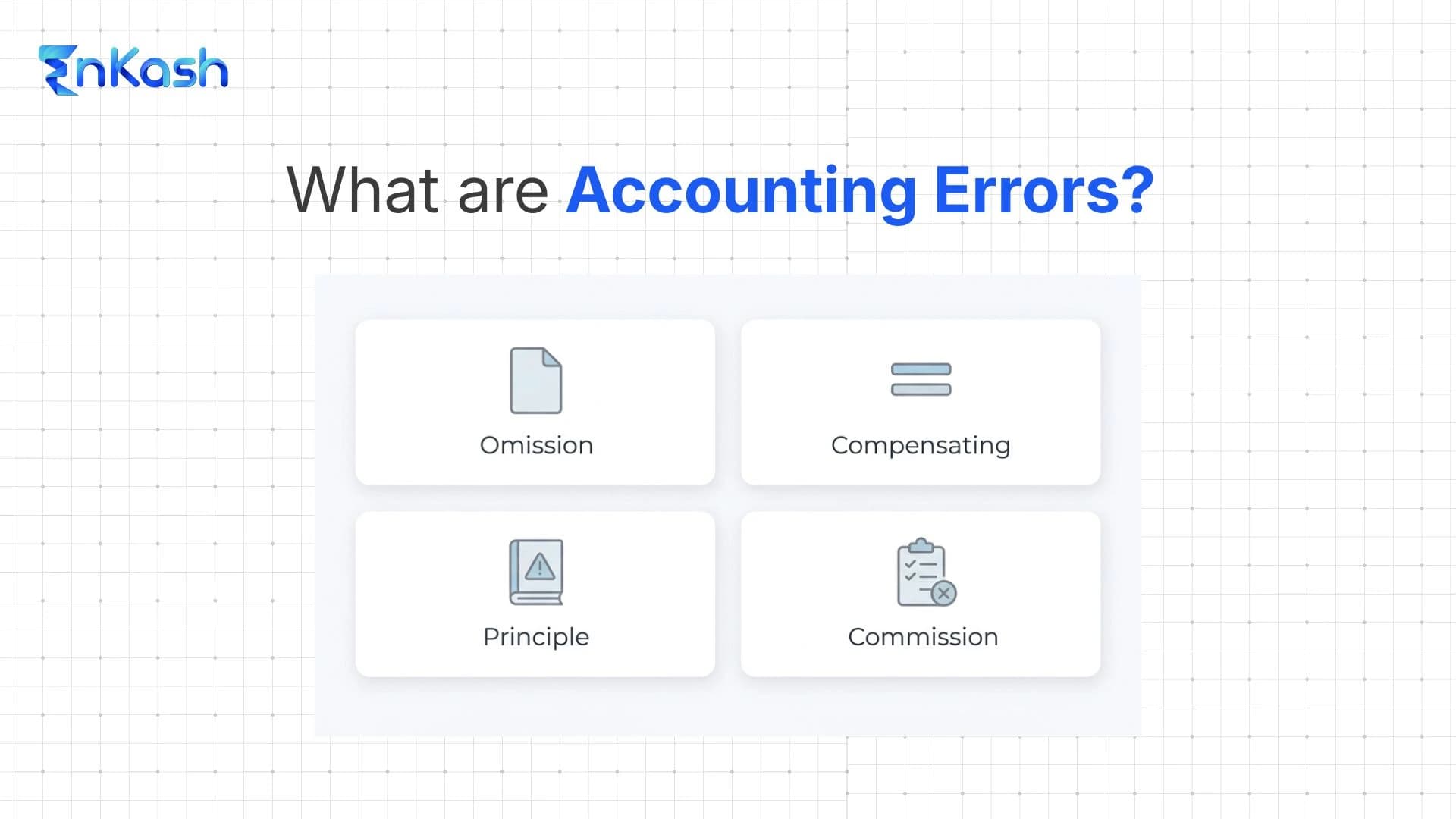

Types of Accounting Error

Accounting mistakes do not enter the books through a single route, and their effect is not uniform. A transaction may be left out entirely, classified under the wrong account, recorded incorrectly, or concealed within balancing defects that are harder to trace. In some cases, a second mistake masks the first and delays detection. A clear view of the types of accounting errors helps finance teams isolate the issue faster and respond with the right correction.

Error of Omission

An omission error occurs when a transaction, or part of it, does not enter the accounting records at all. This can happen at the first stage, such as when a vendor invoice is received but never booked, or later in the cycle when the journal entry is made but the posting to the ledger remains incomplete. A complete omission leaves the transaction entirely outside the books. A partial omission records only one side of the process, leaving the other unfinished.

This kind of error leaves a blind spot in the records. Costs can appear lower than the actual outflow. Outstanding dues may be recorded at a level below their true value. Input tax credit claims and supporting GST records can be affected when the underlying invoice is never recorded in the books. In businesses managing frequent purchases, staff claims, and routine operating spend, a missed transaction can alter monthly numbers quietly and delay accurate review.

Error of Principle

An error of principle arises when the accounting treatment itself is wrong. The entry may be posted on both sides and recorded neatly, yet the transaction has been placed under an incorrect head because the underlying rule was misunderstood. This is a classification issue, not a clerical lapse.

A typical case involves recording the purchase of equipment as day-to-day expenses rather than placing it in the capital account. Another appears when routine repairs are added to asset cost without proper accounting support. Errors like these distort reported profit, asset balances, and the broader financial position over time. They also reduce the value of internal analysis because the figures may appear orderly even though the underlying classification is incorrect. This type of mistake calls for stronger accounting judgment, because the problem lies in faulty treatment rather than a missing record.

Error of Commission

For those asking, “What is the error of commission?”: It refers to a mistake that occurs after a transaction has been entered into the accounting records. The entry is made, but some part of the bookkeeping process goes wrong during recording, posting, totaling, carry-forward, or balancing. The transaction itself is genuine, though the way it is handled in the books is incorrect.

This can include posting an amount to the wrong supplier account, entering an incorrect figure, using the wrong ledger entry, or carrying forward a balance inaccurately. An error of duplication is generally treated as a form of error of commission because a transaction is recorded more than once. A single wrong entry of this kind can affect expense totals, payable ageing, employee claims, or tax figures. Commission errors are operational in nature and tend to grow when entries move through several hands or across disconnected records.

Compensating Errors

Compensating errors occur when two or more mistakes cancel each other out numerically. The books remain inaccurate, though the overall discrepancy may not be apparent immediately because one error offsets another. An expense may be understated in one account and overstated by the same amount in another. A ledger may be over-debited while a separate ledger is over-credited by an equal figure.

This type of error is very risky because balanced figures can give a misleading sense of accuracy. The books may appear in order even when individual postings still contain mistakes. Compensating errors are harder to identify because the totals do not immediately signal a problem. Their presence shows why finance teams need closer transaction review rather than relying solely on overall agreement in the records.

How to Detect Errors in Accounting

Error detection begins with a disciplined review process. Once transactions enter the books, finance teams need structured checks that examine numerical accuracy, supporting records, ledger consistency, and reconciliation quality. Each check serves a separate purpose within the review cycle. Reliable detection, for this reason, depends on layered verification across the accounting process rather than reliance on a single control point.

Check the Trial Balance for Visible Mismatches

The trial balance is one of the primary arithmetic checks used to identify posting and balancing errors.. It helps identify one-sided postings, wrong totaling, and balance carry-forward issues that disturb the debit and credit agreement. A trial balance error can point toward posting defects, ledger imbalance, or calculation mistakes that entered the books during routine processing. This check helps identify visible breaks in the accounting flow before deeper review begins.

Match Entries with Supporting Documents

Ledger entries should be checked against invoices, bills, vouchers, bank advice, debit notes, and reimbursement records. This step helps uncover missing bookings, duplicate entries, amount differences, and unsupported claims. In practical finance work, document matching is where many hidden faults come to light, as the source record reveals what the ledger failed to capture correctly.

Use Ledger Review and Variance Analysis

A close ledger scan can reveal defects that raw totals do not explain. Duplicate vendor names, unusual negative balances, sudden spikes in expense heads, and unexplained month-end adjustments deserve attention. Period comparison also helps. When one category moves sharply without an operational reason, the books may contain a posting defect, classification problem, or duplicate charge.

Perform Reconciliation Across Books and External Records

Reconciliation tests the books against independent records. Bank reconciliation checks whether cash and banking entries agree with the statement movement. Vendor reconciliation compares payable balances with supplier records. Expense and tax reconciliation help identify mismatches that remain hidden inside internal ledgers. This stage is critical because it verifies recorded figures against external evidence, thereby strengthening and making detection more reliable.

How to Avoid Errors in Accounting

Reducing accounting mistakes begins before a transaction reaches the books. A stronger process depends on clear steps, defined responsibilities, and checks that catch issues before they are posted. Control improves when teams work with documented procedures, approval hierarchies, and maker-checker review. The Companies Act, where applicable, requires companies to maintain proper books of account and supporting records, including electronic records.

Standardize Entry Rules and Account Mapping

A well-structured chart of accounts provides finance teams with a clearer base for accurate bookkeeping. Each ledger head should serve a clear purpose across expenses, tax entries, cost centres, and reporting lines. When the accounting structure is clearly laid out, classification becomes more consistent and reporting becomes easier to trust. This creates greater consistency in the books and improves the quality of internal financial review.

Build Approval Controls Before Posting

Review before posting helps stop incorrect entries from moving deeper into the accounting cycle. Stronger control comes from clear authorization rules, separation of responsibilities, and maker-checker review for payments and expense-related transactions. This is useful across reimbursements, procurement bills, travel claims, and recurring operating spend, where document checks and approval verification must occur before final accounting treatment is recorded.

Reduce Dependence on Manual Spreadsheets and Paper Trails

Records can be maintained electronically, and supporting documents must be properly preserved for review and audit. Digital recordkeeping makes it easier to store, retrieve, and present transaction support when needed. When finance data flows through disconnected sheets, involves repeated manual transfers, or is scattered across files, traceability weakens, and reviews take longer. A centralized digital record structure improves document control and supports a cleaner finance process.

Train Teams on Accounting Treatment and Documentation Discipline

Accurate books depend on proper classification, complete support, and consistent transaction handling. Finance teams need clear guidance on ledger usage, documentation standards, and review procedures. Submission quality also affects accounting accuracy, since the books rely on the information that enters the process at the start. Better process discipline strengthens financial control and reduces avoidable correction work later.

How EnKash Helps Reduce Manual Errors with Expense Management

EnKash positions its expense management system as a way for businesses to control expenses, track spending in real time, manage reimbursements, and streamline finance workflows. The platform includes centralized expense tracking, approval workflows, policy controls, accounting sync, API connectivity, and automated journal entry mapping. These features are designed to improve process control, strengthen expense governance, and support more consistent financial reporting.

Centralized Expense Capture Improves Record Completeness

The system captures expenses digitally and connects them with approvals and reports. It also maintains digital records tied to submissions, approvals, edits, receipts, and timestamps. With a centralized workflow, finance teams can review claim details and supporting documents in one place before reimbursement or accounting action begins.

Automated Policy Checks Reduce Invalid Submissions

The platform includes policy validation, budget controls, and automated approvals. It also checks duplicate claims, incorrect reimbursements, and unapproved spending. These controls help screen expense submissions earlier in the workflow, which reduces invalid claims before they move into finance processing.

Approval Visibility Supports Stronger Review

Each transaction leaves a digital trail linking submission, approval, edits, receipts, and timestamps. The approval workflow gives finance teams a clearer view of claim movement and supporting records during review. This improves visibility across the expense cycle and supports stronger internal checking.

Integration Support Reduces Manual Re-Entry

The expense management system connects with accounting tools such as Zoho Books, Tally, and QuickBooks. It also supports APIs, webhooks for real-time sync, and automated journal entry mapping. These features help move expense data into accounting workflows with greater consistency, support faster ledger posting, and simplify financial reporting.

Summing Up

Accounting errors can begin with an overlooked step, an incorrect classification, or a posting defect that passes into the records unnoticed at first. Each error type affects reporting differently, making it important for finance teams to understand both the source of the error and the controls required to contain it. Strong detection comes from disciplined review. Strong prevention comes from tighter process design, better record quality, and clearer approvals. When expense workflows, supporting documents, and accounting routines are managed with greater structure, businesses spend less time on corrections and work with financial records they can trust more confidently.

FAQs

1. What are accounting errors?

Accounting errors are unintentional mistakes made during the recording, classification, posting, totaling, or carrying forward of financial transactions. These mistakes can affect profit, expenses, liabilities, asset values, and the accuracy of financial reporting.

2. What are the main types of accounting errors?

The main types of accounting errors are omissions, principles, commissions, and compensating errors. Each type affects the books differently and requires a different method of detection and correction.

3. What is an error of omission in accounting?

An omission error happens when a transaction, or part of it, is left out of the accounting records. This can lead to understated expenses, missing liabilities, incomplete records, and inaccurate reporting.

4. What is the error of commission?

Error of commission refers to a mistake made during recording, posting, totaling, or balancing a transaction that has already been entered into the books. The transaction exists, though the bookkeeping treatment is incorrect.

5. What is an error of principle in accounting?

An error of principle occurs when a transaction is recorded under the wrong accounting treatment. This happens when classification is incorrect, such as recording a capital expense as a routine revenue expense.

6. What are compensating errors?

Compensating errors are two or more accounting mistakes that offset each other in value. The books may appear balanced overall, though individual entries remain inaccurate and still require review.

7. What is an error of duplication in accounting?

An error of duplication occurs when the same transaction is recorded more than once in the books. This can inflate expenses, purchases, reimbursements, or liabilities and create incorrect account balances.

8. How can accounting errors be detected?

Accounting errors can be detected through trial balance checks, ledger scrutiny, document matching, bank reconciliation, vendor reconciliation, and review of supporting records. Strong detection depends on layered checks across the accounting process.

9. What does a trial balance error mean?

A trial balance error occurs when the debit and credit totals do not match. This may result from incorrect postings, totaling errors, one-sided entries, or balance carry-forward issues.

10. How can businesses avoid accounting errors?

Businesses can reduce accounting errors by using defined entry rules, approval controls, proper documentation, regular reconciliation, staff training, and digital workflows that reduce manual handling across expense and accounting processes.