Trade credit helps sales move, but it can also lock cash inside receivables for weeks or months. When working capital is tight, businesses often look for a funding route linked to sales instead of fresh short-term debt. In this blog, you will find a clear explanation of bill discounting, the accounting treatment of year-end rebates, the different structures used in practice, the process flow, supporting documents, the calculation method, the platform landscape, and the benefits of early receivable funding.

Bill discounting facilities vary across banks, NBFCs, fintech platforms, and TReDS participants. Eligibility, pricing, recourse terms, documentation, and turnaround times differ by provider. Businesses should review agreements carefully and seek professional advice where required.

What is Bill Discounting

Bill discounting is a receivables-finance arrangement in which a business raises money against an accepted bill or invoice before the due date, after the financier deducts a discount charge for the credit period. In simple terms, bill discounting is about unlocking cash from a credit sale before the buyer actually pays. The structure commonly involves three core parties: the seller that supplied goods or services, the buyer that owes payment, and the financier that provides early funds.,

A receivable enters the discounting cycle when the seller offers it for funding before maturity, turning it into a bill under discount. The financier advances the net amount upfront and recovers the full bill value on maturity under the agreed structure. In trade-finance usage, a credit bill meaning refers to a usance or time bill that carries a credit period before payment falls due. This is why the quality of the underlying sale, the buyer’s acceptance, and the payment term all influence whether the bill can be discounted and how it will be priced.

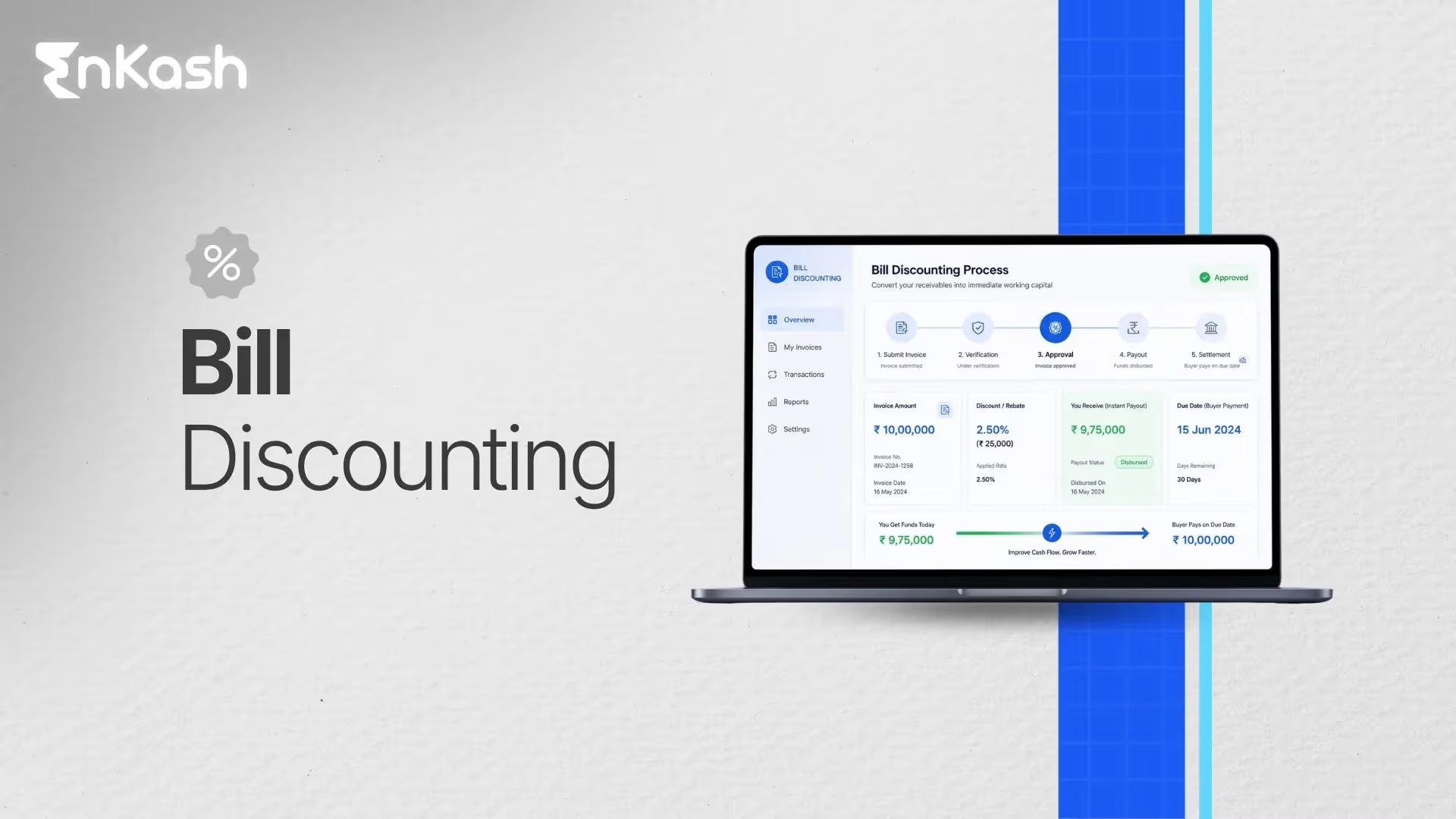

Bill Discounting Example

A simple bill discounting example makes the concept easier to read.

Suppose a seller raises a bill for ₹10,00,000 to a buyer with a 60-day credit period. The buyer accepts the bill, and the seller approaches a financier for early funding. If the financier agrees to discount the bill at 12% per annum, the 60-day discount works out to about ₹19,726. The seller therefore receives about ₹9,80,274 upfront, subject to any additional processing charge agreed upon in the facility terms.

The commercial effect is immediate. The seller converts a credit sale into working capital before the due date instead of waiting for collection. On maturity, the financier recovers the full ₹10,00,000 under the agreed structure. Because of this, bill discounting appeals to businesses with healthy receivables but tight cash cycles. The funding comes from the bill itself, and the price paid for that liquidity is the discount amount deducted in advance.

What is Rebate on Bill Discounted

Rebate on discounted bills is an accounting adjustment linked to the timing of income recognition. When a bank or financier discounts a bill, the discount income for the full bill period is received or recognized upfront. At year-end, a portion of that discount may still relate to days that fall after the close of the accounting period. This unearned portion is called a rebate on bills discounted. In simple terms, it is the share of discount income that belongs to the next accounting period over the current one.

This is the clearest answer to what is rebate on bills. It is not a separate charge collected from the borrower, nor is it a second layer of discount over the original transaction. It is a year-end accounting provision designed to prevent income overstatement. Only the discount that has accrued up to the reporting date should remain in current-period income. The balance has to be carried forward because it has not been earned yet.

In banking-style accounting, this adjustment reduces the discount income credited to profit and loss for the year and appears on the liabilities side as unearned income until the next period begins. At the start of the next financial year, the entry is reversed, and the amount is moved back into discount income as time passes and the bill approaches maturity. For this reason, rebates on discounted bills belong to the year-end accounting discipline rather than transaction pricing or receivable funding mechanics.

Eligibility Criteria for Bill Discounting

Genuine Trade Transaction

A bill can be discounted only when it arises from a real sale of goods or services. The receivable must represent an actual commercial transaction as opposed to an accommodation entry or a financing arrangement dressed up as trade. Financiers look for a clean transaction trail because the strength of the underlying sale is the first layer of comfort in any discounting request.

Acceptable Buyer or Drawee Quality

Buyer quality carries major weight in the decision. A strong drawee, anchor, or accepted corporate counterparty improves the bill’s financeability because repayment depends on that payment obligation being honored on the due date. Bank-led vendor finance programs also lean heavily on approved anchors and financially disciplined buyers.

Valid Tenor and Accepted Payment Obligation

The bill must carry an acceptable credit period and a clear payment commitment. Acceptance by the buyer, acknowledgment on the platform, or another recognized payment obligation strengthens the case for funding. Export bill programs also distinguish eligible bills by the nature of the trade paper and the sanctioned facility structure.

Compliance and Onboarding Readiness

KYC completion, onboarding readiness, and alignment with the financier’s policy are part of eligibility, not a back-end formality. On digital receivables platforms, participants enter a paperless ecosystem built around upload, acceptance, discounting, and settlement, which means compliance readiness affects access from the start.

Types of Bill Discounted

Sight Bill Discounting

A sight bill is payable on presentation or immediately on demand, which makes its funding profile different from a bill carrying deferred payment. Discounting a sight bill is based on immediate realization, faster liquidation, and lower tenor exposure, as the payment obligation falls due without a long credit window.

Usance or Time Bill Discounting

A usance bill carries a defined credit period before payment becomes due. The bill remains payable at a future date, which is why the discount charge depends on the tenor still left before maturity. Businesses use this route when a genuine sale has been made on credit, and working capital is needed before collection.

Domestic and Export Bill Discounting

Domestic discounting is linked to receivables arising within the local trade cycle. Export discounting is tied to cross-border trade bills and often moves within export-finance rules, letters of credit, or sanctioned export bill limits. The commercial principle remains the same, though the transaction context, supporting paper, and risk review differ.

With Recourse and Without Recourse Structures

In a with recourse structure, the seller may still be liable in the event the bill is not honored. In a without-recourse structure, the fallback shifts away from the MSME seller under the platform's design. TReDS transactions are expressly described as without recourse to MSME sellers, subject to platform and financier terms.

Process of Discounting a Bill

Invoice or Bill Creation

The process begins when the seller issues an invoice or bill for completed goods or services. The receivable carries a defined value and due date, which provide the financier with a basis for funding review. On digital receivables platforms, the transaction is entered into the system after the seller creates it, and it is acknowledged within the platform flow.

Buyer Acceptance or Confirmation

Early funding depends on a recognized payment obligation from the buyer. In many transactions, this comes through acceptance of the bill, invoice confirmation, or platform-level approval by the buyer. This stage is critical because the financier prices the receivable against a payable obligation rather than against an unconfirmed sales claim.

After acceptance, the receivable is submitted either to a bank, an NBFC, or a receivables-discounting platform. On TReDS, sellers, buyers, and financiers interact within an electronic arrangement built for financing or discounting trade receivables. Outside that route, the seller approaches the lender directly under the facility terms approved for the business.

Assessment and Discounting Decision

The financier then reviews the receivable, buyer strength, tenor, and transaction terms before quoting the discount rate. Once the receivable is approved, the financier deducts the agreed discount charge from the bill amount and sanctions the net funding. This is the commercial decision point in the cycle because it determines pricing and disbursement.

Disbursement and Collection on Maturity

The seller receives the net amount before the due date, which converts the receivable into working capital. On maturity, the financier collects the full bill value under the agreed structure from the party liable to pay. If payment is delayed, additional interest or other contractual consequences can apply, depending on the facility terms.

The standard bill discounting calculation begins with the discount amount. A practical version of the formula is this.

Discount amount = Bill value × Discount rate × Tenor in days ÷ 365

After that, the net proceeds are calculated as follows.

Net amount received = Bill value − Discount amount

This method helps a business estimate the cash it will receive before maturity and the funding costs associated with the receivable.

The bill value refers to the face amount due from the buyer.

The rate refers to the annual discount rate quoted by the financier.

The tenor refers to the number of days left until the due date. Actual pricing can also include processing charges, platform fees, or tax-related additions, depending on the provider and structure.

Documents Required for Bill Discounting

A bill discounting file works best when the lender can read the transaction, the buyer's obligation, the business profile, and the facility paperwork without gaps. The documents below support those four checks.

Core Trade Documents

- Commercial invoice or bill of exchange

- Purchase order, work order, or contract copy where relevant

- Delivery challan, transport document, shipping paper, or goods-receipt proof

- Supporting trade records that establish the receivable as a genuine sale transaction

The first review begins with the trade itself. A lender needs proof that the receivable comes from an actual commercial sale and that the billing value is backed by supply or service evidence.

Buyer Acceptance and Payment-Support Papers

- Accepted bill or formal buyer confirmation

- Undertaking from the buyer where the routed payment is part of the structure

- Comfort support, guarantee backing, or letter-of-credit related paper, where applicable

- Any other document that confirms the buyer’s payment obligation on maturity

Funding strength improves when the buyer’s liability is clearly documented. Acceptance, routed-payment support, or LC-linked backing helps the lender assess repayment certainty with greater confidence.

Business and KYC Records

- PAN and address proof of the business entity

- Certificate of incorporation, constitutional documents, or establishment proof

- GST details and registration records

- Identity and address proof of authorized signatories, promoters, admin users, or other relevant individuals, where required

- Financial statements, tax returns, and bank statements are used for onboarding or credit review

The lender also needs to understand who is borrowing and how the business operates. Entity KYC, statutory registration, and financial records help complete that part of the assessment.

Banking and Facility Documents

- Application form

- Master agreement and facility terms

- Board resolution, authorization letter, or declaration where required

- Bank confirmation letter

- Mandate form for the designated bank account, where applicable

- Any lender-specific sanction paper or operational document linked to the discounting line.

Trade proof and KYC records do not complete the file on their own. The facility can move only after the operational and banking paperwork is in place, as those documents govern disbursements, authorizations, and account management.

TReDS as the Regulated Digital Route

In India, one regulated digital framework for MSME receivables financing is TReDS (Trade Receivables Discounting System), authorised by the Reserve Bank of India.. It is built for financing or discounting MSME trade receivables through a multi-financier electronic framework. This route is designed around accepted receivables, digital submission, and competitive financing, which gives it a distinct place within the wider bill-discounting market.

RXIL

RXIL is one of the active TReDS platforms and operates as a digital exchange for invoice discounting, bill discounting, and factoring. It was set up with institutional backing from SIDBI and NSE, giving it a strong position in the formal receivables finance ecosystem.

M1xchange

M1xchange is another active platform within the TReDS ecosystem. It connects MSMEs, buyers, banks, and NBFCs in a digital environment for invoice discounting. For businesses already operating with participating buyers and financiers, it serves as one of the main electronic routes for receivables funding.

InvoiceMart

InvoiceMart is also part of the current TReDS platform landscape identified by SIDBI. It connects MSME sellers, corporate buyers, and multiple financiers for receivables discounting in a digital marketplace structure.

NSIC Bill Discounting Scheme

The National Small Industries Corporation Bill Discounting Scheme belongs in this discussion as a separate MSME financing route outside the TReDS platform structure. NSIC covers bills arising from genuine trade transactions by MSMEs for supplies made to eligible buyers, including government departments, undertakings, public limited companies, private limited companies, and partnership firms or LLPs. The bills must be accepted by the purchaser, and the discounting is done against a bank guarantee provided by the buyer or the seller in favor of NSIC. The maximum usance period considered for discounting is 180 days.

Bank and NBFC Routes Outside TReDS

Bill discounting is wider than TReDS alone. Banks and NBFCs continue to offer direct bill or invoice discounting under sanctioned facilities, anchor-led arrangements, export bill programs, and bilateral receivables-finance structures. These routes remain relevant where the buyer is outside the TReDS network or where the funding need is structured differently from the platform model.

Benefits of Bill Discounting

Faster Cash Release

Bill discounting converts receivables into usable cash before the due date arrives. That reduces the waiting period between sale and collection and gives businesses quicker access to working capital already locked in the credit cycle. For firms dealing with longer payment terms, this can ease day-to-day liquidity pressure in a very direct way. Industry reports indicate that digital receivables platforms can help shorten collection cycles for many MSME suppliers. Recent market data also shows a 23% reduction in receivable cycles for MSME suppliers using TReDS, underscoring the practical significance of earlier realization.

Better Working-Capital Planning

Earlier access to receivable-backed funds gives finance teams a clearer grip on short-term cash planning. Vendor payments, payroll schedules, purchase timing, and routine operating commitments become easier to manage when inflows do not depend solely on invoice maturity dates. This improves control across the working-capital cycle and gives the business more flexibility during uneven collection periods.

Reduced Pressure on Other Short-Term Funding

Bill discounting can reduce the need to fill every temporary cash gap with unsecured short-term borrowing. Where the business already holds healthy receivables, it offers a funding route linked to actual sales rather than a fresh round of general debt. For MSMEs facing delayed payments, this can provide a more practical, transaction-backed solution to liquidity constraints.

Stronger Receivables Discipline

A discounting structure brings greater order to receivables management because invoice acceptance, due dates, buyer quality, and collection timing come under closer review. Businesses gain a more disciplined view of what is collectible, when it is due, and how payment risk should be managed. Platform-led routes add further structure by creating a clearer acceptance and settlement trail.

Conclusion

Bill discounting helps businesses unlock cash from credit sales before the due date and gives receivables a more active role in working-capital management. The commercial side involves funding, pricing, structure, documents, and platform choice. The accounting side is different because the rebate on bills discounted belongs to year-end income recognition rather than transaction pricing. Businesses that understand both sides can prepare cleaner files, choose better funding routes, and use receivables finance with stronger control over liquidity, reporting, and decision-making.

FAQs

What is bill discounting in simple words?Bill discounting is a way to receive cash against an unpaid trade bill or invoice before the due date. The financier releases the amount early after deducting a discount charge for the credit period.

What is rebate on discounted bills?Rebate on bills discounted is the unearned part of discount income relating to the period after the financial year closes. It is adjusted at year-end to keep income recognition accurate.

What is rebate on bills in banking?In banking, a rebate on bills means the portion of discount on bills discounted that belongs to the next accounting period. It is carried forward because it has not yet accrued as income.

What does a credit bill mean in bill discounting?Credit bill meaning refers to a usance or time bill that carries a credit period before payment becomes due. The amount is paid on a future date rather than immediately on presentation.

What is the difference between a sight bill and a usance bill?A sight bill is payable immediately on presentation, while a usance bill is payable after a specified credit period. This difference affects tenor, pricing, and the structure of the discounting transaction.

Which documents are needed for bill discounting?Bill discounting generally requires the invoice or bill of exchange, buyer acceptance (where applicable), trade support such as purchase orders and delivery proof, KYC records, bank statements, and facility-related documents.

Which are the main bill discounting platforms in India?The main regulated digital route is TReDS. The active platforms commonly identified in this space are RXIL, M1xchange, and InvoiceMart, while banks and NBFCs also offer bill discounting outside TReDS.

Is bill discounting the same as a loan?Bill discounting is different from a general loan because the funding is linked to a specific trade receivable. The amount, tenor, and repayment structure depend on the underlying bill or invoice.

Who can use bill discounting?Businesses with genuine trade receivables, an acceptable buyer, and proper transaction support can use bill discounting. Access also depends on lender policy, buyer quality, and the structure of the receivable.

Why do businesses use bill discounting?Businesses use bill discounting to unlock cash tied up in credit sales before the due date. It helps improve working capital flow and reduces pressure from delayed collections.