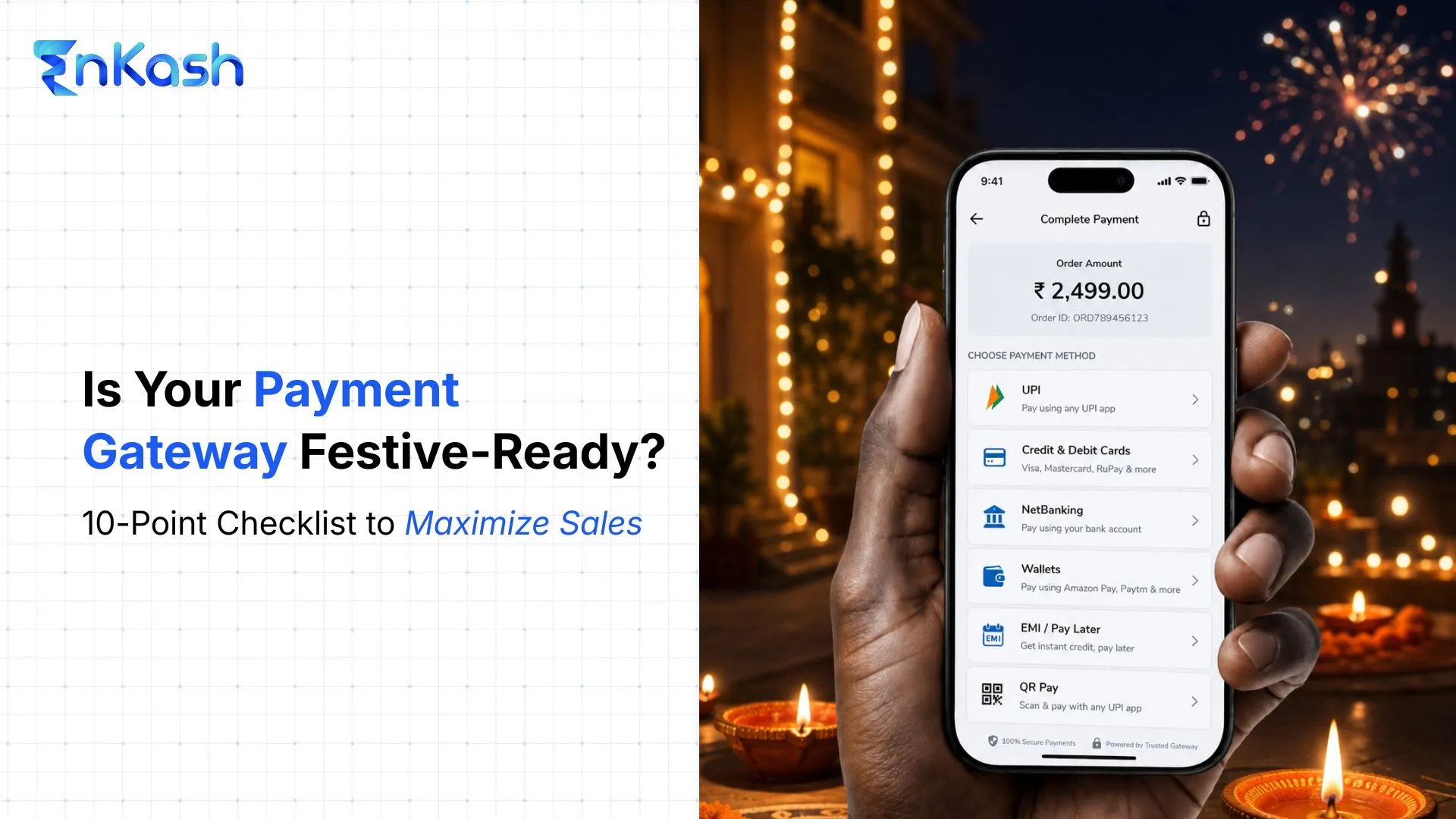

Online payments look simple to customers, but several systems work in the background before a transaction is approved. A payment gateway securely captures payment details, sends them for authorization, and returns the payment status to the business in real time. For any business accepting payments through a website, app, link, or checkout page, the payment gateway directly affects payment success, customer trust, settlement tracking, and revenue collection.

What is a Payment Gateway?

A payment gateway is a secure technology that helps businesses accept online payments through UPI, cards, net banking, wallets, and other digital modes. It encrypts payment details, sends them for authorization, and confirms whether the transaction is successful or failed.

It functions as the front-end of the electronic payment process, transferring customer data to the merchant's acquiring bank to process transactions.

How does an online payment gateway work?

An online payment gateway processes a digital payment by securely transferring transaction details between the customer, merchant, and financial institutions. The process typically follows these steps:

- Customer initiates payment by selecting a payment method such as UPI, credit card, debit card, net banking, or digital wallets.

- Payment details are encrypted and securely sent to the payment gateway.

- The bank or payment network verifies the transaction and checks fund availability.

- The payment is approved or declined based on authentication, bank checks, network response, and available funds.

- The merchant receives the payment status and confirms the order or transaction.

- Funds are settled into the merchant's account according to the settlement schedule.

This secure process helps protect sensitive financial information and ensures smooth online transactions for both customers and merchants.

Read more in detail: Working of Payment Gateways.

Benefits of a Payment Gateway for Businesses

A payment gateway helps businesses accept online payments securely, improve the checkout experience, and manage transactions more efficiently.

- Accepts multiple payment methods: Collect payments through UPI, cards, net banking, and digital wallets.

- Improves checkout conversions: A smooth payment flow reduces drop-offs and failed transactions.

- Strengthens payment security: Encryption and fraud checks help protect customer payment data.

- Simplifies reconciliation: Transaction reports make payment tracking and accounting easier.

- Supports faster business growth: Businesses can collect payments across websites, apps, and other digital channels.

How to Choose a Payment Gateway

Choosing the right payment gateway depends on how your business collects payments, how quickly you need settlements, and how much control your finance team needs over transactions.

- Check supported payment methods: Choose a gateway that supports UPI, credit cards, debit cards, net banking, wallets, and other modes your customers prefer.

- Review payment success rate: A reliable payment gateway should reduce failed payments and improve checkout completion.

- Compare pricing and charges: Check payment gateway fees, setup costs, settlement charges, refund charges, and any hidden platform fees.

- Evaluate security and compliance: Look for PCI DSS compliance, encryption, tokenization, fraud checks, and secure authentication.

- Check integration options: Ensure the gateway supports APIs, SDKs, payment gateway plugins or no-code payment links based on your website or app setup.

- Understand settlement timelines: Review how quickly funds are transferred to your merchant account and whether instant settlement is available.

- Assess dashboard and reconciliation tools: A good gateway should provide transaction reports, refund tracking, settlement details, and failure reasons.

- Review customer support: Choose a provider with reliable support for failed payments, refunds, disputes, and integration issues.

Payment Gateway vs. Payment Terminal

Many people confuse a payment gateway with a payment terminal, but they serve different purposes in the digital payments environment.

| Feature | Payment Gateway | Payment Terminal (POS Machine) |

|---|

| Definition | A secure online platform that processes digital transactions between a buyer and seller. | A physical device used to accept card payments in offline stores. |

| Usage | E-commerce websites, mobile apps, SaaS platforms, and subscription businesses. | Retail shops, restaurants, hotels, and offline businesses. |

| Transaction type | Card-not-present (CNP) transactions, including online cards, UPI, net banking, and wallets. | Card-present (CP) transactions, including swiped, inserted, or tapped card payments. |

| Integration | Integrated through APIs, SDKs, plugins, or payment links on a website or app. | Integrated through POS Machines connected to a merchant or bank account. |

| Settlement process | Payment gateway to the acquiring bank, issuing bank, and merchant settlement. | POS terminal to acquiring bank, card network, issuing bank, and merchant settlement. |

| Security features | SSL encryption, tokenization, PCI DSS compliance, and fraud checks. | EMV chip technology, PIN authentication, and card-present transaction security. |

| Examples | EnKash, Razorpay, PayU, Paytm, CCAvenue, and Stripe. | Pine Labs POS, HDFC POS Terminal, and ICICI Merchant Terminal. |

Payment Gateway vs. Payment Processor

A payment gateway and a payment processor work together, but they perform different roles in online payment processing.

| Feature | Payment Gateway | Payment Processor |

|---|

| Meaning | Securely captures, encrypts, and sends payment details for authorization. | Transfers transaction data between banks, card networks, and financial institutions. |

| Main Role | Front-end payment technology that enables online payment acceptance. | Back-end transaction processing system that facilitates payment execution. |

| Used For | Checkout processing, encryption, payment authorization, and transaction status updates. | Fund routing, transaction clearing, settlement, and bank communication. |

| Works With | Websites, mobile apps, payment links, checkout pages, and online businesses. | Acquiring banks, issuing banks, payment processors, and card networks. |

| Primary Focus | Secure customer checkout experience, fraud prevention, and payment authorization. | Transaction processing, payment approval, fund movement, and settlement. |

Read More: Payment Gateway vs Payment Processor

The Parties in the Payment Gateway Ecosystem

A payment gateway ecosystem involves multiple parties working together to complete a secure online transaction. Each participant plays an important role in the payment flow:

1. Customer (Payer): The customer is the one who initiates the payment—whether by card, UPI, wallet, or net banking. This is the person-to-merchant transaction, where money flows from the buyer to the seller.

2. Merchant (Payee): The merchant is the business or seller receiving the payment. For e-commerce or SaaS businesses, the merchant payment gateway ensures they can accept and manage online transactions seamlessly.

3. Payment Gateway: The gateway online system captures the customer’s payment details, encrypts them, and routes them securely to the banks for authorization.

4. Acquiring Bank (Merchant’s Bank): This is the bank that holds the merchant account. It receives the transaction request from the payment gateway and forwards it to the payment processor.

5. Issuing Bank (Customer’s Bank): The issuing bank provides the card or account used for payment. It verifies the details, checks the balance, and approves or declines the transaction.

6. Payment Processor / Card Network: Payment processors and card networks help route transaction information between the acquiring bank and issuing bank. Card networks such as Visa, Mastercard, RuPay, and American Express support card-based transactions.

Popular Payment Gateway Companies in India

India has witnessed rapid growth in digital payments, and several payment gateway companies now power secure online transactions for businesses of all sizes. Choosing the right payment gateway provider is essential to ensure smooth checkouts, faster settlements, and a reliable customer experience.

Top Payment Gateway Companies in India

EnKash Payment Gateway: It is a fast-growing online payment gateway designed for businesses of all sizes. EnKash offers secure APIs, multiple payment methods (cards, UPI, net banking, wallets), and competitive pricing.

Razorpay: One of the most popular payment gateway providers, Razorpay offers easy integration for startups, e-commerce stores, and SaaS platforms. It supports cards, UPI, EMI, and international payments.

Paytm Payment Gateway: Backed by India’s leading fintech brand, Paytm offers a robust merchant payment gateway with wallet, UPI, cards, and net banking options, ideal for high-volume businesses.

PayU: A trusted payment gateway company, PayU, caters to SMEs and large enterprises with features like recurring billing, fraud detection, and multi-currency support.

CCAvenue: One of the oldest third-party payment gateways in India, CCAvenue supports 200+ payment options, including cards, wallets, and net banking. It is widely used by e-commerce merchants.

Read more: Top 10 payment gateways in India

Conclusion

A payment gateway is an important part of online payment acceptance for digital businesses. From enabling smooth e-commerce transactions to ensuring secure online trading, payment gateways make it possible for businesses and customers to exchange money safely and instantly.

Whether you are a startup, SME, or enterprise, choosing the right payment gateway provider in India—such as EnKash, Razorpay, PayU, Paytm, or CCAvenue—can help you deliver a frictionless payment experience, gain customer trust, and grow your business.

FAQs

1. What is meant by a payment gateway?

A payment gateway is a secure technology that connects a merchant’s website/app with the bank, allowing customers to make online payments via cards, UPI, net banking, or wallets.

2. What is the difference between a payment gateway and a payment terminal?

A payment gateway is used for online payments (e-commerce, apps), whereas a payment terminal (POS machine) is a physical device for offline, in-store card payments.

3. How secure are payment gateways?

Modern payment gateways are highly secure with SSL encryption, PCI DSS compliance, tokenization, OTP verification, and fraud detection systems to protect customer data.

4. How to add a payment gateway to a website?

To add a payment gateway to a website:

- Choose a payment gateway provider (e.g., EnKash, Razorpay).

- Complete KYC and account setup.

- Integrate APIs or plugins.

- Test in sandbox mode before going live.

5. What are the top payment gateway companies in India?

Popular payment gateway providers in India include EnKash, Razorpay, PayU, Paytm, and CCAvenue.

6. How much does a payment gateway cost?

The payment gateway cost depends on the provider and transaction type. In India, payment gateway charges vary by provider, payment mode, transaction volume, settlement type, and business category. UPI is often priced differently from cards, wallets, and net banking.