Over the last few months, we have seen a growing number of cases where a payment appeared to be completed, but the money never reflected in the merchant’s account. In most situations, the transaction moved forward because the screenshot looked familiar and matched what people expected to see after a successful payment. UPI payments have become routine across counters, deliveries, and one-to-one sales. When you see the same confirmation screens multiple times a day, it becomes easy to rely on familiarity instead of verification. A screen that looks right often feels sufficient, especially when the transaction flow matches what you have seen many times before. Most of these cases surface during routine business moments such as peak hours, end-of-day closures, or quick handovers. A confirmation screen is shown with a visible reference number, and the transaction looks identical to many others that have gone through without issues. When everything appears familiar, checking your own account often slips down the priority list. This pattern is no longer limited to small retail counters. If you are a freelancer, a service provider, part of a delivery team, or an individual seller, the same risk applies. While the setting may change, the breakdown usually happens at the same point. The decision to move forward is based on what appears on the payer’s phone rather than what reflects in your own bank or UPI app.

What is a Fake Payment Screenshot Scam

A fake payment screenshot scam happens when someone shows a payment confirmation screen, but no money has reached your account. The transaction moves forward because the screenshot looks like a normal UPI success screen, even though the payment was never completed. The screen usually shows all the expected details, including the amount, time, and a reference number. Since it looks similar to genuine payment confirmations, it is easy to assume the payment is done without checking your own app. Collect UPI Payments Safely

Who Gets Targeted Most

Fake payment screenshot scams affect anyone who accepts UPI payments as part of daily transactions. The risk is higher in situations where payments are completed quickly and verification is treated as routine rather than deliberate. Merchants at physical counters are often exposed because transactions happen continuously and attention is divided between customers, stock, and billing. In these moments, a familiar-looking confirmation screen is often accepted without further checks. Freelancers and service providers face similar risks, especially when payments are settled at the end of a task or service. The focus is usually on closing the job, which makes it easier to rely on what is shown on the payer’s phone. Delivery staff and individual sellers are also affected because payments are completed on the move or in informal settings. Across all cases, the common factor is reliance on visual confirmation instead of checking whether the payment has reflected in the recipient’s account.

How Scammers Create Fake Payment Screenshots

Scammers use different tricks to create the illusion of a successful transfer. Most of these methods are designed to look convincing at first glance, which is why many people fall into the trap. Knowing the common approaches helps you stay alert.

Edited or Manipulated Screenshots

In some cases, a real payment receipt is edited to change details like the amount, date, or reference number. If you are busy, these changes are easy to miss at a glance.

Prank and Spoof Apps

Certain apps copy the look of real UPI platforms and generate fake success screens. These screens often resemble confirmations from popular apps like GPay, which makes them appear believable at first glance. No transfer takes place, even though the screen shows a completed payment.

Fake UPI IDs and Transfer Requests

Fraudsters also mislead by sharing fake UPI IDs. A victim sends money believing the ID belongs to the seller, but the transfer goes to someone else entirely. In some cases, fraudsters generate fake UPI transfers and show a “pending” or “processing” message, pretending that funds are on their way.

Fabricated Payment Histories

Cloned or tampered apps sometimes display a full fake Paytm history or fake online payment records. These screens are used to convince merchants that the user has paid on multiple occasions. In reality, the entries do not exist in the banking system.

Social Engineering with Screenshots

The fraud is not always about technology. Many scammers apply social pressure. They flash a payment screenshot, act hurried, and insist that the money has gone through. In crowded places or during busy hours, merchants may feel pressured to complete the deal without checking their own app.

Step-by-Step: How to Detect a Fake UPI Payment in Seconds

The best defense against fraud is learning how to detect a fake UPI payment before handing over your product or service. Scammers rely on speed and distraction, but a few careful checks can expose a fake payment instantly. Step 1: Check your own UPI app or bank account first A real payment shows up in your transaction history. If the credit is not visible on your side, the payment has not been received. Step 2: Match the amount and time on your record If the payer shows a success screen, compare the amount and timestamp with what appears in your app. If there is no matching entry, the screenshot does not help. Step 3: Verify the reference number in your transaction history A genuine payment has a reference number that appears with the transaction in your app or bank statement. If you cannot find it, the payment is not confirmed. Step 4: Confirm the payee name shown for the transfer UPI usually displays the recipient name during the payment flow. If the name shown does not match your business or your account, treat the transfer as incorrect. Step 5: Do not rely on screenshots, SMS, or sound alerts Screenshots can be edited and messages can be delayed. Sound alerts can also be misleading. Your own app is the final confirmation. Step 6: Slow down if the payer creates urgency Pressure to hand over the product quickly often shows up in fake payment cases. If the payment has not reflected, it is safer to pause the transaction. A typical interaction often looks like this: Customer: Payment done. Here’s the screenshot. Merchant: Okay, let me just check my app once. Customer: It’s successful. See the reference number. Merchant: I don’t see the credit on my side yet. Customer: It will reflect in some time. Network issue. Merchant: I need to confirm.

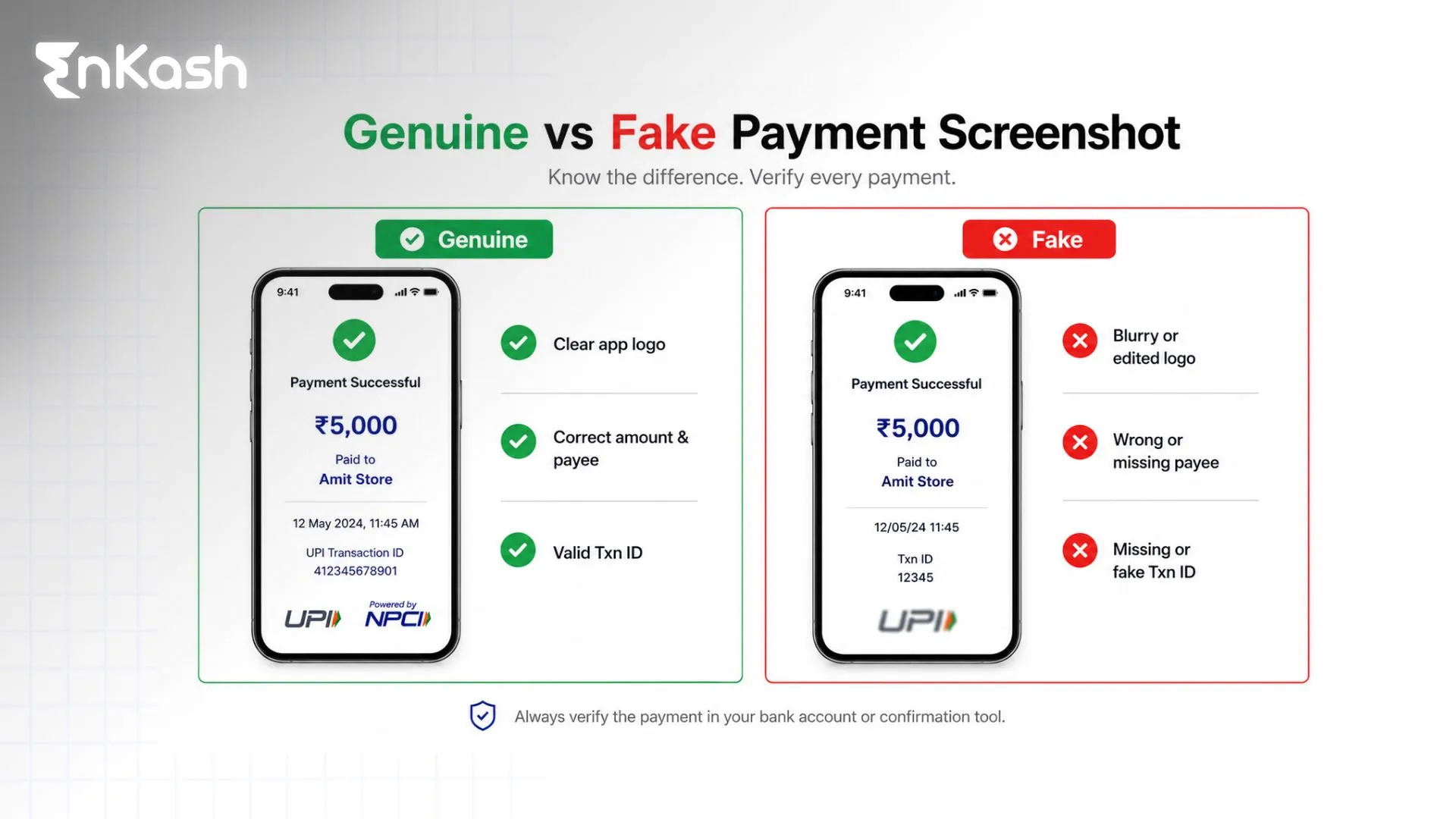

Difference between Real and Fake Payment Screenshot

Risks of Fake Payment Scams

Fake payment tricks may look harmless on the surface, but the damage runs deeper than a single lost sale. They put individuals, businesses, and even the larger digital payment systems at risk.

Direct Financial Losses

The most obvious impact is losing money or goods without receiving actual payment. For small merchants, even a single fake UPI payment can cut into daily earnings. In peer-to-peer sales, like second-hand items or services, the loss hits individuals directly.

Reputational Harm

When fraud happens repeatedly, customers lose confidence. A shop or service provider known for being tricked by fake payment claims may face trust issues. People might assume the business is careless with digital transactions, which hurts long-term credibility.

Legal Complications

Handing over products or services based on a fake screenshot can lead to disputes. If a merchant tries to recover the loss later, it may involve police reports, legal processes, or long banking complaints. All of this consumes time and resources.

Operational Disruption

Fraud is not just about money - it disrupts operations too. It slows down business operations. Staff have to manage disputes, explain situations to genuine customers, and record complaints. This wasted time could otherwise be used to serve paying clients.

System-Wide Risks

On a larger scale, repeated incidents of fake online payment scams erode trust in digital platforms. If users start doubting apps like UPI, PhonePe, or Paytm due to prank payment apps or Paytm spoofing cases, it weakens confidence in the entire ecosystem.

How Merchants Can Protect Themselves from Fake Payment

Merchants are the most common targets for fake payment scams. The good news is that a few simple practices can make it extremely hard for fraudsters to succeed. Prevention depends on discipline, staff training, and clear rules at the point of sale.

Adopt a “No Screenshot” Policy

Set a clear rule: goods or services will only be handed over once the payment reflects in your own app or bank account. A fake payment screenshot may look convincing, but your app’s transaction history is the only real proof. Displaying this policy on a signboard helps customers understand it’s non-negotiable.

Verify Every Transaction Yourself

Always check your own merchant app or bank statement before completing an order. Do not rely on the customer’s device. This single step blocks most fake UPI transfers.

Train Your Staff Regularly

If employees handle payments, train them to stay calm under pressure. Scammers often act rushed, insisting that the money is “already sent.” Role-play these scenarios during staff briefings so your team is prepared.

Use Payment Soundboxes Wisely

Soundboxes are useful, but they are not foolproof. There have been cases where merchants trusted the Chime without checking their app and lost money to fake online payment attempts. Use sound notifications as an alert, not as final proof.

Communicate Clearly with Customers

Polite but firm communication reduces conflict. A short line, such as “We release the product only after the payment shows in our account,” makes your process transparent. Most genuine customers respect this rule.

Keep Records of Transactions

Maintain receipts, digital confirmations, and notes of disputed cases. If you ever face a Paytm spoof or a fake Paytm history scam, detailed records will help when filing a complaint with your bank or the cybercrime portal.

Some financial institutions and payment service providers offer protection plans for merchants. These can provide coverage against digital fraud, including prank payment apps that generate false confirmations.

Legal and Regulatory Aspects in India

Digital payment frauds have grown rapidly, and regulators have stepped in with rules to protect both merchants and users. A fake payment may look like a small trick, but under the law, it is treated as a serious offence.

Laws That Apply to Fake Payment Scams

Cheating someone with a fake payment screenshot falls under sections of the Indian Penal Code dealing with fraud and deception. The Information Technology Act also applies, as it covers electronic records and online transactions. Depending on the case, charges may include forgery, impersonation, and financial fraud.

The Cybercrime Helpline and Reporting Portal

Victims can immediately call the national cybercrime helpline number 1930 or submit a complaint through the official cybercrime reporting portal. Quick reporting improves the chances of tracking a fake UPI payment and freezing suspicious accounts before the scammer withdraws funds.

Guidelines from RBI and NPCI

The Reserve Bank and NPCI have issued multiple guidelines to make UPI safer. Rules include mandatory two-factor authentication, device binding, and limits on risky flows. These steps reduce misuse, but the biggest safeguard is still user awareness. No rule can protect a merchant who releases goods only on the basis of a fake Paytm screenshot.

Recent Updates in the Payment Ecosystem

New policies require the payee’s name to be shown before a transfer is made. This helps prevent fraud using fake UPI IDs or misdirected payments. Collect request features, which were once misused, are being phased out to further tighten the system. These updates aim to close gaps that fraudsters once used.

How to Report and Handle a Fake Payment Incident

Even with precautions, there may be times when a scammer slips through. In such cases, acting quickly makes all the difference. The faster you report a fake payment, the better your chances of recovering funds or preventing further misuse.

If you realize you have handed over goods or services after a fake payment screenshot, call the national cybercrime helpline 1930 right away. The system is designed to alert banks and freeze suspicious accounts before the scammer withdraws the money.

File a Complaint on the Cybercrime Portal

Visit the official cybercrime reporting portal and register your case. Provide complete details, including the payer’s fake VPA, the amount claimed, and any screenshots or chat logs. This creates an official record that investigators and banks can act upon.

Inform your bank or UPI app support team as soon as possible. Share the transaction reference you were shown and explain that it was fraudulent. Even if funds cannot be traced, reporting helps flag accounts that use prank payment apps.

Preserve Evidence Carefully

Do not delete messages, screenshots, or CCTV footage. Save the payment screenshot shown by the fraudster, note down the phone number, and record the time and place of the incident. Detailed evidence strengthens your complaint and helps investigators track repeat offenders.

Escalate Through the Dispute Process

Most UPI apps and banks have a dispute redressal system. Raise a ticket and follow up regularly. Escalation through NPCI channels is possible if the issue remains unresolved.

Common Myths Around Fake Payments

Many people lose money because they believe in common assumptions about digital transfers. These myths make scammers’ jobs easier. Clearing them up is key to staying safe. “If the customer’s phone shows success, the money is in my account.” This is false. A fake payment screenshot or even a real success screen on the payer’s phone does not prove anything. The only proof is the credit appearing in your own app or bank account. “SMS alerts are enough to trust.” Messages can be delayed, duplicated, or even spoofed. Fraudsters have used fake notifications to convince shopkeepers of a fake UPI payment. Always confirm through your official app. “Soundbox chimes mean the money is settled.” Soundboxes are helpful but not final proof. There have been cases where merchants trusted the chime and later found no credit. Never release goods without checking your own record of the transaction.

Conclusion

UPI payments have made transactions quicker, but they have also made it easier to rely on what looks right instead of what is actually confirmed. A payment screen can appear genuine even when the money has not reached your account. Most issues arise during routine moments when verification feels unnecessary. If you accept digital payments regularly, your own bank or UPI app is the only place that confirms whether a payment is complete. Screenshots, alerts, and messages may appear reassuring, but they do not confirm that a payment has been received. The only confirmation comes from your own bank or UPI app. When you make this check part of how you accept payments, disputes become less frequent and losses are easier to avoid.

FAQs

1. What is a fake payment app? A fake payment app is an application that looks like a real UPI app but does not move any money. It generates fake success screens, receipts, or payment histories to make a transaction appear complete even though no payment has been made. 2. How do scammers use fake Paytm or PhonePe apps? Scammers use cloned or spoofed apps that copy the design of popular UPI platforms. During a transaction, they enter payment details and show a fake success screen. Since no real transfer takes place, the payment never reaches the recipient’s account. 3. How can you identify a fake UPI transfer? A fake UPI transfer does not appear in your own bank or UPI transaction history. Screenshots, green ticks, or reference numbers shown by the payer do not confirm payment unless the credit reflects in your account. 4. Is using fake payment screenshots illegal in India? Yes. Using fake payment screenshots to obtain goods or services can be treated as cheating and misuse of electronic records under Indian law, depending on the facts of the case. 5. How can merchants protect themselves from fake payment fraud? Merchants reduce risk by relying on their own bank or UPI app to confirm payment before completing a transaction. Following the same verification process for every customer also helps avoid pressure-based mistakes. 6. What should you do if you receive a fake payment receipt? You should check your own account before releasing the product or service. If the payment does not reflect, the transaction should not proceed. If goods have already been handed over, the incident should be reported immediately. 7. Are prank payment apps safe to use? No. Prank payment apps are often misused for fraud and may carry legal and privacy risks. Using or relying on them can lead to financial loss and legal trouble. 8. What evidence should you collect if scammed by a fake payment? You should keep the screenshot shown to you, note the payer’s phone number and UPI ID, save any messages, and retain records from your own app showing that no payment was received. 9. Can banks recover money lost to fake UPI payments? Recovery depends on how quickly the fraud is reported and whether the funds can be traced. Early reporting improves the chances of action, but recovery is not guaranteed. 10. How do fake online payments affect trust in digital transactions? Repeated fraud cases make people hesitant to rely on UPI payments. This affects both merchants and customers by slowing down transactions and reducing confidence in digital payment systems.