Cheques may appear less common in a UPI-led payment environment, yet they remain a recognised banking instrument for authorising account-based payments in India. A cheque is a written payment instrument drawn on a specified banker and payable on demand. In everyday banking terms, it is an instruction from an account holder directing the bank to pay a specified amount to a named payee. RBI data indicates that several million cheques are processed through the CTS clearing system daily across India, highlighting that the instrument remains active within the formal banking infrastructure.

Cheques are still issued for structured payments such as rent, school fees, vendor invoices, and transactions where written authorisation supports documentation and reconciliation. Banks process cheques through established legal and clearing systems, which helps ensure consistent handling when a cheque is presented for deposit.

In this blog, you will get a clear cheque definition, a quick breakdown of a cheque leaf, and a practical method to write a cheque correctly for Indian payments. It also covers how banks read key fields during processing, which errors commonly trigger returns, and a short checklist to reduce avoidable issues for both payer and payee.

What is a Cheque

A cheque is a written payment instruction. It tells a bank to pay money from the account holder’s account to a named person or business. In India, legal definition of a cheque is provided under Section 6 of the Negotiable Instruments Act, 1881, while cheque processing and clearing are governed through RBI-regulated banking and CTS frameworks.

In day-to-day banking, a cheque follows a simple flow. The account holder issues the cheque. The payee deposits it into a bank account. The banking system verifies key details and clears the cheque before crediting the money. This is why banks treat a cheque as a formal payment instruction, not a casual note.

A bank cheque is used when the payer wants a clear record of the payment instruction. It is common for rent, school fees, vendor invoices, and payments, where documentation helps with tracking and reconciliation.

The cheque definition also becomes easier when you separate it from similar documents:

- A cheque is not cash.

- A cheque is not a receipt.

- A cheque is not a guaranteed payment if funds are not available.

A correctly issued cheque provides a structured way to pay through the banking system, with clear accountability for both the payer and the payee.

Features of a Cheque

A cheque is treated as a formal payment instruction linked to a bank account. It creates a clear record of who authorised the payment and who is entitled to receive it. Banks process it through defined checks before releasing funds.

Payable on Demand Within Banking Process

A cheque is payable on demand, meaning it is payable when presented through banking channels. Handing over the paper does not complete payment. Deposit and clearing come first, then credit is given if the checks pass.

Clear Accountability for Payer and Payee

A cheque supports accountability in a payment chain. The drawer authorises payment, the payee presents it, and the bank validates key requirements. This structure supports documentation, internal controls, and dispute review.

Controls that Reduce Misuse Risk

Practical controls, such as crossing and payee restrictions, reduce misuse and push collection through an account route. These controls support safer use, with documentation and traceability expected for formal payments.

Cheque Meaning in Banking is Standardised

Banks treat cheques using a standardised legal and clearing framework. This keeps processing consistent across common use cases and reduces uncertainty during deposit and collection.

Cheque Issue Meaning in Operational Terms

Issuing a cheque means handing a completed instrument to the payee as an instruction for payment. After the issue, sufficient funds and clean execution become critical, since avoidable errors can lead to a return.

Cheque Leaf as the Physical Instrument

A cheque leaf is the single page taken from a cheque book. Banks treat each leaf as a unique instrument because it carries identifiers linked to the account and the issuing bank. The printed layout also helps clearing systems read and process the cheque consistently.

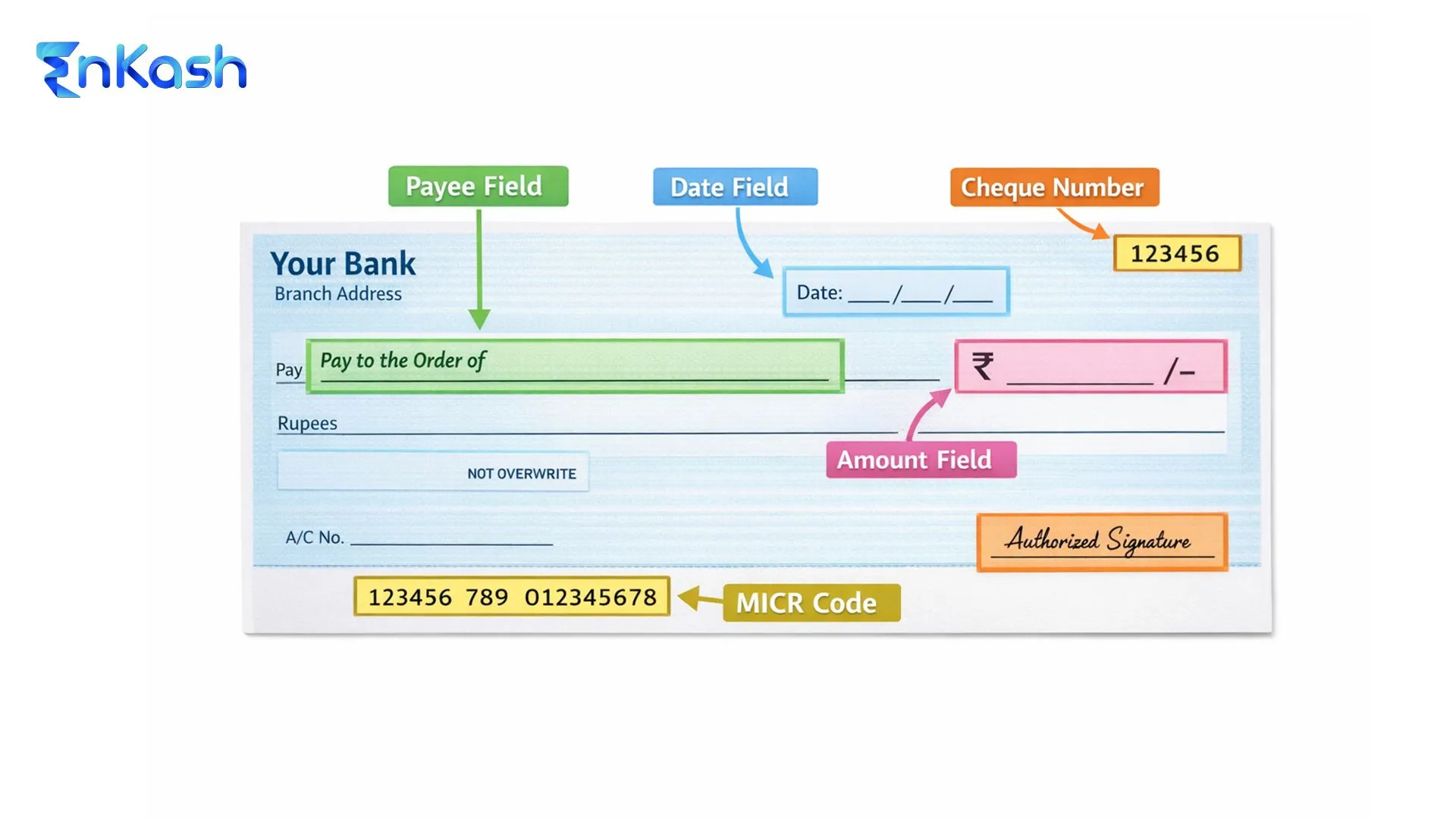

Parts of the Cheque

Bank and Branch Identifiers Printed on the Cheque

A cheque carries the bank name and branch details printed on the leaf. Many cheques also include codes used for routing in clearing. These identifiers help the collecting bank and the clearing system recognise the drawee bank and direct the cheque for processing.

Payee and Date Fields Used for Payment Instruction

The payee line records the name of the person or business receiving the payment. The date field indicates when the instrument is intended to be payable. Both entries support validation and help avoid disputes during deposit and processing.

Cheques include two separate amount entries: the numeric amount and the written amount. Banks compare these entries during handling. Clean writing and consistent amounts reduce the risk of return due to mismatch or unclear entries.

Signature Area Used for Authorisation

The signature is the drawer’s approval for the bank to honour the payment instruction. Banks compare the cheque signature with the signature on record for the account. A clear, consistent signature reduces avoidable rejection.

Cheque Number and Serial Identification

A cheque number is printed on the cheque leaf as a serial identifier. It helps track the instrument for recordkeeping, stop payment requests, and reconciliation. It also helps distinguish each cheque issued from a cheque book.

What is a Cheque Number and How to Find It

Serial Reference Used for Identification

A cheque number is a unique serial reference printed on each cheque. Banks and account holders use it to identify an exact instrument during tracking and reconciliation.

Location on the Cheque Leaf

You can find the number on the cheque leaf in the printed series area. Many cheque formats also display it within the printed code line used in clearing. Always record the printed number from the instrument for accuracy.

Common Banking Uses for Recordkeeping

The number helps during stop payment requests and internal payment logs. It also helps confirm which instrument was issued for a vendor invoice. Finance teams use it to match bank entries with accounting records.

Clear Separation From Other Identifiers

This reference is different from the account number and routing identifiers. Treat it as an identifier for a specific cheque instrument, not as confirmation of successful payment.

Types of Cheques Used in India

Bearer Cheque and Order Cheque

A bearer cheque allows payment to the person presenting the instrument, subject to the bank's rules and verification checks. An order cheque is payable only to the person named on the cheque, creating a clearer payee linkage.. For routine payments where the payer wants stronger control over who collects the funds, an order cheque is usually the cleaner choice.

Open Cheque and Crossed or Account Payee Cheque

An open cheque is issued without a crossing, which means collection restrictions are lighter and the risk is higher if the cheque is misplaced. A crossed cheque imposes a restriction requiring collection through a bank account rather than over-the-counter payment. An account payee marking tightens the restriction by indicating that the credit should go to the named payee’s account. These formats suit rent, invoice, and institutional payments, where traceability supports reconciliation.

Self Cheque

A self cheque is written in the account holder’s own name, generally for cash withdrawal at a branch when allowed by the bank. The bank verifies the signature and account status before releasing cash. This type fits personal cash requirements handled through a branch channel.

Post-dated Cheque and Ante-dated Cheque

A post-dated cheque carries a future date and is used when payments need to be scheduled in advance, such as rent commitments or vendor contracts. An ante-dated cheque carries a date earlier than the day it is written and issued. In both cases, the date written on the cheque indicates when it is intended to be presented, and banks assess it during processing based on that date.

Stale Cheque

A stale cheque is a cheque presented beyond its permitted validity period and may be returned as out of date. This is not a separate "format" chosen for use. It is a status that arises when timing and presentation do not align with validity rules.

Cancelled Cheque

A cancelled cheque is a cheque leaf marked “cancelled” with two parallel lines. It is used for account verification in processes like KYC, mandate registration, or bank detail confirmation. It is not used to make a payment because cancellation removes the payment intent.

Blank Cheque

A blank cheque is signed but not fully filled out. It carries a higher risk of misuse if it is lost, copied, or handled by multiple parties. Many organisations avoid accepting blank signed cheques because they weaken control and create avoidable disputes.

Banker’s Cheque, Pay Order, and Demand Draft

These instruments are issued by a bank, rather than by an individual account holder, after funds are collected or blocked as per the bank's process. They are used for formal transactions such as fees, tenders, or large-value payments where the payee prefers a bank-issued instrument. Bank issuance reduces execution risks associated with handwriting or signature mismatches.

Indian law recognises cheques in electronic form and the electronic image of a truncated cheque used in clearing. Many banks also issue payable-at-par cheque formats intended for wider acceptability across locations. These categories reflect how cheque usage has adapted to modern clearing and standardisation requirements.

Traveller’s Cheque

Traveller’s cheques were historically used for controlled encashment during travel. Their use has almost disappeared in India after the rise of cards and digital payments.

Validity of a Cheque in India

Validity Period Counted From the Instrument Date

In India, validity is counted from the date written on the cheque. RBI circular DPSS.CO.CHD.No.1832/04.07.05/2011-12 reduced the validity period of cheques, demand drafts, and pay orders from six months to three months from the instrument date.. After this period ends, banks generally treat the instrument as out-of-date during processing.

Stale Cheque Outcome During Deposit

A stale cheque is not a separate format chosen by the payer. It is a status that arises when the cheque is presented after the permitted validity window. In such cases, the collecting bank can return the instrument unpaid, and the payer usually needs to issue a fresh cheque with a current date.

Post-dated Cheque Handling Within Validity Rules

A post-dated cheque is dated in the future. Banks are expected to process it only when it is presented on or after that date, subject to standard checks and funds availability. Validity is assessed from the date on the instrument, not from the handover date.

Ante-dated Cheque Handling Within Validity Rules

An ante-dated cheque carries a past date. Banks assess validity using the instrument date at the time of deposit. If the cheque is already beyond its validity window when presented, a return is likely.

Practical Controls for a Bank Cheque

For a bank cheque used in structured payments, issue the cheque close to the expected deposit date. Confirm the date entry is correct before handing it over. Replace any cheque that has crossed the validity window instead of requesting informal corrections.

How to Write a Cheque for Payment

Prepare Before Filling the Cheque

Use a fresh and clean leaf from the cheque book. Write with a single dark ink pen and keep the handwriting clear. Avoid overwriting and avoid leaving blank gaps that can be misused.

Write the date in the usual Indian format used on bank instruments. Ensure the date is legible and complete. A missing digit or unclear date can trigger a return during processing.

Write the Payee Name Without Shortcuts

Write the payee name exactly as it should appear for deposit. For a company, use the full registered name as it appears on invoices or official documents. Avoid initials and avoid extra blank space after the name.

Write the amount in numbers inside the figures box. Use commas where needed and keep the digits aligned inside the box. If paise is included, write it clearly in the figure entry.

Fill the Amount in Words With Controlled Spacing

Write the amount in words on the line provided. Add "only" at the end after the amount to reduce misuse risk. Strike through unused space on the line with a single clean line to prevent additions later.

Apply Crossing and Payee Restriction When Needed

Cross the cheque when the payment should be collected through an account channel. Add an account payee marking when the payment should be credited to the named payee’s account. This control is preferred for invoice payments and third-party payments.

Sign in the Bank-recorded Style

Sign in the signature area using the same signature style recorded with the bank. Avoid variations in signature strokes. A mismatch can lead to a return even when all other fields are correct.

Record the Key Details After the Issue

Record the date, payee name, amount, and cheque number for tracking. This helps if the payee reports a delay, if a stop payment request is needed, or if reconciliation is required later.

Key Points to Remember While Writing a Cheque

- Use the same signature style recorded with the bank for every payment.

- Avoid overwriting, scratching, or using correction fluid on any field.

- Keep the payee name complete and clearly readable for deposit.

- Ensure the amount in words and the amount in figures match fully.

- Strike out unused space on the amount-in-words line to block additions.

- Do not sign and hand over a blank or partially filled instrument.

- Record the date, payee, amount, and cheque number for tracking.

- Cross the cheque for third-party payments routed through an account.

Advantages of a Cheque

Documented Payment Instruction for Records

A cheque creates a written payment instruction that supports documentation. This helps when payment trails are needed for audits, internal approvals, or dispute checks.

Clear Payee Naming for Controlled Payouts

The payer writes the payee's name on the instrument, reducing ambiguity at the point of deposit. This supports invoice-linked payments, fee payments, and vendor settlements where naming accuracy is important.

Suitable for Approval-led Business Workflows

A bank cheque aligns with finance processes that require visible authorisation. Teams can log the payee, amount, and issue details before deposit, improving reconciliation and query handling.

Useful When Digital Initiation is Not Available

Cheques allow issuance without immediate digital initiation, while still enabling collection through banking channels later.

Disadvantages of a Cheque

Slower Completion Compared to Instant Rails

A cheque requires deposit and clearing before credit is confirmed. This adds time compared to instant account-to-account transfers, which can affect the timing of urgent payments.

Higher Return Risk Due to Execution Errors

Minor errors can lead to a return, even when funds are available. Common triggers include unclear writing, mismatched amount entries, signature mismatch, and incorrect payee naming. A return can delay settlement and create follow-up work for both parties.

Misuse Risk if Handling Controls are Weak

A lost instrument, a signed blank instrument, or a cheque issued with wide encashment flexibility increases the risk of misuse. Risk also rises when cheques pass through multiple hands before deposit.

Process and Tracking Effort for Businesses

A bank cheque adds operational work for logging issue details, tracking deposit status, and matching clearing outcomes with invoices. Teams may also need to stop payment controls if a payment route changes.

Conclusion

A cheque is a structured banking payment instrument governed by legal and clearing frameworks in India. When written correctly, it provides traceability, documentation, and accountability between payer and payee.. Once you understand cheque meaning in banking, you view a cheque as a formal payment authorisation that moves through verification, clearing, and documented outcomes, not as a casual handover. That distinction protects both parties. It reduces dispute risk, improves reconciliation, and keeps payment records clean when transactions need written authorisation.

Execution quality decides the result. Use clear writing, complete entries, and consistent signatures. Apply crossing and account payee restrictions when the payment must be collected through an account route. Record the cheque number and issue details the moment the instrument is handed over, since tracking begins at issue, not after deposit. When you know the cheque information printed on the leaf and respect the validity rules, cheque payments become disciplined, bank-readable, and far less likely to face return or delay.

FAQs

What should I do if I lose a cheque before handing it to the payee?Request a stop payment from your bank immediately using the cheque number and date range. Record the request reference for follow-up. If misuse risk seems likely, file a complaint as your bank advises. Issue a fresh cheque only after confirming the stop instruction is active.

How can I confirm if a deposited cheque was credited or returned?Check the account statement and transaction narration after the deposit date. Banks typically post either a credit entry or a return entry with a reason code. For business use, match the deposit slip reference with the statement line. Keep screenshots or PDFs for audit and closure.

What does a cheque return memo mean, and why is it important?A cheque return memo is the bank’s written reason for non-payment. It helps identify the exact failure point, such as signature mismatch, date issue, or funds shortfall. Keep the memo with your records. It supports reissue decisions, dispute resolution, and documentation for compliance reviews.

How should I write the payee name for a company or institution?Use the exact registered name used on invoices, fee notices, or official letters. Avoid initials, short forms, and informal names. If the institution provides a prescribed payee format, copy it exactly. Clear payee naming reduces deposit rejection risk and speeds reconciliation for the receiving finance team.

What should I do if the amount in words and figures does not match?Cancel the cheque and issue a fresh cheque with clean entries. Do not overwrite or use correction fluid, because a mismatch raises return risk and dispute risk. Record the cancelled cheque number in your log. Inform the payee quickly, and share the replacement cheque details for tracking.

What precautions help prevent tampering after I issue a cheque?Write with dark ink and keep entries tightly spaced. Strike through unused space on the amount-in-words line. Use crossing and account payee restrictions for third-party payments. Avoid handing over signed blank cheques. Record the cheque number, payee, and amount immediately after issue for traceability and follow-up.

Can someone else deposit a cheque on behalf of the payee?Deposit acceptance depends on the cheque type and bank policy. Account payee cheques are intended for credit to the named payee’s account. Other formats may allow collection under bank checks and endorsements. Payee name accuracy and crossing reduce ambiguity. For sensitive payments, prefer account payee marking.

What is the safest way to issue cheques for recurring payments like rent?Maintain a cheque register with month, payee, amount, and cheque number. Issue instruments close to expected deposit dates to reduce validity risk. Use account payee crossing for traceable collection. Maintain sufficient balance near presentation dates. Reconcile monthly using bank statements and landlord receipts for a clean closure.

How do stop payment requests work?A stop payment request instructs the bank to decline payment on a specific cheque if presented. Provide cheque number, date, and amount details through branch, netbanking, or mobile app channels. Charges and timing depend on the bank. Keep the confirmation reference, since it supports follow-up and disputes.

What details should a business maintain for cheque audit and reconciliation?Maintain a log with cheque number, issue date, payee, amount, invoice reference, approver, and signer. Add the deposit date, credit confirmation, or return reason after processing. Store supporting documents such as invoice copies and deposit slips. This structure supports vendor queries, accounting closure, and audit readiness.